by Dr. Talat Anwar

CPEC mega project worth USD 62 billion is considered to be a game changer for Pakistan. The progress of CPEC has, however, been affected in the wake of economic crisis since 2018. There have been reservations among international donors that CPEC loans have resulted in enormous imports of Chinese equipment and materials, leading to a higher debt burden for Pakistan in 2018. In this context, it is important to examine Pakistan’s debt sustainability and dependence on Chinese loans.

Pakistan’s total external debt and liabilities increased by USD 31.6 billion between FY15 and FY18, to reach USD 96.7 billion by September 2018. Owing to higher borrowing in order to finance the fiscal deficit, current account deficit in 2017-18 increased to USD 19 billion (5.9 percent of GDP), leading to depletion of foreign exchange reserves and financial crisis in 2018. The increase in the public external debt was primarily due to disbursements from IFIs, China, foreign commercial banks and the Sukuk bond proceeds, and on account of revaluation losses issued during this period. Notably, the country relied more on China, both in terms of CPEC-related and short-term commercial loans. The increased borrowing from China, both CPEC-related and commercial, at USD 3.9 billion and US 4 billion, respectively in 2016-17 and 2017-18 has important implications for debt sustainability.

These commercial loans were for balance of payments support with a maturity of 2-3 years and a floating rate based on LIBOR. It is noteworthy that most of these Chinese loans of a total USD 6.6 billion (or 2.1 percent of GDP) are front loaded as debt service payments over the next three years. This has increased the country’s gross financing needs along with vulnerability of the balance of payment account during 2018 and 2019.

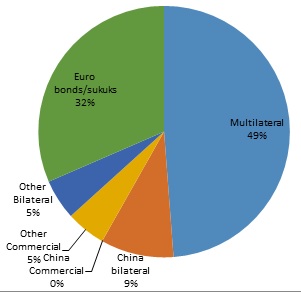

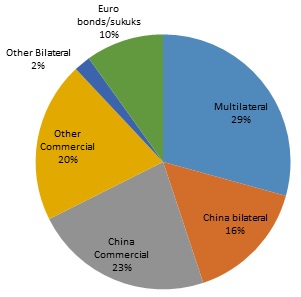

The heavy reliance on Chinese loans is clearly reflected by the rising share of China in total disbursement (See Figure 1 & 2). As a result, the share of disbursement from China (both bilateral and commercial) increased substantially from 9.4 percent in 2013-14 to 39 percent in 2016-17 and surpassed the share of multilateral of 29 percent in 2016-17.

The increased borrowing from China, including both CPEC-related and commercial, at USD 3.9 billion and US 4 billion respectively in 2016-17 and 2017-18, has important implications for debt sustainability. Chinese foreign loans together with domestic borrowing increased the fiscal deficit to an unsustainable level and worsened the country’s debt profile rapidly in a short period of one year. As a result, Pakistan’s debt-to-GDP ratio increased significantly by 6 percentage points from 67 percent of GDP in 2017-18 – well beyond the debt sustainability limit of 60 percent of GDP defined under the FRDL Act, 2005.

The growing unsustainable debt burden, together with increased payment difficulties in debt servicing, has now adversely impacted the economic and financial sustainability of CPEC projects. Fiscal consolidation in 2019-20 through scaling down of public investment spending, including CPEC-related PSDP projects coupled with interest rate rise under IMF program have slowed down the progress of CPEC.

According to IMF program document, Pakistan has to pay back US$ 37 billion to both bilateral and multilateral creditors over the IMF program period, 2019-22. Out of the total repayment, Pakistan will have to pay back USD 14.7 billion to China as repayment of bilateral and commercial debt during this period. In the current fiscal year 2019-20, total external debt servicing will be USD 14.9 billion (or 62 percent of exports earning), increasing the vulnerability of the balance of payment account. Increased debt servicing has reduced the fiscal space for development expenditure in particular the CPEC related infrastructure projects which are vital for restoration economic growth and employment creation which has been contracted due to the stabilization dosage of the IMF program.

Though reduction in current account deficit is achieved now, a further worsening of economic growth combined with high inflation will have adverse consequences for the people and inevitably for standards of living of the poor and the already squeezed middle class. Pursuing policies that reduce the debt servicing burden needs to be emphasized. The current debt servicing burden can be reduced through rescheduling and re-profiling of Chinese loans. Immediate policy decisions are, therefore, required to initiate discussion with our all-time friend China for re-profiling of Chinese loans in order to reduce the debt burden on the economy. The reduced debt burden will provide fiscal space to allocate expenditure in order to accelerate the progress on CPEC projects. We must remember that CPEC will not be a game changer unless we complete it and use it to our advantage.

Dr. Talat Anwar you are right Debt-to-GDP ratio is well beyond the debt sustainability limit of 60 percent of GDP defined under Fiscal Responsibility and Debt Limitation Act, 2005 (FRDL). Section 9 of FRDL provides the mechanism for compliance with the law, but I believe FRDL will be once again amended as was done in 2016 to provide relief to the government.

[…] project fuelled by foreign capital. However, the circular debt problem of Pakistan cannot be attributed to the Chinese loans alone. But the absence of requisite reforms in power sector particularly, and […]

CEPC was really a game changer but the owners and promisors has been kicked out. This project has been put at stake due to current political situation and intervention of establishment. Our GDP growth continuously went up from 3.68 % to 5.8% since inception of CPEC in 2013 to 2018. Our GDP growth rate flattened to 1.7% within one year when when the current govt. said Goodbye to CPEC.