Corporate Governance in the State-Owned Electricity Distribution Companies

NEPRA has approved the detailed design and implementation plan of Competitive Trading Bilateral Contract Market (CTBCM) of electricity, to be implemented in a year. The model envisages that all future contracts for the sale/purchase of electricity will be bilateral between the parties: sellers (generation companies) and buyers (distribution companies or bulk power consumers). But for a competitive electricity market, we need an efficient and financially viable distribution sector first, where a well-developed corporate governance system could be the solution.

-

INTRODUCTION

In electric power systems, the financial health of the distribution sector is critical. A financially weak distribution company can weaken the flow of funds in the entire supply chain, and their operational limitations can lead to the wastage of energy resources. There is a shortfall between cash inflows and outflows in the power supply chain of Pakistan—circular debt. In FY-2020, more than 50 percent of arrears were due to low bill recoveries and the difference between the allowed and actual distribution losses by NEPRA (Malik, 2020).

Apart from sectoral policy issues, the power distribution sector challenges, including institutional weaknesses, centralized control (under the Ministry of Energy-Power Division), and weak corporate governance, are mainly responsible for the circular debt.

-

STRUCTURE OF ELECTRICITY DISTRIBUTION SECTOR

After the formal bifurcation of WAPDA in November 2007, eight separate distribution companies (DISCOs) (which later increased to ten) were established. KESC (now K-Electric (K-El)) remained vertically integrated; in December 2005, it was privatised—the government sold 73 percent of its shares to a private conglomerate. These companies are distributing electricity to the end-consumers in their respective geographical areas as a monopoly.

2.1. Issues in the Distribution Sector

Operational Efficiency

During FY 2021, almost a fifth of the electricity generated in the country was lost in the transmission and distribution (T&D) network (including K-Electric losses). There is an enormous variation in performance across state-owned distribution companies (Chart 1).

On the other side, when a certain percentage of these losses are not accounted for in tariffs, it adds to the circular debt as it is not compensated by tariff differential subsidy. NEPRA is using this T&D target as a tool to improve the operational performance of distribution companies. However, this strategy is not working for most of the DISCOs. There is no penalty associated with utility mismanagement which leads to operational inefficiency.

_________________________________

The author is grateful to Tahir Basharat Cheema, Former MD, PEPCO for his valuable comments and suggestions on the initial draft of this brief.

Commercial Efficiency

Commercial Efficiency

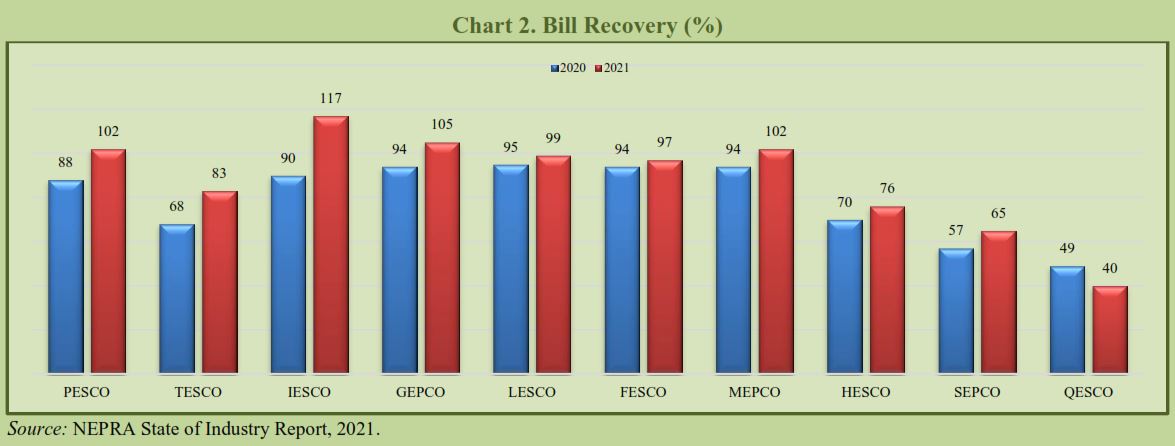

The revenue collection rates in distribution companies range from 40 percent in QESCO to 117 percent in IESCO in FY 2021 (Chart 2). On average recovery percentage of all DISCOs was around 97 percent in FY 2021, despite more than 100 percent collection in IESCO, PESCO, and GEPCO. With the same collection rate for other DISCOs, the average may not remain the same next year. For instance, bill recovery of 117 percent in IESCO is due to a one-time deposit of AJK arrears by the Government of Pakistan. Otherwise, the actual recovery in IESCO in FY2021 was roughly 89 percent.

Generally, the distribution companies with high system losses also suffer from low recoveries of the billed amount. In other words, there are more leakages in geographical areas via fraud (meter tampering), stealing (illegal connections), and billing irregularities; there is also less willingness to pay for the power consumed.

Despite a significant improvement in bill recoveries in FY 2021, the receivables from DISCOs in FY 2021 increased by Rs. 63.7 billion, which accumulated as circular debt (NEPRA, 2021).

Unreliable Supplies

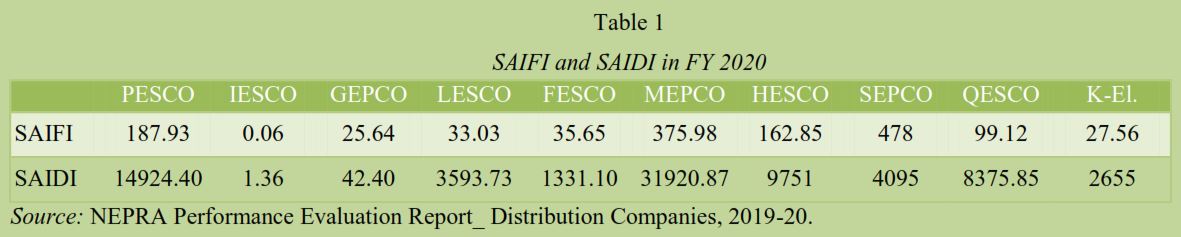

Despite the increase in the installed capacity in the reliability of electricity supply, Pakistan is still ranked 99 out of 141 economies in the Global Competitiveness ranking of 2019. According to Rule 4 (a) of Performance Standards (Distribution) Rules 2005, a distribution company shall ensure that the System Average Interruption Frequency Index (SAIFI) does not exceed 13 and System Average Duration Index (SAIDI) does not exceed 14. Except for IESCO, none of the DISCO satisfies this criterion (Table 1).[1]

______________________________

[1] SAIFI and SAIDI are the least focussed areas in NEPRA priorities.

Instead of correcting for their failures in minimizing inefficiencies, DISCOs have adopted a policy of revenue-based load-shedding. The low-cost and uninterrupted power supply (solar) is taking compliant consumers away from DISCOs (NEPRA, 2020). If this trend continues, it will be another big challenge for the cash-starved DISCOs.

Instead of correcting for their failures in minimizing inefficiencies, DISCOs have adopted a policy of revenue-based load-shedding. The low-cost and uninterrupted power supply (solar) is taking compliant consumers away from DISCOs (NEPRA, 2020). If this trend continues, it will be another big challenge for the cash-starved DISCOs.

-

CORPORATE GOVERNANCE

Corporate governance defines the rights and responsibilities of a board, managers, shareholders, and other stakeholders. It outlines rules and procedures for making decisions (Haque and Hussain, 2021). Corporate governance of the utility—private or state-owned is crucial for its effective operations. Its mechanisms such as monitoring, Board of directors, and executive plans are significant (Gunay, 2016). Developing any state-owned company as a modern corporate entity may help improve its proficiency via regular monitoring and accountability of its managers, transparent information, and decreased political interference in its matters (Vagliasindi, 2008). The autonomy and capability of board members are vital.

DISCOs lack technical and managerial skills to operate independently.[2] The structure of these companies based on corporate governance principles has not been established. Poor corporate governance is the main reason behind the poor technical and financial performance of DISCOs. Zhang (2019) finds significant potential to reduce losses through better management in DISCOs in Pakistan.

Weak administrative performance in DISCOs is due to centralized control. All of the ten DISCOs are under the administrative control of the Ministry of Energy (Power Division). There is no incentive to improve performance as there is no penalty associated with weak performance. Not only there is an absence of transparency in investment decisions, but no merit-based staff performance evaluation and promotion. Promotions are based on seniority. All decisions about finance, employment, and pricing are not without government (political) intervention.

3.1. Financial Performance and Business Model

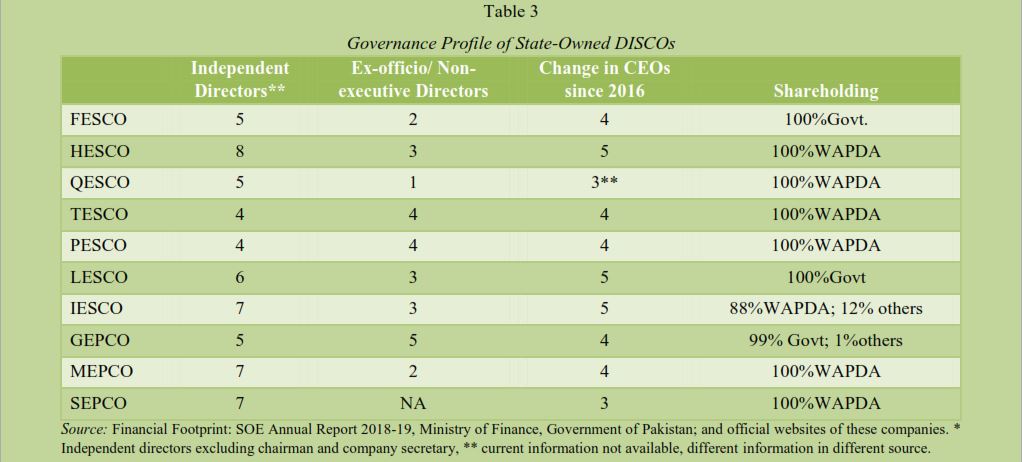

Between FY 2015 to FY 2019, total assets of DISCOs have increased by 7.5 percent. A maximum increase was recorded in LESCO, almost 12 percent. The asset base of these ten state-owned distribution companies was roughly Rs 2 trillion in FY 2019, equivalent to about 5 percent of current GDP in the same year. However, the involvement of these DISCOs in the stock business is zero, as none of them is a listed company. Except for IESCO, in all DISCOs, either Government of Pakistan or WAPDA is a 100 percent shareholder. In IESCO, 12 percent of shares belong to Employee Trust Fund since FY 2014-15 (transferred under Benazir Employees Stock Option Scheme) previously owned by WAPDA (Table 3).

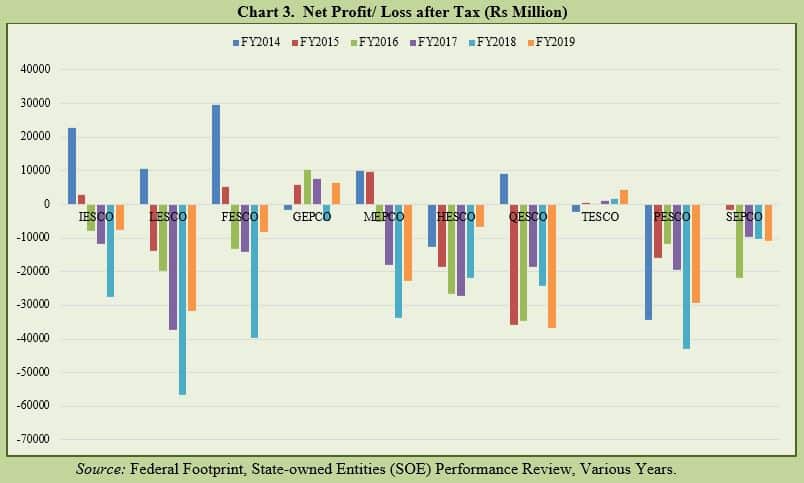

There is no business model followed in these companies. The level of strategic planning and business model is evident in Chart 3. These companies, on average, recorded a net loss of Rs 143 billion in FY 2019. The net loss has increased by 18 percent in the last five years. A corporate governance system guides and operates companies to yield high financial performance (MacMillan and Downing, 1999). Unfortunately, it is missing in DISCOs.

______________________________

[2] As reported by Former MD PEPCO, in PIDE webinar on “Reforming Electricity Distribution Companies”.

3.2. Board of Directors

According to SECP Public Sector Companies (Corporate Governance) Rules, 2013, it is mandatory for each company to have independent directors—40 percent of its total members. On paper, each of these DISCOs has independent board members but with limited authority to make decisions.[3]

As per the Companies Act 2017, and SECP Public Sector Companies (Corporate Governance) Rules, 2013, it is the prerogative of the government to appoint a Board of Directors (BOD) after satisfying the ‘Fit and Proper Criteria’. But in the appointment of DISCO board members, rules are generally not followed. Political interference in board appointments is also common.

For instance, in the last seven months, new boards are appointed in all the ten DISCOs. As reported in newspapers, in the selection process, the Power Division relied on their enlistment as Independent Directors with the Pakistan Institute of Corporate Governance (PICG), their CVs, and an affidavit from each proposed nominee that they fulfill the ‘Fit and Proper Criteria’ as required under the law and rules. While going through the profile[4] of these independent directors, wherever available, we find that the actual practice is different from what was stated in the papers.

Some facts about current boards are below:

- Until the recent past, except for TESCO, each DISCO has its BOD with independent directors. Now it is decided that the PESCO BOD will also function as the TESCO BOD.

- Each DISCO has four or more independent directors.

- Out of the total 40 independent directors, only 3 are PICG certified directors.[5]

- Out of the ten appointed chairmen, none of them is a PICG certified director. At least five of them are ex-employees of a privatized distribution company, K-electric. Others include a professor, a general manager of a manufacturing company, an ex-employee of hydro IPP, and a power sector consultant.[6]

- In the selection of independent directors, the focus seems to be on those with K-electric experience. Including chairpersons, in total, ten independent directors remained affiliated with K-electric in various capacities. In addition, consultants (energy or otherwise) are given preference in the selection.[7]

- In each Board, there is civil society representation (2 to 3 members).

- 11 Directors are on the Board of 2 DISCOs, and one of them is on three boards.

- Board chairman is appointed against the Corporate Governance rules, 2013 which states that the chairman to be elected by the Board to achieve an appropriate balance of power, increasing accountability, and improving the Board’s capacity to exercise independent judgment; but in these DISCOs, the chairman is appointed by the government.

- CEO is appointed by the government against the rules, which state, CEO is to be appointed by the Board. Besides, as informed by various utilities, all major decision-making remained with the As is evident from the minutes of the board meetings,[8] the meetings only discuss human resource-related issues.

_________________________________

[3] These companies are under full government control; board and management positions at DISCOs are held either by government employees or political appointees with limited experience. Officials sitting on multiple energy boards aggravate this issue.

[4] As of September 6, 2021, a detailed profile of GEPCO, HESCO, SEPCO, QESCO and MEPCO board members is not available. Only names are posted. As per law, the companies are required to publish these details in their annual reports. But publishing Annual reports is not a practice in the majority of these DISCOs.

[5] Apart from the personal affiliations of selectors, the fee they are paid (meeting attendance fee) could be the reason for not finding truly independent professionals to be on DISCO boards. The director fee is an issue in companies other than the power sector as well (Ameer, 2013).

[6] The identity of the QESCO board chairman is not clear.

[7] As reported in newspapers, the reliance on K-electric employees is to prepare for future privatisation of these companies.

[8] This information is extracted from newspaper clippings, studies, informal discussions with some DISCO officials, etc.

3.3. Transparency

Transparency is one of the basic principles to ensure a sound governance framework in any organization or company, both in the public and the private sector. Transparency is only possible when information on commercial and non-commercial operations and financial results are timely available for evaluation, not only to the government but also to the public.

- None of the ten DISCOs publishes its Annual Company Report except for FESCO, MEPCO, and IESCO. Even the latest available for MEPCO and FESCO is for 2019, and for IESCO, it is for 2013.

- The latest financial statement (FY 2020) is publicly available only for IESCO, FESCO, MEPCO and GEPCO. For the rest of the DISCOs, a publicly available financial statement is two to four years old.

- Only MEPCO publishes details of its board meetings in its Annual Report, that is number of meetings, etc. It is the only DISCO, with minutes of meetings posted on its website.

- Each DISCO has a website but with limited information on corporate matters.

- Each DISCO does post names of directors on their websites, but as of September 08, 2021, only IESCO, LESCO, FESCO, PESCO have shared profiles of their board members.

3.4. Monitoring and Accountability

Another principle of good corporate governance is accountability. Accountability can be ensured, when managerial performance and the role of independent boards are evaluated by the parliament, public, and the shareholders. But in the case of DISCOs, none of these is listed on any stock exchange of Pakistan; therefore, no accountability by shareholders. The boards have never been empowered to make decisions. At the same time, they are not held accountable. This trait is common in other Pakistani companies—the Board of directors does not consider them accountable for what they do (Aziz, et al. 2019).

CEOs have been changed quite frequently in these DISCOs (Table 3) and not for the sake of accountability.[9] For instance, the recently appointed CEO at IESCO has previously served at PESCO. PESCO performance is evident in Chart 1 to Chart 3 and Table 1 and Table 2.

Cash injections by the successive government have impeded the efforts of power companies to improve their governance, efficiencies and reduce their losses. Whenever the power companies face problems, the government extended financial help either through subsidies or by increasing tariffs, resulting in more inefficiencies. Lack of expertise in the form of financial and commercial skills is a serious impediment in accountability, quick decision-making, and commercial orientation. Defaults are now a routine matter.

-

WAY FORWARD

- Outright privatization may not be a solution. It might increase the financial burden of the government.

- Mandate listing of DISCOs in the stock exchange and appoint principal shareholders on the Board.

- Sell a certain percentage of shares to DISCO employees and give them representation on the Board.

- Facilitate a corporate culture in DISCOs with a viable business model as also envisaged in the National electricity policy-2021. Each company needs its business model based on its domestic market conditions.

- An independent/ apolitical board with professional directors (power sector specialists) with sufficient capabilities to develop a business model. It should be mandatory for the power sector professionals to get trained from an institute like PICG to qualify as independent directors. Once these directors are appointed, they must have the power to make decisions. In addition, hold them accountable for their decisions.

- For increasing transparency and accountability, a well-designed website of each authority. Minutes of each board meeting or at least major decisions should be publicly available. Their annual reports, as well as financial statements, should be timely available for public scrutiny.

- There should not be any conflict of interest for the government as owner as well as a policymaker. The government should only be a facilitator and can play its role by improving the business environment by enforcing contracts, improving laws, and simplifying tax administration.

- Professional and competitive management having a clear corporate vision and business plans for organizing the utility on commercial lines. These professionals must have the capacity to develop a comprehensive revenue collection and theft prevention program in their respective companies.

_________________________

[9] CEOs are normally appointed when they are about to retire.

REFERENCES

Aziz, M., Gondal, Z. H. and Ali, S. (2019). Problem Relating to Corporate Governance in Pakistan. Research Advances in Social Sciences Journal, 6 (6), 353-358.

Castro, N. J., Soares, I., Rosentel, R. and Sellare A. J. (2010). Impact of Corporate Governance on Companies in Brazil’s Electricity Sector. TDSE No 24, GESEL, Institute de Economia.

Dube, I. and Jaiswal, N. (2015) Corporate Governance in the Energy Sector. Journal Global Law Review, 6(2), 143-178.

Fremeth, A. R. and Holburn, G. L. F. (2018). Corporate governance of publicly-owned electric utilities: Survey evidence from Ontario’s municipally owned distribution companies. Ivey Business School University of Western Ontario, Canada.

Gassner, K., Popov, A., & Pushak, N. (2009). Does Private Sector Participation Improve Performance in Electricity and Water Distribution? Trends and Policy Options No. 6, Public-Private Infrastructure Advisory Facility, The World Bank, Washington D.C.

Gunay, G. Y. (2016). The test of corporate governance system in electricity utilities industry. Journal of Management and Sustainability, 6(1), 132–140.

Haque, N. and Hussain, A. (2021). A Small Club: Distribution, Power and Networks in Financial Markets of Pakistan. (PIDE Working Paper 2021:3).

Irwin, T and Yamamoto, C. (2004). Some Options for Improving the Governance of State-Owned Electricity Utilities. Energy and Mining Sector Board Discussion Paper Series No. 11, The World Bank, Washington D.C.

Liu, Y., Miktkor, M.K., Wei, Z. and Yang T. (2015). Board independence and firm performance in China. Journal of Corporate Governance, 35, 223–244.

MacMillan, K. & Downing, S. (1999). Governance and performance: Goodwill hunting. Journal of General Management. https://doi.org/10.1177/030630709902400302

Malik, A. (2020). Circular debt: An unfortunate misnomer. PIDE. (PIDE Working Paper Series 2020:20).

Sheveleva, G. I. (2018). Corporate governance in Russian electric power industry in terms of consumer requirements to its funding sources. https://doi.org/10.1051/e3sconf/20185802004

Srivastava, G. and Kathuria V. (2020). Impact of corporate governance norms on the performance of Indian utilities. Energy Policy, 140, https://doi.org/10.1016/j.enpol.2020.111414

Vagliasindi, M. (2008). Governance Arrangements for State Owned Enterprises. The World Bank, Washington D.C. (Policy Research Working Paper 4542).

Wei, G. (2007). Ownership structure, corporate governance and company performance in China. Asia Pacific Business Review, 13(4), 519-545.

Zhang, F. (2019). In the dark: How much power sector distortion costs South Asia? South Asia Development Forum, International Bank for Reconstruction and Development, The World Bank, Washington, D.C.