Green Finance – An Islamic Way to Rescue the Nature

Ahmad Fraz (PIDE)

Interest is prohibited in Islamic finance and forbidden to generate money by money. According to Islamic rules money itself has no value and is just a way to define the value in Sharia’s law. Furthermore, risk is being shared in business activities by market participants. The key issue in Islamic finance is to guarantee the wealth increase by productive activities. The element of speculation and gambling which uncertainty “Gharar” is forbidden in Islamic finance. The uncertainty can be avoided by using equity principle. To invest in non-ethical industry like alcohol, tobacco and adult entertainment is prohibited in Islamic finance.

Islam demands comprehensive development of an economy and emphasizes social welfare. Its teachings stress translating shariah principles into practice and integrate them into individual and collective human life. The investments which are beneficial to the society are encouraged by Islamic finance. The concept of the maqasid al sharia supports the principle of serving the public interest of maximizing benefit and reducing harm to the society. Therefore, firms have a dual objective of generating economic gains along with a positive impact on society. There is a strong nexus between Islamic finance and green finance.

In Shariah, there is an emphasis on conservation, preservation, and responsible use of resources. There is a discouragement for excessiveness, and wastefulness in the use of resources. The realization of the value of the environment even if it is in no one’s private ownership is vital for fostering a culture of care and responsibility towards the environment. The steps towards preserving and conserving the climate are fundamental to promote environmental sustainability. The first step in this dimension recognition of climate as an asset endowment by Allah and its use responsible use.

The financing of green projects or firms is a challenging issue. The acceptability and growth in green finance require work in two domains i.e. creating a conducive environment for mobilizing capital for financing climate-friendly projects and/or firms and developing environment-friendly innovative financial instruments. The conducive environment means the development of a green finance ecosystem involving stakeholders that encourage the green businesses through regulatory frameworks and ensure the availability of financial instruments along with financing and an advisory mechanism.

“Islamic finance shares similar underlying principles as that of sustainable finance, i.e. financial stability and economic growth, poverty alleviation and wealth distribution, financial and social inclusion as well as environmental preservation. This has therefore allowed for Islamic finance to capitalize on these similarities to become a natural vehicle to propagate the elements of green finance.” [1]

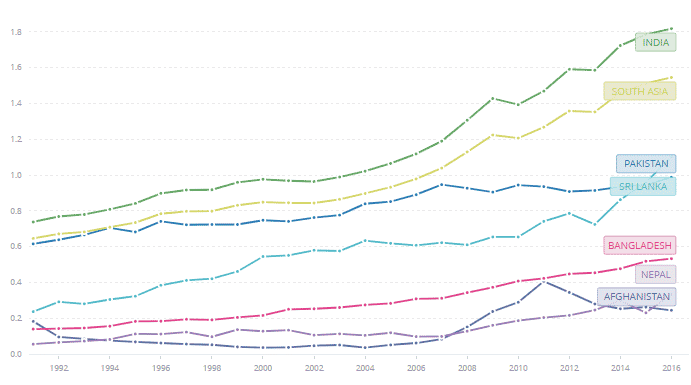

Figure 1 illustrates that CO2 emissions per person increased which suggests that there is a direct relationship between the GHG emissions and population. In case of India, CO2 emissions per capita increased from 1.0 to 1.8 metric tonnes per capita between 2000 and 2016. India is more vulnerable in South Asia. Pakistan and Sri Lanka are ranked second and third. The figure also presents the CO2 emission in Nepal and Afghanistan which indicate that these countries are facing a lower level of environmental and climatic issues. In general, procedural difficulties and the lack of awareness about how to safeguard the environment are major factors that may inflate the risks associated with environmental problems among countries located in the South Asian region as they pertain to CO2 emissions.

A green finance ecosystem may be composed of four major stakeholders including green finance promotors, green finance providers, green ecosystem coordinators, and ultimate users of green finance. Each of these parties may play a well-defined role in the conception, implementation, and financing of the whole scheme. The promotors may include governments, international agencies, and organizations. The green finance providers may be financial institutions in general and Islamic financial institutions in particular. Islamic green finance may include grants and investments. The creation of social finance ecosystems requires coordination between the green finance promotors and green finance providers and users. In addition, product development centers, and advisory firms, are necessary to create and maintain sustainable ecosystems. This will help to provide a framework, guidelines, and best practices to achieve the desired objectives.

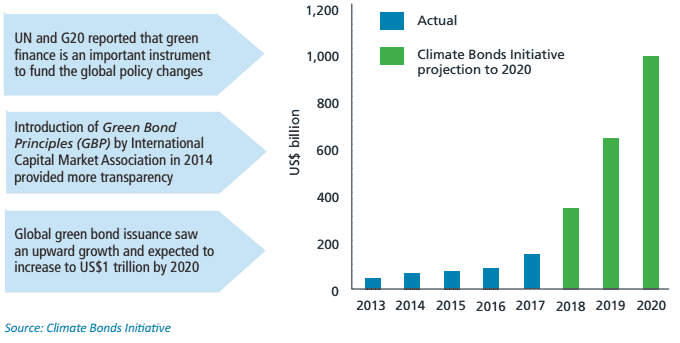

Advances in green finance are attracting global attention for finding alternative ways to finance socially responsible businesses and creating value in the society and Islamic Finance is not an exception. Green Sukuk is the first step in this direction. Green Sukuk are asset-based financial instruments structured to provide funding for renewable energy and environment-friendly projects and helps in achieving sustainable development goals. Although the advancement of Green Sukuk is a positive step its small market size poses numerous challenges. It is interesting that green equity is still missing which should an integral part of sustainable climate finance. The green equity may be a differentiating point for new firms and the existing firms may issue tracker stocks with the shariah-compliant green specification. The green bonds globally witnessed an upward curve between 2013 and 2017. The issuance amount in 2017 was at US$155.5 billion and it is expected to grow exponentially to US$1 trillion by 2020.

In past few years the growing investment through green finance shows the interest and concern of investors to fight against the climate change. Green finance is still at its initial stage and government can play a significant rule to assist the private sector to shift the conventional business models into the green finance model. The financial viability can be created though different incentives like tax exemptions and preferential tariff. Providing incentives can help reduce the costs of green adoption and certification. In nutshell, green Islamic finance can be a catalyst for the growth of environment-friendly growth and it can provide greater opportunities for Islamic finance to attract a wider investor base and expand its role to support sustainable objectives of finance.

_______________________

[1] Tan Sri Dato’ Seri Ranjit Ajit Singh, Chairman, Securities Commission Malaysia

[2] https://data.worldbank.org/indicator/EN.ATM.CO2E.KT?locations=8S

Figure 1: Country-wise Position of CO2 Emissions (Metric Tonnes Per Capita) in South Asia

Source: World Bank, “Data Indicators,”[2]

Source: World Bank, “Data Indicators,”[2]

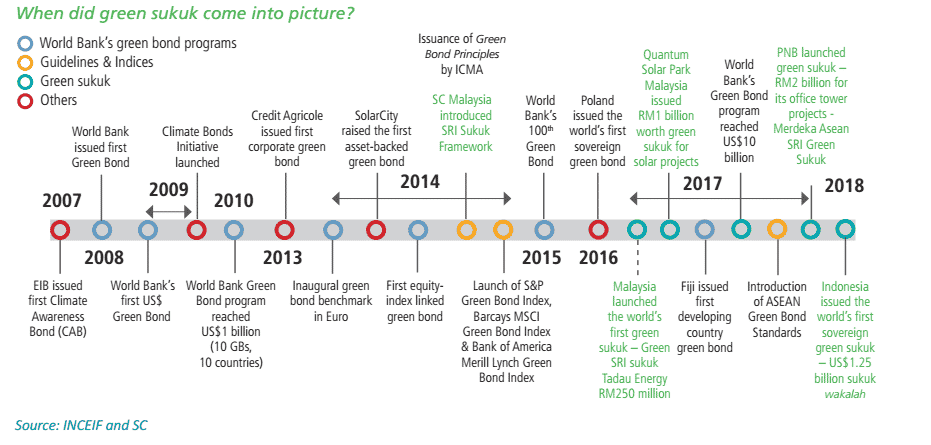

Figure 2: Evolution of the Green Bond and Sukuk Market

Source: INCEIF and SC

Source: INCEIF and SC

Figure 3: Upward Trajectory of Green Bond Issuance Globally

Source: Climate Bonds Initiative

Source: Climate Bonds Initiative