Debt Sustainability: Economic Growth is the Panacea

Abdul Jalil, Professor of Economics, Pakistan Institute of Development Economics, Islamabad.*

Early development theory focused on the need for debt and foreign exchange, arguing that developing countries need external funds since they cannot generate adequate resources domestically to achieve economic growth to improve their livelihood.The borrowing addiction has led to repayment difficulties opening up concerns for debt sustainability (see Box 1).

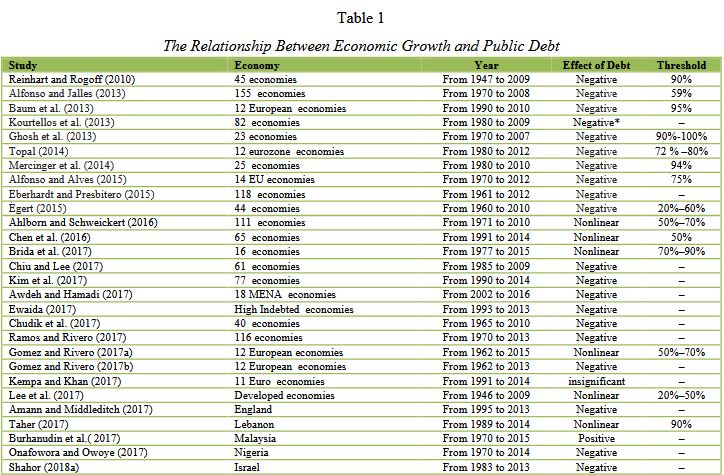

Therefore, the debt-growth nexus remains a widely discussed issue in the empirical literature. Mainly, Reinhart and Rogoff (2010) got colossal attention in this regard, which claimed that a debt to GDP ratio, which is higher than 90 %, negatively hurts economic growth. Though some research also challenges the Reinhart and Rogoff claim (2010).

This knowledge brief reviews the empirical studies on debt-growth nexus since 2010 to evaluate Reinhart and Rogoff (2010) claim that high debt to GDP ratio negatively impacts economic growth or vice versa. We shall also simulate the threshold level of economic growth for a sustainable debt to GDP ratio in Pakistan’s case.

| Box 1: What is Debt Sustainability? The countries incur debt due to the shortage of local resources. In case of debt burden of country how much is too much depends on the debt sustainability of that country. When a country is able to meet all its payment obligations, current and future, without taking exceptional finances from the external resources without being default is known as debt sustainable country. The sustainability of the debt depends on the number of factors like the quality of institutions, debt management capacity and macroeconomic fundamentals, that is, economic growth. |

- DEBT AND ECONOMIC GROWTH: TWO DECADES OF STUDIES

The empirical literature can be divided into three main categories: linear negative relationship, positive linear relationship, and nonlinear relationship.

Linear positive relationship implies that a country grows as the level of debt increases. Theoretically, it is an ideal condition since the economy can increase debt to encounter their developmental goals, such as developing their physical and human infrastructure. Conversely, a negative link guides that an economy’s growth declines when it increases its public debt. When the debt may affect both positively and negatively, then it is known nonlinear relationship.

__________________________

Acknowledgement: My thanks to Nadeem UI Haque for suggesting the topic and his guidance through the project. I am also thankful to Durr-e-Nayab and Mahmood Khalid for their comments and suggestions on an earlier draft of the paper. Errors of course remain the responsibility of the author.

Four main conclusions can be drawn from the review of the literature (see Table 1).

- The majority of the articles posit that there is a negative linear association between debt and economic growth regardless of the types of debt and level of the countries’ income. This finding is in line with the theory of debt-growth nexus (See Box 2).

- Burhanudin et al. (2017) and Gomes and Rivero (2017a) find a positive link between debt and growth in the short run.

- There is no magic number of a threshold level of the debt. It may vary from 15% to 2000% (Pegkas 2018 and Butkus and Seputiene, 2018 for details).

- The literature further suggests that the tax rate increase to substitute the debt will not make a reasonable attempt in lower-income countries. However, improvement in the economic environment to create an investment-friendly environment is suggested.

2. DEBT SUSTAINABILITY IN PAKISTAN: SOME SIMULATIONS

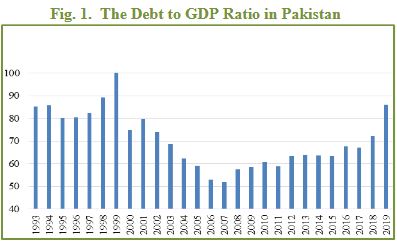

The debt to GDP ratio has continuously increased in Pakistan’s last ten years (see Figure 1). Therefore, the question of debt sustainability is quite relevant here. Notably, we need to understand how the debt to GDP ratio will remain in a manageable range. The Fiscal Responsibility and Debt Limitation (FRDL) act suggests that the debt should remain around 60 percent of the GDP.

| Box 2: The Theory on Negative Linear Relationship There are three main explanations of the negative linear relationships between debt and economic growth. Crowding Out Effect: Elmendorf and Gregory (Mankiw, 1998) document that the high public debt crowd out the private investment. This is the most conventional explanation that increase the government borrowing will elevate the interest rates which crowd out the private investment and ultimately will hit the economic growth. Overlapping Generation Models (OLGMs) also explain the lower economic growth due to higher public debt (see Modigilani 1961, Diamond 1965 and Blanchard 1985). According to the OLGMs, the increase in public debt consume the savings which are supposed for the coming generations. The reduction in saving may raise the interest rates. This may discourage the future investment which lead to lower economic growth. Debt Overhang explains that the debt overhang happens when a country has higher accumulated debt level than net present value of national income. Krugman (1988) notes that this happens due to inefficiently managed borrowed funds. In this situations, most of the indebted countries use the borrowed funds for the repayments of the debts instead of the developmental projects. That’s why they get a negative hit on their economic growth. |

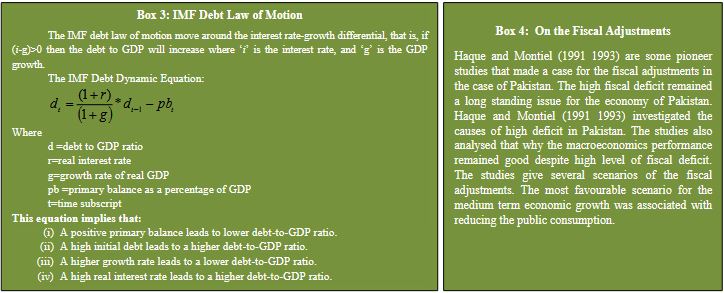

In this regard, the interest rate-growth differential is essential to understand the long-run fiscal sustainability. The higher interest rate implies that higher debt servicing, which adversely affects the debt dynamics. On the other hand, higher economic growth means a lower debt to GDP ratio (see Box 3). Therefore, as long as the cost of borrowing is less than the economic growth, the debt burden will not rise. Consequently, debt sustainability will be questionable in lower economic growth and high-interest rate environment in Pakistan (see . Box 4).

We develop several scenarios, based on some assumptions, to evaluate the case of Pakistan. More clearly, what should be the threshold level of economic growth to be solvent.

2.1. Assumptions and Scenarios

Assumptions

- The real interest is taken as a historical average, which is equal to around 1.5 percent.

- The initial value of the public debt to GDP ratio is 86 for 2019.

- The population growth rate is zero.

Scenarios

- We develop three scenarios for primary balance (see Box 5).

(a) Baseline Scenario: when the primary balance is zero.

(b) Historical Scenario: when the primary balance is –2.2, which is the average of the last ten years.

(c) Most Extreme Scenario: when the primary balance is –4.3, which is the historic high of the last ten years.

- We develop three scenarios for GDP growth.

(a) When GDP growth is 1.5, which is equal to the historical average interest rate.

(b) When GDP growth is 4.5, which is the average for the last 20 years.

(c) When GDP growth is 10 percent, which is the historic high of the last 20 years plus population growth.

| Box 5 : Primary Balance (PB) The PB is the difference between revenues of the government and its non-interest expenditure. When the primary balance is negative, that is, when revenues are less than non-interest expenditure, that can also be referred to as a primary deficit. IMF approved Extended Fund Facility (EFF) in July 2019 and a strong fiscal consolidation of 4.5 % of GDP in primary balance over is suggested for the sustainable public debt. |

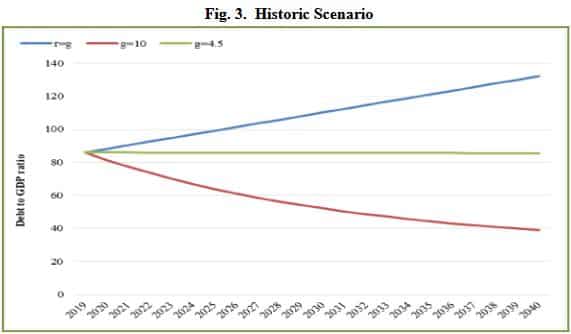

2.2. The Threshold Level of GDP Growth Rate in Three Different Scenarios

Base Line Scenario: When Primary Balance is Zero.

- When the primary balance is zero, the real interest rate threshold level is equal to the real interest rate. This implies that the Debt to GDP ratio will not increase from the existing point when the growth rate is equal to the real interest rate.

- When g>r, then the debt to GDP growth rate will start decreasing.

- Suppose the GDP grows at 4.5 percent, which is the average of the last 20 years, then the debt to GDP ratio may reach 60 percent by 2031, which is suggested by FRDL.

- The FRDL suggested limit for debt to GDP ratio may be achieved more rapidly with 10 percent GDP growth when the primary balance is zero.

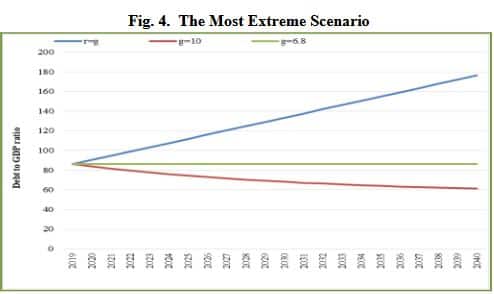

Historic Scenario: When Primary Balance is –2.2.

The debt to GDP ratio will worsen in the case of a negative primary balance. The GDP growth must be equal to 6.6 percent, the average of last twenty years 4.5 plus population growth 2.1, to maintain the current debt to GDP ratio.

Most Extreme Scenario: When the Primary Balance is –4.3.

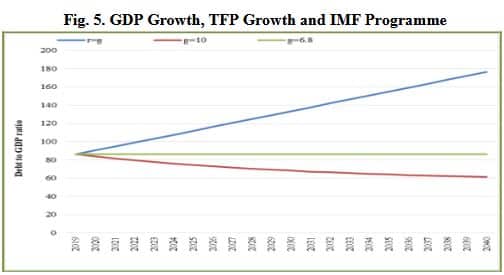

- If we consider the most extreme scenario, then the threshold level of economic growth is 6.8 percent plus population growth (roughly 8.9 percent) to maintain the current level of Debt to GDP ratio. The FRDL limit, which is 60 %, will be achieved in 2040 with a 10 percent GDP growth.

CONCLUSION

The evidence presented here reinforces the age-old principles.

- We see overwhelming evidence from the literature that there is a negative relationship between debt and economic growth.

- The cardinal principle for incurring debt remains that the expected growth rate must be higher than both payments and additional debt incurred. In other words, debt should lonely be used for high quality, high return investments?

Pakistan’s debt difficulties are longstanding, as our repeated use of IMF facilities shows. We have had about three reschedulings in our history. The policy seems to be debt hungry, even if it means adopting stabilisation policies that reduce growth. Both economic growth and productivity are low and declining (see Figure 5; black Dots are IMF programmes in the corresponding year).

As pointed out in Haque (Haque 2020a and Haque 2020b ), the policy continues to follow the Haq/HAG model to build low return ‘brick and mortar’ projects on borrowed funds. There is no policy or framework for maximising returns on assets created or better project selection through precise cost-benefit analysis or tighter control on project expenditures. Not only does debt grow because of this policy, growth, and productivity decline too.

As pointed out by Haque ( Haque 2020a and Haque 2020b, Haque 2017a and Haque 2017b) as well as the Framework of Economic Growth 2011, the policy has not yet adopted the Lucas-Romer endogenous growth approach that would prioritise reform of institutions and the business environment for accelerating growth.

Our simulations and calculations show that the only way out of the debt difficulties that Pakistan has been in for the last 40 years has to be a strong growth acceleration. We urge the government to adopt a new growth strategy based on a market-friendly, investment-friendly, and transaction friendly environment. PIDE is actively engaged in developing one.

REFERENCES

Ahlborn, M., and Schweickert, R. (2016). Public debt and economic growth – Economic systems matter. International Economics and Economic Policy, 15(2), 373–403.

Alfonso, A. and Jalles, J. T. (2013) Growth and productivity: The role of government debt. International Review of Economics & Finance, 25, 384–407.

Alfonso, A., and Alves, J. (2015). The role of government debt in economic growth. Hacienda Pública Española, 215(4), 9–26.

Amann, J., and Middleditch, P. (2017). Growth in a time of austerity: Evidence from the UK. Scottish Journal of Political Economy, 64(4), 349–375.

Arcabic, V., Tica, J., Lee, J., and Sonora, R. J. (2018). Public debt and economic growth Conundrum: Nonlinearity and inter-temporal relationship. Studies in Nonlinear Dynamics and Econometrics, 22(1), 1–20.

Awdeh, A, and Hamadi, H. (2017). Factors hindering economic development: Evidence from the MENA countries. International Journal of Emerging Markets, 14(2), 281–299.

Baum, A., Checherita-Westphal, C., and Rother, P., (2013). Debt and growth: New evidence for the Euro area. Journal of International Money and Finance, 32(C), 809–21.

Blanchard, O. (1985). Debt, deficits, and finite horizons. Journal of Political Economy, 93(2), 223–247.

Brida, J. G., Gomez, D. M., and Seijas, M. N. (2017). Debt and growth: A non-parametric approach. Physica A: Statistical Mechanics and Its Applications, 486, 883–894.

Burhanudin, M. D. A., Muda, R., Nathan, S. B. S., and Arshad, R. (2017). Real effects of government debt on sustainable economic growth in Malaysia. Journal of International Studies, 10(3), 161–172.

Butkus, M., and Seputiene, J. (2018). Growth effect of public debt: The role of government effectiveness and trade balance. Economies, 6(4), 62.

Chen, C., Yao, S., Hu, P., and Lin, Y. (2016). Optimal government investment and public debt in an economic growth. China Economic Review, 45, 257–278.

Chiu, Y, and Lee, C.-C. (2017). On The Impact of Public Debt on Economic Growth: Does Country Risk Matter? Contemporary Economic Policy, 35(4), 751–766.

Chudik, A., Mohaddes, K., Hashem Pesaran, M., & Raissi, M. (2017). Is there a debt-Threshold effect on output growth? Review of Economics and Statistics, 99(1), 135–150.

De Vita, G., Trachanas, E., and Luo, Y. (2018). Revisiting the Bi-directional causality between debt and growth: Evidence from linear and nonlinear tests. Journal of International Money and Finance, 83, 55–74.

Diamond, P. A. (1965). National debt in a neoclassical growth model. The American Economic Review, 55(5), 1126–1150.

Eberhardt, M. and Presbitero, A. F. (2015) Public Debt and Growth: Heterogeneity and Non-linearity. Journal of International Economics 97, 45–58.

Elmendorf, D. W., and Mankiw, G. N. (1998). Government debt (pp. 6470). Cambridge: National Bureau of Economic Research.

Egert, B (2015). Public debt, economic growth and nonlinear effects: Myth or reality? Journal of Macroeconomics, 43, 226–38.

Esteve, V., and Tamarit, C. (2018). Public debt and economic growth in Spain, 1851–2013. Cliometrica, 12(2), 219–249.

Ewaida, H. Y. M. (2017). The impact of Sovereign debt on growth: An empirical study on GIIPS versus JUUSD countries. European Research Studies Journal, 20(2), 607–633.

Gomez-Puig, M., and Sosvilla-Rivero, S. (2017a). Public debt and economic growth: Further evidence for the Euro area Working Papers Del Instituto Complutense de Estudios Internacionales 1709. Madrid.

Gómez-Puig, M., and Sosvilla-Rivero, S. (2017b). Heterogeneity in the debt-growth nexus: Evidence from EMU countries. International Review of Economics and Finance, 51, 470–486.

Gómez-Puig, M., and Sosvilla-Rivero, S. (2018a). On the Time-varying nature of the debt-growth nexus: Evidence from the Euro Area. Applied Economics Letters, 25(9), 597–600.

Gómez-Puig, M., and Sosvilla-Rivero, S. (2018b). An investigation of nonlinear effects of debt on growth. Journal of Economic Asymmetries, 18, 1–13.

Ghosh, Atish R., Jun I. Kim, Enrique G. Mendoza, Jonathan D. Ostry, and Mahvash S. Qureshi, (2013), Fiscal Fatigue, Fiscal Space and Debt Sustainability in Advanced Economies. Economic Journal, 123(566), F4–F30.

Haque , N. (2017a) Macroeconomic Research and Policy making Processes and Agenda. Mahboob-ul-Haq Lecture 33rd AGM of Pakistan Society of Development Economics. https://www.pide.org.pk/psde/pdf/Lectures/Mahboob-ul-Haq-Lecture/Mahbub-ul-Haq%20Lecture-33rdAGM.pdf

Haque, N. (2017b) Looking back: How Pakistan became an Asian tiger by 2050. KITAB; 1st Edition.

Haque , N.(2020a) Doing development better: Analysing the PSDP. The Pakistan Development Review, 59(1), 139–142.

Haque, N. (2020b) Enough “Bricks and Mortar”!. PIDE Blog https://pide.org.pk/blog/enough-brick-and-mortar/

Haque, N. and Montiel, P. (1991). The macroeconomics of public sector deficits: The case of Pakistan. (World Bank Working Paper No. 673).

Haque, N. and Montiel, P. (1993). Fiscal adjustment in Pakistan: Some simulation results. Staff Papers (International Monetary Fund). 40, 471-480.

Karadam, D. Y. (2018). An investigation of nonlinear effects of debt on growth. Journal of Economic Asymmetries, 18, 1–13.

Kempa, B., and Khan, N. S. (2017). Spillover effects of debt and growth in the euro area: evidence from a GVAR model. International Review of Economics and Finance, 49, 102–111.

Kim, E., Ha, Y., and Kim, S. (2017). Public debt, corruption and sustainable economic growth. Sustainability, 9(3), 433.

Kourtellos, A., Stengos, T., and Tan, C. M. (2013). The effect of public debt on growth in multiple regimes. Journal of Macroeconomics, 38, issue PA (2013): 35–43.

Krugman, P. (1988). Financing vs forgiving a debt overhang. Journal of Development Economics, 29(3), 99–104.

Lee, S., Park, H., Seo, M. H., and Shin, Y. (2017). Testing for a debt-threshold effect on output growth. Fiscal Studies, 38(4), 701–717.

Liaqat, Z. (2019). Does government debt crowd out capital formation? A dynamic approach using panel VAR. Economics Letters, 178, 86–90.

Maitra, B. (2019). Macroeconomic impact of public debt and foreign aid in Sri Lanka. Journal of Policy Modelling, 41(2), 372–394.

Mercinger, J., Aristovnik, A., and Verbic, M. (2014). The impact of growing public debt on economic growth in the European union. Amfiteatru Economic 16(35), 403–14.

Mhlab, N., and Phiri, A. (2019). Is public debt harmful towards economic growth? New evidence from South Africa. Cogent Economics and Finance, 7(1).

Modigliani, F. (1961). Long-run implications of alternative fiscal policies and the burden of the national debt. Economic Journal, 71(284), 730–755.

Pegkas, P. (2018). The effect of government debt and other determinants on economic growth: The Greek experience. Economies, 6(1), 10.

Pegkas, P. (2019). Government debt and economic growth: A threshold analysis for Greece. Peace Economics, Peace Science and Public Policy, 25(1), 1–7.

Ramos-Herrera, M. C, and Sosvilla-Rivero, S. (2017). An empirical characterisation of the effects of public debt on economic growth. Applied Economics, 49(35), 3495–3508.

Reinhart, Carmen M., and Kenneth S. Rogoff. (2010). Growth in a time of debt. American Economic Review, 100(2), 573–78.

Shahor, T. (2018). The impact of public debt on economic growth in the Israeli economy. Israel Affairs, 24(2), 254–264.

Snieska, V., and Burksaitiene, D. (2018). Panel data analysis of public and private debt and house price influence on GDP in the European Union countries. Engineering Economics, 29(2), 197–204.

Taher, H. (2017). The impact of government debt on economic growth: An empirical investigation of the Lebanese market. International Journal of EuroMediterranean Studies, 10(1), 23–41.

Topal, P. (2014). Threshold Effects of Public Debt on Economic Growth in the Euro Area Economies. (Working Paper, 2014).