Austerity: Which Way Now?

Abdul Jalil, Professor of Economics, Pakistan Institute of Development Economics, Islamabad.*

Austerity, during the global financial crisis, was the rubric used to define the highly contractionary policies at the cost of domestic social and infrastructural needs (see Varoufakis, 2017). Economies with high fiscal deficits and high debt to GDP ratios are often pushed to adopt austerity IMF programmes (see Box 1 and 2, Alesina, et al. (2019).

Does austerity help or hurt the stabilising country?

- Proponents, such as the IMF regard that as a moral responsibility to reduce the excessive debt accumulated due to policy mistakes and political distortions.

- Opponents, consider austerity as inappropriate, troublesome and disruptive. They also that increased taxes, reduced expenditures, or both could adversely affect productivity, growth employment and welfare.

Alesina, et al. (2019) and Ramey (2016) have done comprehensive work to demarcate which type of austerity is less distortionary. Expenditure-based austerity is less costly as compared to tax-based austerity. They note that tax-based austerity negatively hit private capital investment. Therefore, it has a longer negative effect in terms of size and span of time.

Can austerity be expansionary? Alesina, et al. (2019) claim that it is possible when accompanied by compensatory growth in private consumption, private investment and net exports. Few notable examples of the expansionary austerity are Ireland, Austria and Denmark, Canada, Spain and Sweden in 1980s and 1990s. More recently, the United Kingdom and Ireland did a better job in economic growth despite cutting back on the banking sector’s spending and issues. Apparently, countries with strong institutions and credible policy-making can generate required expansionary responses.

In this backdrop, the present knowledge brief is divided into two main parts. First, we shall review the existing literature on the fiscal multipliers: the government spending multipliers and the tax multipliers to draw some important conclusions. Second, we shall attempt to calculate the fiscal multipliers to invite the policy discussion in Pakistan.

| Box 1: Austerity and Stabilisations Austerity: The austerity is a policy of reducing government deficits and stabilising government debt by cutting government expenditure or increasing taxes or both. Alesina et al (2019a) discuss the expenditure-based austerity and tax-based austerity in greater details. Stabilisation: It is an imposed stringent monetary and fiscal discipline, as a condition, on the highly indebted economies which approach for the fund to correct their balance of payment problems. |

| Box 2: Policy Mistakes and Political Distortions The standard economic theory and the practice suggest that the economies run fiscal deficits in the period of economic down turn and then these deficits are balanced in boom period. Besides this, the forward looking and rational government also accumulate some extra funds for the difficult times. Therefore, theoretically, there is no need of austerity. On the contrary, the austerity policy is common in due to inadequate policy. That is, the country don’t save in boom period. They even run deficit in the boom period as well. The other important reason is that the countries need exceptional high spending due to war and other disasters mainly because of political distortions (Alesina, et al 2019a). |

____________________________________

Acknowledgement: My thanks to Nadeem UI Haque for suggesting the topic and his guidance through the project. Actually, this note is his brainchild. I am also grateful to Hammad Manzoor, a PhD student of PIDE for his help in preparing this note. Errors of course remain the responsibility of the author.

Empirical Evidence Around the World

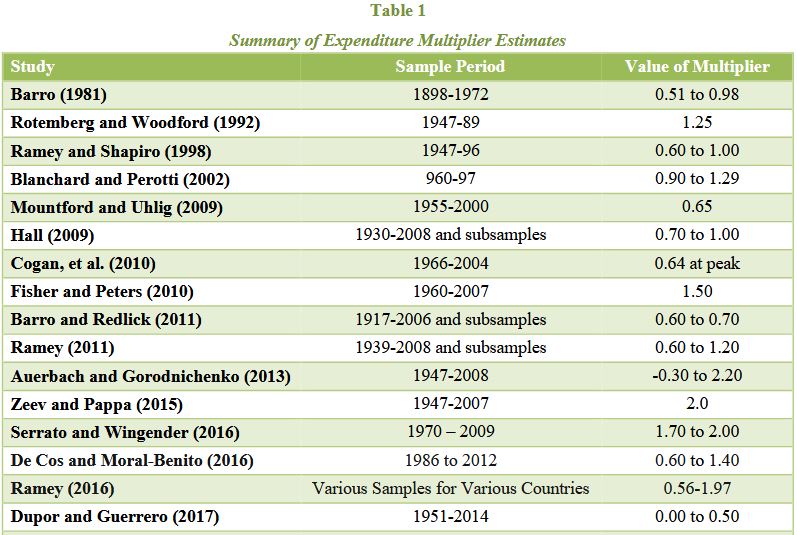

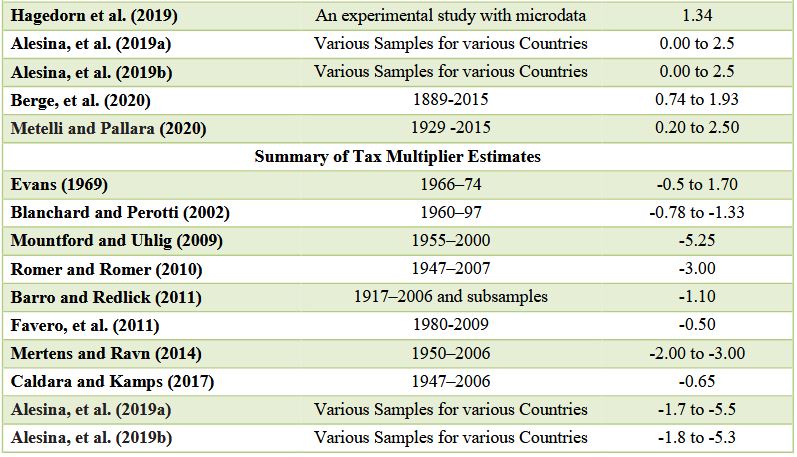

To begin with, let us review fiscal multipliers (See Table 1). The key takeaways are:

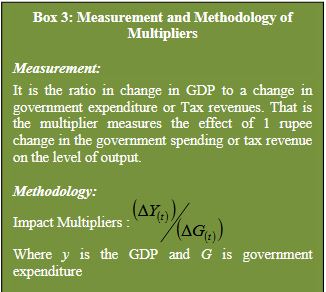

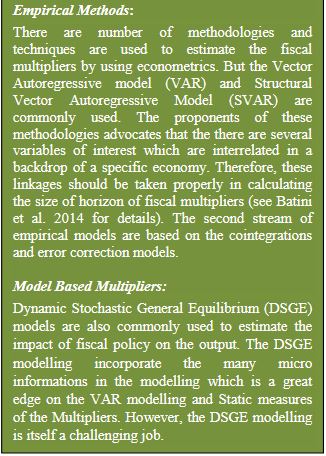

- (1) The calculation of fiscal multipliers is not a straightforward task. Different studies provide different estimates even for the same economy depending on the focus, objective, assumptions and methodology (see Box 3).

- (2) There is a considerable difference between the expenditure-based austerity plan and tax-based austerity plan.

- The expenditure multipliers range from 0.00 to 2.5, i.e., the growth impact could be positive if done well. In any case, the negative impact is low.

- Tax multipliers are –0.5 to –5.5, i.e., tax-based austerity always slows down economic growth.

- (3) Alesina, et al. (2019a) document that;

- A 1 percent reduction in deficit through cuts on government expenditure is associated with the 0.5 percentage point reduction in GDP, and the recession will last a couple of years.

- On the other hand, a 1 percent reduction in deficit through the tax-based austerity is associated with a 2 to 3 percent loss of GDP growth and recession will last for several years.

- (4) Furthermore, Alesina, et al. (2019b) note that the expenditure-based austerity may reduce the growth rate of debt to GDP ratio. On the other hand, the tax-based austerity plan may increase the growth rate of debt to GDP ratio.

- (5) Alesina, et al. (2019a) document that private investment in expenditure-based austerity plan differs from a tax-based austerity plan.

- The expenditure-based austerity plans boost the investors’ confidence and may help in the increase of private investment.

- However, the other aggregate demand components are that private consumption and net export do not differ during both austerity plans.

- (6) The impact of austerity policy plan is asymmetric in the recession and boom periods. It may hurt severely in the period of recession and the downturn compared to the boom period.

The Case of Pakistan

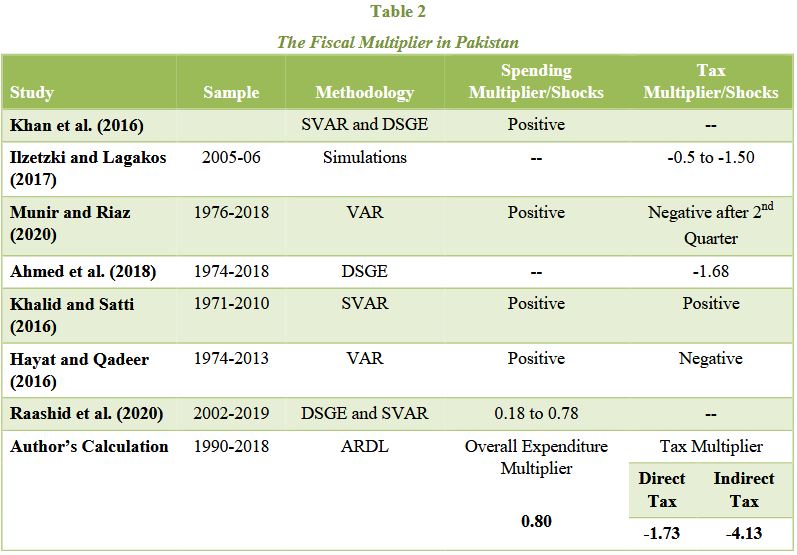

Few studies have estimated the fiscal multipliers for Pakistan (see Table 2).[1]

The present brief calculates the numerical values of the overall government expenditure, development expenditure, current expenditure, direct taxes and indirect taxes (see Table 2). Our calculations are in line with Haque and Montiel (1993), Alesina, et al. (2019) and Ramey (2016). Highlights are:

- As expected, pending multipliers are positive, and tax multipliers are negative.

- The size of spending multiplier is smaller than the value of tax multipliers. That is, the tax-based austerity plan will hurt more as compared to the expenditure-based austerity plan.

- Further, the multipliers’ development expenditures are much higher than the current expenditure multiplier (see Box 4). This implies that cutting development expenditures is a fatal mistake even in the recessions.

[1]Most of the work has been done in term of shock and response. That is, what will be the response of output when shocks are given to government expenditures and taxes.

____________________________

[1]Most of the work has been done in term of shock and response. That is, what will be the response of output when shocks are given to government expenditures and taxes.

In a nutshell, expenditure-based stabilisation is preferable. is preferable, if inevitable, as compared to tax based austerity. Unfortunately, all our stabilisation programmes and donor-funded programmes that have guided our policy have been based on tax increases. As suggested in this analysis, the payoff is in expenditure reduction, especially reducing targeted and making expenditure efficiency and growth orientation. Alesina, et al. (2019a) suggest that the tax-based austerity hurt some essential components of aggregate demand: private consumption, private investment and net exports. Therefore, we estimate the impact of taxes through the channels of private consumptions and private investment. Note earlier PIDE studies have supported our findings that our policy orientation for the last three decades seeking stabilisation through increased taxation has negative growth consequences.

- Nasir, et al. (2020) have shown higher taxes, and excessive documentation reduce transactions in the economy leading to lower economic growth, Nizamani (2020) overwhelming empirical evidence across countries that tax increases reduce economic growth.

| Box 4: Haque and Montiel (1993) Macroeconomic Model on Fiscal Adjustments Haque and Montiel (1991, 1993) are some pioneer studies that made an empirical case for the fiscal adjustments for Pakistan based on the macroeconomic model. They simulate the fiscal adjustments in several different scenarios. The empirical findings suggest that the reducing the public consumption is the most favourable scenario for the medium term economic growth of Pakistan. The least favourable scenario is the reducing public investment. The revenue increase scenario is paced in the intermediate position. |

Conclusion

Three important messages can be drawn:

- The tax-based austerity is more costly and long-lasting than expenditure-based austerity irrespective of the nation, methodology, sample and focus.

- The current expenditure multiplier is lower than the development expenditure. Therefore, the cut in current expenditure will have an insignificant impact on economic growth.

- The indirect taxes are more distortionary as compared to direct taxes in an austerity policy plan. It hurt private consumptions and private investment.

Clearly, we and the IMF need to rethink our stabilisation approach. Tax increases for the last three decades have been arbitrary and distortionary and too frequent (Nasir 2020, Haque 2015). Perhaps, for this reason, long-run growth and productivity have been showing a declining trend over this period.

Expenditures are hard to rationalise and restrain. Salary increases and PSDP losses have piled up while political will or sagacity appears to be lacking. Private investment too remains low and declining wary of arbitrary and undertone tax increases and mindful of the lack of expenditure control. The business community continues to complain about the “cost of doing business” arising from this stabilisation approach based on uncertain and costly tax policy and lack of expenditure control.

This and other PIDE research shows the need to change our macro policy approach and focus on expenditures. It will require painstaking work and serious reform. But the payoffs could be large.

References

Ahmad, S., Sial., M. H. & Ahmad, N. (2018). Indirect taxes and economic growth: An empirical analysis of Pakistan. Pakistan Journal of Applied Economics, 28, 65–81.

Alesina, A., Favero, C., & Giavazzi, F. (2019a). Austerity: When it works and when it doesn’t. Princeton University Press.

Alesina, A., Favero, C., & Giavazzi, F. (2019b). Effects of austerity: Expenditure and tax-based approaches. Journal of Economic Perspectives, 33(2), 141–62.

Auerbach, A. J., & Gorodnichenko, Y. (2012). Fiscal multipliers in recession and expansion. In Fiscal policy after the financial crisis (pp. 63–98). University of Chicago Press.

Barro, R. J. (1981). Output effects of government purchases. Journal of political Economy, 89(6), 1086–1121.

Barro, R. J., & Redlick, C. J. (2011). Macroeconomic effects from government purchases and taxes. The Quarterly Journal of Economics, 126(1), 51–102.

Berge, T. J., De Ridder, M., & Pfajfar, D. (2020). When is the fiscal multiplier high? A comparison of four business cycle phases. (Finance and Economics Discussion Series 2020-026).

Blanchard, O., & Perotti, R. (2002). An empirical characterisation of the dynamic effects of changes in government spending and taxes on output. The Quarterly Journal of Economics, 117(4), 1329–1368.

Caldara, D., & Kamps, C. (2017). The analytics of SVARs: A unified framework to measure fiscal multipliers. The Review of Economic Studies, 84(3), 1015–1040.

Cogan, J. F., Cwik, T., Taylor, J. B., & Wieland, V. (2010). New Keynesian versus old Keynesian government spending multipliers. Journal of Economic Dynamics and Control, 34(3), 281–295.

De Cos, P. H., & Moral-Benito, E. (2016). Fiscal multipliers in turbulent times: The case of Spain. Empirical Economics, 50(4), 1589–1625.

Dupor, B., & Guerrero, R. (2017). Local and aggregate fiscal policy multipliers. Journal of Monetary Economics, 92, 16–30.

Evans, M. K. (1969). Reconstruction and estimation of the balanced budget multiplier. The Review of Economics and Statistics, 14–25.

Favero, C., Giavazzi, F., & Perego, J. (2011). Country heterogeneity and the international evidence on the effects of fiscal policy. IMF Economic Review, 59(4), 652–682.

Fisher, J. D., & Peters, R. (2010). Using stock returns to identify government spending shocks. The Economic Journal, 120(544), 414–436.

Hagedorn, M., Manovskii, I., & Mitman, K. (2019). The fiscal multiplier (No. w25571). National Bureau of Economic Research.

Hall, R. E. (2009). By how much does GDP rise if the government buys more output? (No. w15496). National Bureau of Economic Research.

Haque, N. & Montiel, P. (1991). The macroeconomics of public sector deficits: The case of Pakistan. (World Bank Working Paper No. 673).

Haque, N. & Montiel, P. (1993). Fiscal adjustment in Pakistan: Some simulation results. Staff Papers (International Monetary Fund). 40, 471–480.

Hayat, M. A., & Qadeer, H. (2016). Size and impact of fiscal multipliers: An analysis of selected South Asian Countries. Pakistan Economic and Social Review, 54, 205–231.

Ilzetzki, E. & Lagakos, D. (2017) The macroeconomic benefits of tax enforcement in Pakistan. A report of International Growth Centre. F-37405-PAK-1

Khalid, M. & Satti, U. I. (2016). Fiscal policy effectiveness for Pakistan: A structural VAR approach. The Pakistan Development Review, 55(4), 309–324.

Khan, S., Pasha, F., Rehman, M. & Choudhary, M. A. (2016). The dominant borrower syndrome: The case of Pakistan. (SBP Working Paper No. 77).

Mertens, K., & Ravn, M. O. (2014). A reconciliation of SVAR and narrative estimates of tax multipliers. Journal of Monetary Economics, 68, S1–S19.

Metelli, L., & Pallara, K. (2020). Fiscal space and the size of the fiscal multiplier. Bank of Italy Temi di Discussione (Working Paper No. 1293).

Mountford, A. & Uhlig, H. (2009). What are the effects of fiscal policy shocks? Journal of Applied Econometrics, 24(6), 960–992.

Munir, K. & Riaz, M. (2020). Macroeconomic effects of exogenous fiscal policy shocks in Pakistan: A disaggregated SVAR analysis. Hacienda Pública Española / Review of Public Economics, IEF, 233(2), 141–165.

Nasir, M., Faraz, N., & Anwar, S. (2020). Doing taxes better: Simply, open and grow economy. (PIDE Policy Viewpoint No. 17) https://file.pide.org.pk/pdf/Policy-Viewpoint-17.pdf

Nizamani, S. (2020). Higher taxes reduce economic growth: Overwhelming international evidence. (PIDE Knowledge Brief No. 14). https://file.pide.org.pk/pdf/PIDE-Knowledge-Brief-14.pdf

Ramey, V. A. (2011). Identifying government spending shocks: It’s all in the timing. The Quarterly Journal of Economics, 126(1), 1–50.

Ramey, V. (2016). Macroeconomic shocks and their propagation. Handbook of Macroeconomics, 2A, 71–162.

Ramey, V. A. & Shapiro, M. D. (1998, June). Costly capital reallocation and the effects of government spending. In Carnegie-Rochester conference series on public policy (Vol. 48, pp. 145-194). North-Holland.

Raashid, M., Saboor, A., & Ahmad, S. (2020). Fiscal policy transmission mechanism in Pakistan: A general equilibrium analysis. Business Review, 15(1), 50–66. https://ir.iba.edu.pk/businessreview/ vol15/iss1/10

Romer, C. D., & Romer, D. H. (2010). The macroeconomic effects of tax changes: estimates based on a new measure of fiscal shocks. American Economic Review, 100(3), 763–801.

Rotemberg, J. J., & Woodford, M. (1992). Oligopolistic pricing and the effects of aggregate demand on economic activity. Journal of Political Economy, 100(6), 1153–1207.

Serrato, J. C. S., & Wingender, P. (2016). Estimating local fiscal multipliers (No. w22425). National Bureau of Economic Research.

Varoufakis, Y. (2017). Adults in the room: My battle with Europe’s deep establishment. London and New York: Random House.

Zeev, N. B. & Pappa, E. (2015). Multipliers of unexpected increases in defense spending: An empirical investigation. Journal of Economic Dynamics and Control, 57, 205–226.