By Mr. Shahid Sattar and Mr. Saad Umar

Editor’s Note: This is Part 1 of a 3 part article on Pakistan’s Power Sector.

Addressing Pakistan’s Power Sector Woes

The woes of Pakistan’s power sector and associated negatives are not unknown. These range from such as impact on GDP, high tariffs, prolonged and frequent load shedding and poor governance. Addressal of the same requires careful unfolding of the layers of mismanagement that continue to plague the sector’s supply chain.

Pakistan: A Single Buyer Model

To begin with, it is important to consider Pakistan’s power sector performance at a regional level. How does it fare in terms of pricing, market development, generation and transmission when compared with other South Asian economies. We should treat electricity as a commodity, conceptually separating production and trading from operation of the power system. On the other hand, Pakistan has a single buyer model that purchases electricity from GENCOs and supplies to DISCOs. This means that the monopoly status of electric utilities does not incentivize efficiency and instead encourages them to pass on the cost of their resultant inefficiencies to consumers in the form of heightened tariffs.

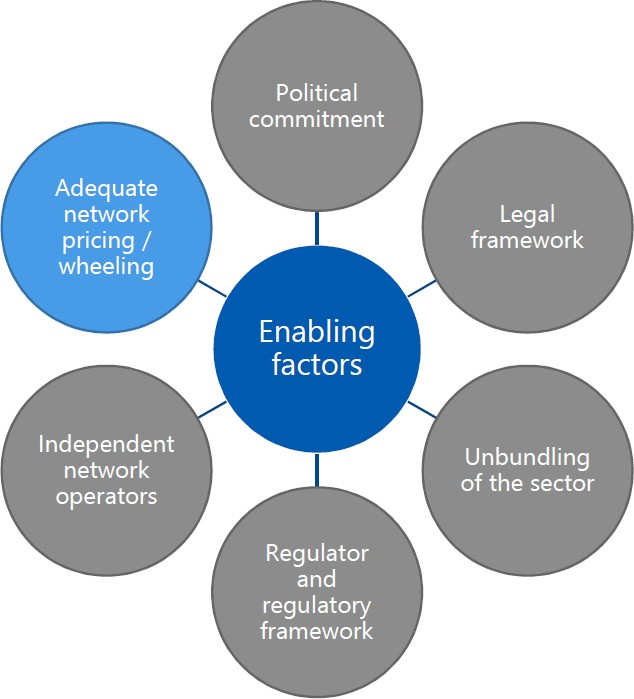

If Pakistan’s supply of electricity becomes the object of market discipline rather than monopoly regulation of government policy, the economy and end consumer will have much to benefit from competitive markets. This, however, will not be a straightforward process requiring interplay of several factors, as illustrated in Figure 1.

Competitive Electricity Markets

Competitive markets in the power sector can include i) wholesale, creating more competition for generating companies, and (ii) retail, catering for small consumers who cannot buy from the wholesale market. Prices in the first instance are determined by the interplay of supply and demand. Such competitive electricity markets are not alien to South Asian economies like Turkey and Bangladesh, and Pakistan may have important lessons to learn from these experiences.

In the country’s defense, however, some well-intentioned decisions have been made. This includes the ECC’s decision to move to a Competitive Trading Bilateral Contracts Market (CTBCM). This transforms the single-buyer market model to a CTBCM where NEPRA and CPPA-G are working closely to establish the Contracts Market in their own capacities.

CTBCM does have severe limitations however, since the generation side is already completely tied up in long-term generation contracts. Distribution competition can only be termed as an irrelevant exercise as there are no free suppliers in the foreseeable future. One way of freeing some generation for competition is urgent re-negotiation of all PPAs of existing IPPs to guarantee 50% of capacity, and balance to be traded or sold directly on B2B basis either through wheeling or from a power exchange.

Wheeling

Wheeling, a process whereby efficiencies are maximized by moving least-cost power to where it is needed, is the first step in achieving competitive markets. If wheeling is an option, a utility can determine if it is cheaper to build a new electric generation facility or buy power from another service area. Wheeling can achieve many benefits like open access to all market participants on a non-discriminatory B2B basis, attracting investment, and evolving the wholesale market and eliminating sovereign guarantees. To be financially viable, however, wheeling charges must be determined by the economic principle of marginal cost rather than incorporating all the inefficiencies of theft, stranded cost, non-collection and improper cross- subsidies which endanger the development of competitive markets. Currently, the existing charges for wheeling in Pakistan are Rs.1.35 to Rs.1.50 per kwh which the CPPA wants to increase to Rs.8.3/kwh by incorporating the aforesaid inefficiencies. The proposal by CPPA of adding irrational and unjustified costs in wheeling charges (including BPCs) will obstruct the formation of free and competitive markets – increasing employment, GDP and exports for Pakistan – especially when the power sector is close to achieving breakthrough of signing MoUs with IPPs to start operating on Take and Pay basis (i.e. without capacity payments) and various other concessions to lower generation costs and the establishment of a competitive market is one of the preconditions of the MoUs.

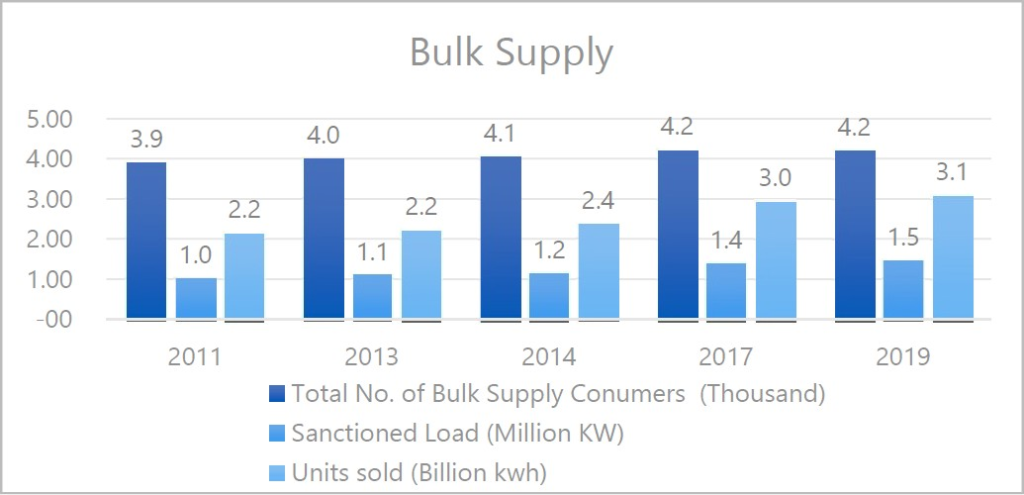

Bulk Supply Consumers

Figure 2 shows that Bulk Supply Consumers have grown from 3.91 million to 4.22 million in Pakistan (8% increase), while consumption has increased from 2.16 billion kWh to 3.09 billion kWh (43% increase). If bilateral contracts become financially unviable owing to excess (above legitimate) wheeling charges to BPCs, the development of competition will be threatened in the long term and export-oriented industries will become non-competitive. Moreover, it will have significant financial impact if costs are recovered from BPCs by DISCOs on Cost of Service which includes irrelevant business costs which are not part of the wire business.