Executive Summary

The current oil price shock, emerged because of Israel-US-Iran war and its spread over the Gulf region, can have serious consequences on the fiscal consolidation efforts of the Government of Pakistan. The federal primary surplus, budgeted at Rs. 1,706 billion (1.3% of GDP), declines sharply across fiscalrisk scenarios. Under a moderate shock ($100/bbl), it falls to Rs 1,002 billion (0.7% of GDP), a reduction of Rs 704 billion (−0.6 percentage points). In a severe shock ($120/bbl), it drops to Rs 821 billion (0.6% of GDP), Rs 885 billion (−0.7 pp). In an extreme scenario ($144/bbl), it further declines to Rs 781 billion (0.6% of GDP), Rs 925 billion (−0.7 pp). At the same time, the fiscal deficit widens from Rs 6,501 billion (5.0% of GDP) to Rs 7,517 billion (5.8% of GDP), reflecting rising fiscal stress.

1. Introduction

In the wake of the Israel-US-Iran war, the disruptions in the supply chain of petroleum products have shown serious consequences for Pakistan, which are not limited to the economy but also on the fiscal consolidation as well. Rising oil prices increase the import bill, intensify inflationary pressures, and place downward pressure on the exchange rate, thereby slowing economic activity. The existing closure of the Strait of Hormuz, if prolonged, can elevate industrial input costs and weaken overall business confidence. Furthermore, higher energy prices may also widen the trade deficit and strain external financing needs. It reduces fiscal space, while increasing subsidy pressures and lowering the petroleum levy can undermine ongoing fiscal consolidation efforts. Accordingly, it can significantly increase the fiscal deficit and reduce the primary balance. Against this background, the primary balance provides the most useful fiscal lens for assessing whether Pakistan can absorb an external oil shock without undermining stabilization gains.

2. Oil Price Shocks and Pakistan’s Macroeconomic Vulnerability

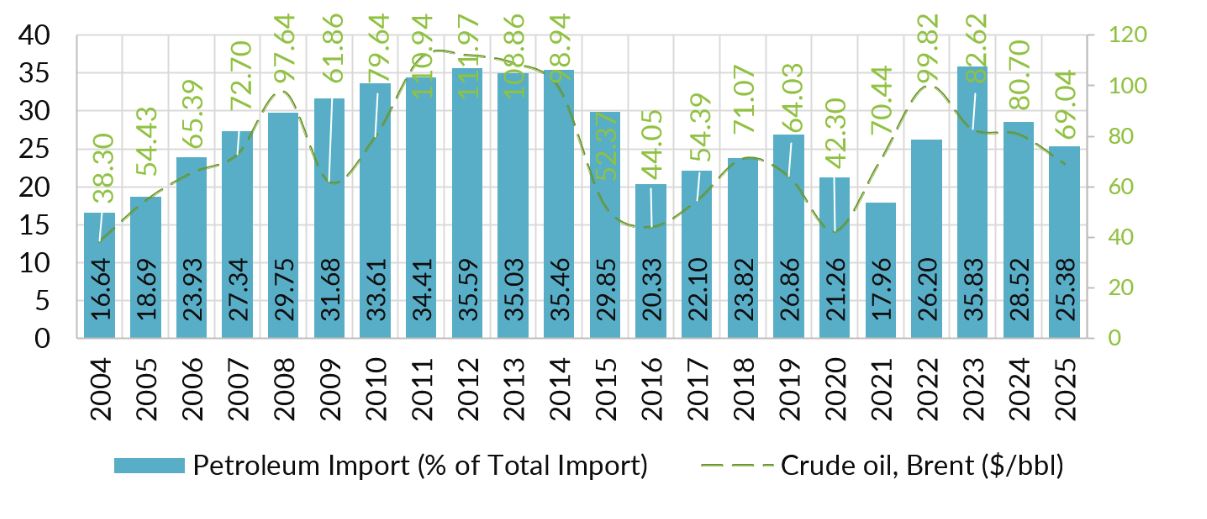

The oil price shock often leads to increased petroleum import costs, pressure on the external sector, rising inflation, slower growth, and increased fiscal vulnerability. Oil shocks have consistently been transmitted to Pakistan through imported inflation, external financing stress, subsidy pressure, and deterioration in fiscal buffers (See Appendix Table 1). The global oil price collapse from 2014 to 2016 provided temporary relief to the external sector when crude oil prices declined from USD 98.94 per barrel to USD 44.05. It led to a reduction in imports to USD 8.36 billion (20.33% of total imports) in 2016 (Figure 1). Following the U-shaped recovery of the global economy, the Russia-Ukraine war again put pressure on the external sector by increasing imports to USD 18.88 billion (35.83% of total imports). It again highlights Pakistan’s economic exposure to oil price shocks. Although oil prices were somewhat moderated in 2004 and 2025, the external sector remained highly sensitive to global energy market fluctuations.

Figure 1: Petroleum Imports and Global Oil Prices: Pakistan’s External Vulnerability

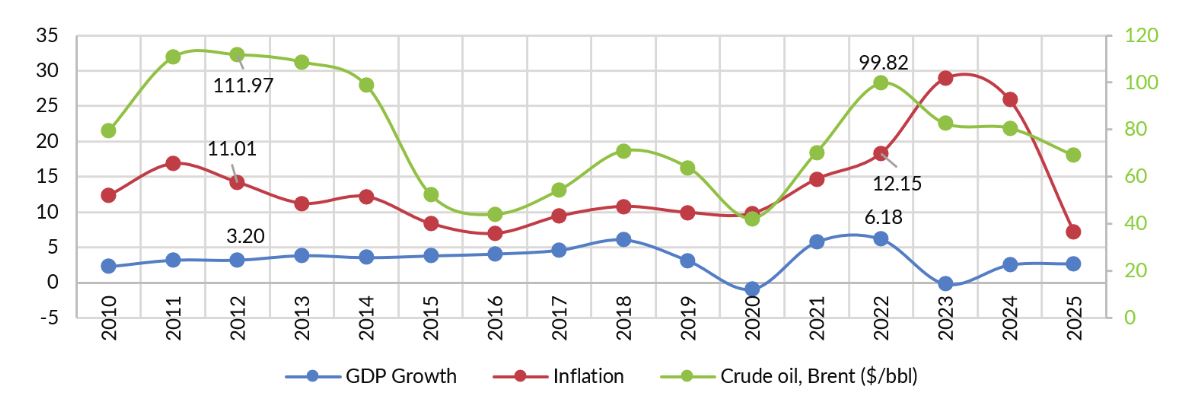

Oil price movements in the international market underscore a strong relationship with inflation in Pakistan. For instance, during 2011-2012, when Brent prices exceeded $110 per barrel, inflation remained in double digits (Figure 2). In contrast, the significant decline in global oil prices during 2015-2016, when Brent fell to around $44-52 per barrel, coincided with a sharp moderation in inflation to below 5 percent. This reflects the economy’s structural dependence on imported energy and the strong pass-through from international prices to local fuel, transport, and production costs.

Oil-driven inflationary pressures are closely associated with weaker or more volatile growth outcomes. Periods of macroeconomic stress, particularly 2020 and 2023, combine elevated inflation with subdued or negative economic growth. As such, inflation surged to 29.18 percent in FY2023 while GDP growth turned negative at -0.21 percent (Figure 2), reflecting the combined impact of external shocks, energy price volatility, domestic macroeconomic imbalances, and tightening policy conditions. Managing external shocks, particularly oil price volatility, and maintaining sustained macroeconomic stability are critical prerequisites for sustained and equitable economic growth in Pakistan.

Figure 2: GDP Growth, Inflation, and Brent Crude Oil Prices

3. Oil Price Shocks and Fiscal Sustainability in Pakistan

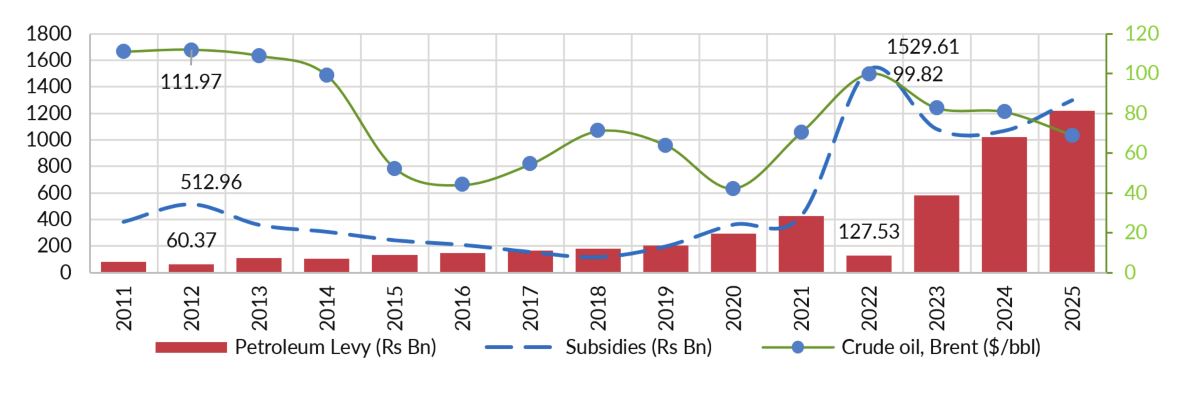

Petroleum Levy and subsidy expenditures have remained key instruments during periods of price pressures, thereby undermining fiscal sustainability. Fiscal pressures were intensified around 2011-2014. In 2022, Brent crude oil price approached nearly $100 per barrel, and subsidy expenditures surged to Rs 1,529.6 billion. At the same time, petroleum levy collections declined to about Rs 127.5 billion, indicating the government’s discretion to avoid pass-through. Furthermore, the increase in the petroleum levy to Rs 100 per liter in the Finance Act 2025-26 reflects the Federal Government’s policy of using it as the main source of revenue and to enhance fiscal consolidation.

Figure 3: Global Oil Prices and Pakistan’s Fiscal Response

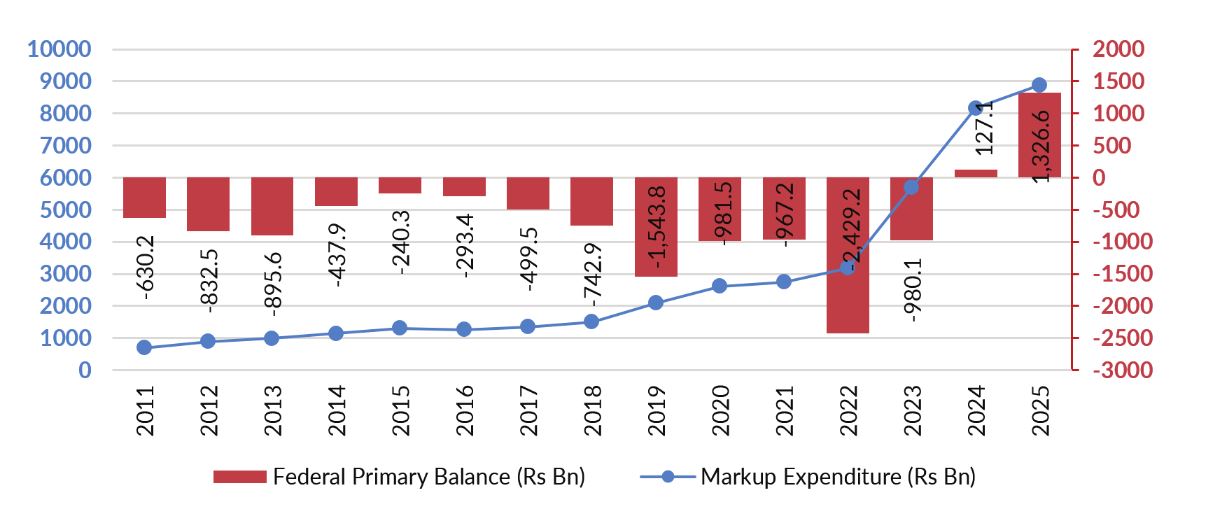

The federal primary balance (difference between net federal revenues and non-markup expenditures) is a critical indicator of debt sustainability. For instance, the federal primary deficit from 2011 to 2023 led to the debt-to-GDP ratio exceeding the 70 percent benchmark of debt sustainability. Given that Pakistan is under the IMF’s Extended Fund Facility programme, room for discretionary reduction in the petroleum levy is constrained by federal revenue targets and the fiscal commitments embedded in the current macroeconomic framework. However, it seems plausible under an alternative arrangement to cross-subsidize the prices of petroleum products by a decrease in expenditures.

Figure 4: Fiscal Sustainability: Interest Burden and Primary Balance

The Prime Minister of Pakistan has announced several measures to contain expenditures. However, in the volatile war situation and rising price pressures on petroleum products, the question remains: for how long and to what extent can the government absorb the decline in petroleum levy, particularly when it cannot afford to derail the IMF programme. For this, Pakistan achieve to achieve a Federal Primary surplus of Rs 1,706 billion (Rs 3,170 billion overall) during the current fiscal year. The fiscal implications of an oil shock extend beyond petroleum pricing decisions alone. They also operate through lower revenue collection, possible energy-sector support requirements, exchange-rate pressures, and contingent liabilities in the broader energy chain. These channels must be assessed jointly in any realistic fiscal-risk exercise.

4. Fiscal Risk Analysis: FY2026

This section provides an analysis of fiscal risk, assuming possible macro-fiscal implications of alternative oil price shock scenarios, using actual fiscal and macroeconomic data for the current fiscal year. Scenario 1: Oil Price at $100 per Barrel (Moderate Shock)

Starting from an already prevailing FBR revenue shortfall during the first half of the current fiscal year, the fiscal position weakens relative to budget projections. The federal fiscal deficit rises from the budgeted Rs 6,501 billion (5.0 percent of GDP) to Rs 7,333 billion (5.7 percent of GDP). At the same time, the federal primary surplus is expected to decline significantly from Rs 1,706 billion (1.3 percent of GDP) to Rs 1,002 billion (0.7 percent of GDP). This decline reflects rising expenditure pressures, partially managed through austerity measures, contingency spending, and lower development expenditures, despite some revenue support from higher nominal GDP.