Pakistan is once again entering the season of fiscal planning, with the budget for the fiscal year 2025–26 imminent. However, for more than a decade, these budgets have mostly followed a routine pattern—focused more on projecting revenues and expenditures than on delivering transformative reforms. They tend to prioritize maintaining the status quo over introducing meaningful change.

Pakistan is at a critical juncture where in the past routine budgeting will no longer suffice. In this year, there is a need to shift away from the conventional fiscal framework and present a business-growth-oriented budget. A budget that invigorates entrepreneurial aspirations and elaborates the sectors of production even further, unlocking the real potential of Pakistan’s economy.

Over the course of the past decade, consecutive government budgets have mostly focused on debt payments, military, and current expenditures. There has been very little attention paid to encouraging innovation, providing assistance for small and medium-sized enterprises (SMEs), or generating development that is led by the private sector. However, even though budget expenditures are increasing—from 3.9 trillion Pakistani rupees in 2014–15 to nearly 14.4 trillion Pakistani rupees in 2023–24—the quality of spending and its impact on the actual economy continue to be abysmal. Over the past decade, budgets have consistently followed shifting themes, from infrastructure development to fiscal tightening, but have lacked a coherent long-term reform strategy focused on business-led growth. The table below summarizes the key focus areas of each budget since FY 2014 -2015.

Table 1 Key Focus Areas of Federal Budget from 2015 to 2025

| Fiscal Year | Key Focus |

| Budget 2014-15 | Energy sector reforms, tax base expansion, and infrastructure development |

| Budget 2015-16 | CPEC investments, tax reforms, and social safety nets (BISP allocations increased). |

| Budget 2016-17 | Infrastructure (CPEC projects), agriculture subsidies, and FBR reforms. |

| Budget 2017-18 | Election-year budget with tax relief, higher PSDP, and energy projects. |

| Budget 2018-19 | Austerity measures, IMF negotiations, and fiscal consolidation. |

| Budget 2019-20 | IMF-backed reforms, tax hikes, social protection (Ehsaas Program). |

| Budget 2020-21 | COVID relief, healthcare boost, and stimulus packages. |

| Budget 2021-22 | Growth-oriented budget, Kamyab Jawan Program, and tax incentives. |

| Budget 2022-23 | Flood relief, IMF conditions, and fiscal tightening. |

| Budget 2023-24 | Austerity, tax hikes, and IMF deal compliance. |

| Budget 2024-25 | Economic stability and growth, fiscal consolidation, efficient use of Public Money, improving balance of payments, revitalizing private sector, |

Source: Pakistan Economic Survey (Various Editions)

A quick look at budget trends over the last ten years shows where our priorities are. The table below presents yearly allocations as percentages of total budget outlays from FY2015 through FY2025. What stands out is not just what is included, but what is left out: The sharp fall in education allocation—1.5% in FY2015 to 0.5% in FY2025—underscores misplaced priorities. Health expenditure is even worse, remaining at 0.1-0.3%. In return, more than 60% of the federal budget is eaten up by defense and debt repayment. Such a composition has made the budget a growth-retarding rather than growth-stimulating instrument.

Table 2 Yearly allocation as percentage of total budget outlay (2015 – 2025)

| Year | Total Budget (PKR Trillion) | Defence | Debt Servicing | Education | Health | Subsidies | Social Protection |

| FY15 | 4.30 | 16.3% | 30.8% | 1.5% | 0.2% | 4.7% | 0.04% |

| FY16 | 4.45 | 17.6% | 28.8% | 1.7% | 0.2% | 3.1% | 0.04% |

| FY17 | 4.89 | 17.6% | 27.8% | 1.7% | 0.2% | 2.9% | 0.04% |

| FY18 | 4.75 | 19.4% | 28.7% | 1.9% | 0.3% | 2.9% | 0.04% |

| FY19 | 5.93 | 18.5% | 27.3% | 1.6% | 0.2% | 2.9% | 0.04% |

| FY20 | 7.04 | 16.4% | 41.1% | 1.1% | 0.2% | 3.9% | 2.71% |

| FY21 | 7.29 | 17.7% | 40.4% | 1.1% | 0.3% | 8.8% | 3.17% |

| FY22 | 8.49 | 16.2% | 36.0% | 1.1% | 0.3% | 8.0% | 3.01% |

| FY23 | 9.50 | 16.5% | 41.6% | 1.0% | 0.2% | 7.0% | 3.90% |

| FY24 | 14.46 | 12.5% | 50.5% | 0.7% | 0.2% | 7.4% | 3.32% |

| FY25 | 18.88 | 11.3% | 51.8% | 0.5% | 0.1% | 7.2% | 3.22% |

Source: Pakistan Economic Survey (Various Editions)

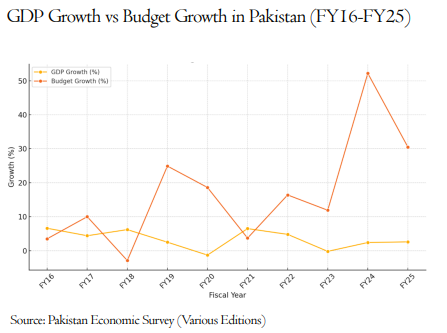

Even with large increases in budgetary allocations over the last decade, Pakistan’s economic growth has been uneven and largely unresponsive. A comparison between GDP growth and budget growth shows a wide divergence—years of high budget growth did not coincide with higher GDP growth. For example, the federal budget grew well above 52 percent in FY24 with only modest 2.4 percent GDP growth. More examples: the budget increased by almost 19 percent in FY20 and the economy contracted by 1.3 percent; more again, the economy grew 6.5 percent in FY21, but the budget grew only 3.7 percent. Such data points imply that greater fiscal outlays are not being converted into actual economic development. The key problem is the way the budget is set up: a big part is used by unproductive spending like paying off debts and security, which leaves little room for putting money into sectors that improve growth— such as human capital, new ideas, and industrial productivity.

Even with large increases in budgetary allocations over the last decade, Pakistan’s economic growth has been uneven and largely unresponsive. A comparison between GDP growth and budget growth shows a wide divergence—years of high budget growth did not coincide with higher GDP growth. For example, the federal budget grew well above 52 percent in FY24 with only modest 2.4 percent GDP growth. More examples: the budget increased by almost 19 percent in FY20 and the economy contracted by 1.3 percent; more again, the economy grew 6.5 percent in FY21, but the budget grew only 3.7 percent. Such data points imply that greater fiscal outlays are not being converted into actual economic development. The key problem is the way the budget is set up: a big part is used by unproductive spending like paying off debts and security, which leaves little room for putting money into sectors that improve growth— such as human capital, new ideas, and industrial productivity.

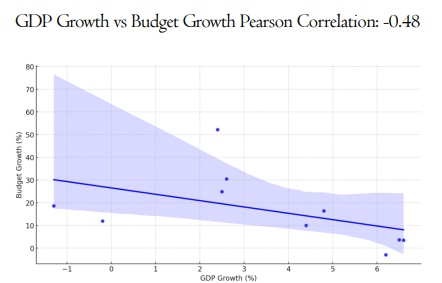

The analysis reflects a negative correlation of about -0.48 between GDP growth and budget growth over the last 10 years in Pakistan. It means there is no evident or positive correlation between the size of the budget and economic growth. More so, in many years when the budget grew significantly, GDP growth stagnated or even declined — indicating that most of the times, the budget has not functioned as a growth engine.

The disconnect between budgetary expansion and GDP growth shows a fundamental flaw in how fiscal priorities are set and executed in Pakistan. Each year, public finances have grown in size, but spending remained inward – looking (internal government operations and short-term obligations). Which further substantiates the argument for a budget design that is reoriented toward productivity, private sector facilitation, and human capital investment—rather than merely expanding fiscal outlays without impact.

A business-as-usual approach has failed to translate contemporary budgeting exercise into meaningful economic outputs. This neglect is most visible in the limited support for small businesses and startups despite their critical role in employment generation and value creation. Pakistan’s growing population, especially its youth and women, holds significant entrepreneurial potential which at present is dead capital. To unlock it and shift from fiscal expansion to real economic transformation, the budget must begin to directly empower those who drive innovation and productivity. To that end, we propose five key shifts:

Firstly, reassign at least 2% of the federal budget to a “Business Innovation Fund/Innofund” for SMEs more women and youth entrepreneurs. The main barrier is access to finance; currently, only 6% of Pakistani SMEs have bank loans. This fund shall put forth interest-free micro-investments and technical support. Models like Rwanda’s YouthConnekt or Bangladesh’s SME Foundation offer viable blueprints.

Secondly, remove the red tape and instead roll out the red carpet for businesses. Initiate a “One-Click Business Registration Portal” for all parts of the country, linked with NADRA and FBR, only requiring CNIC and bank details. Eliminate NOC regimes and departmental approvals; startup costs can be reduced by 70% along with the time taken—Georgia’s business reform model demonstrates this and pushed it into the top 10 of the World Bank’s Ease of Doing Business Index.

Third, introduce a special tax regime for new businesses with a three-year tax holiday and simplified tax return. Countries like Vietnam and Turkey have used such incentives to incubate a vibrant startup ecosystem and attract FDI.

Fourth, set up “Business Growth Zones” in every district having co-working spaces with digital infrastructure plus tax facilitation counters next to logistics support. Utilizing existing public sector buildings like schools after-hours or Basic Health Units for training as well as incubation centers would further develop these zones—akin to the earlier proposed Village Economic Zones model.

Fifth, harmonize fiscal and monetary policies to realize pro-growth outcomes. For instance, with inflation now less than 4% and interest rates having fallen from 22% to 11%, the forthcoming budget should indicate a unified fiscal-monetary stimulus. This should include guidelines on how to direct public expenditure towards sectors that enable exports—IT, agriculture, green energy. Pakistan can gain from regional trade if barriers are removed and logistics streamlined.

This reorientation has been shown to have a number of different advantages. Studies conducted by the International Monetary Fund and the World Bank indicate that reforms aimed at small and medium-sized enterprises (SMEs) in East Asia contributed more than forty percent to the increase of the GDP between the years 2000 and 2020. Currently, India’s startup ecosystem is responsible for contributing $100 billion to the country’s economy. This contribution is driven by public investments in digital infrastructure and laws that are favorable to startups. Pakistan is able to follow a similar path by establishing key performance indicators (KPIs) in the budget for the fiscal year 2025–2026. These KPIs include the creation of one million new formal employment, the reduction of the regulatory burden on small and medium-sized enterprises (SMEs) by 50%, and the expansion of exports by 20%.

This budget must not be an accounting exercise. It must be a growth manifesto.

Dr. Nasir Iqbal is an Associate Professor at Pakistan Institute of Development Economics (PIDE) specialising in areas of Social Protection, Governance and Poverty. He is also serving as the Registrar at PIDE.