Executive Summary

The European Union–India Free Trade Agreement (FTA), signed on January 27, 2026, marks a strategic development in the global political economy. The agreement offers tariff reductions, thereby facilitating greater access of Indian exports to the EU market across a wide range of goods, with limited coverage of agricultural products. In bilateral trade terms, the FTA holds significant implications for economies, including Pakistan, that are considerably dependent on the European Union as a major export destination.

A preliminary analysis based on Computable General Equilibrium (CGE) simulations suggests that India’s exports to the EU could increase by between 21.23% and 33.63% as a result of improved market access and its larger production base. In absolute terms, this translates into an estimated additional export gain of approximately USD 16.7–26.5 billion. Part of this increase would arise from trade diversion away from competing exporters. For Pakistan, exports to the EU are projected to decline by between 0.12% and 0.18% in the short term, equivalent to a modest reduction of roughly USD 11–16 million.

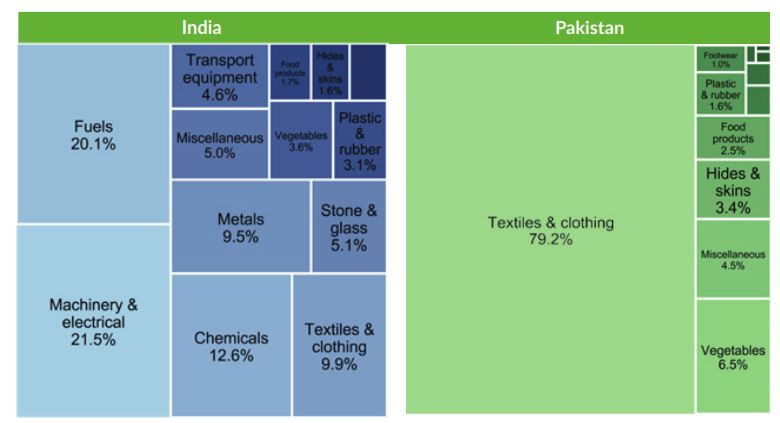

Over the past decade, 17–21% of India’s total exports were directed to the EU. India’s export basket to the EU is broad and increasingly tilted toward higher-value sectors. Electrical and mechanical equipment together account for more than one-fifth of India’s EU-bound exports, alongside chemicals, fuels, metals, and textiles and clothing. This diversified base positions Indian producers well to benefit from tariff reductions and regulatory cooperation under the new agreement.

By contrast, during the past decade, Pakistan’s exports to the EU accounted for around 30–34% of its total exports. Pakistan’s exports to the EU remain concentrated in a narrow range of products. Critically, nearly 80 % of Pakistan’s EU-bound exports consist of textiles and apparel alone. This concentration turns any shift in relative market access in Europe into a sector-level structural competitiveness challenge.

In the sum total of EU’s imports of textiles and apparel from non-EU countries, China accounts for 19.91 %, followed by Bangladesh (11.53%), Turkey (7.61%), India (3.81%), Pakistan (3.54 %), and Vietnam (3.16%). Pakistan currently receives duty-free access to the EU under the Generalized Scheme of Preferences Plus (GSP+), covering around two-thirds of tariff lines. However, this arrangement is granted unilaterally by the EU, thus conditional upon compliance requirements, and is subject to periodic review. The EU–India FTA reduces Pakistan’s tariff advantage in overlapping sectors while providing India with more stable and predictable market access, along with closer regulatory cooperation.

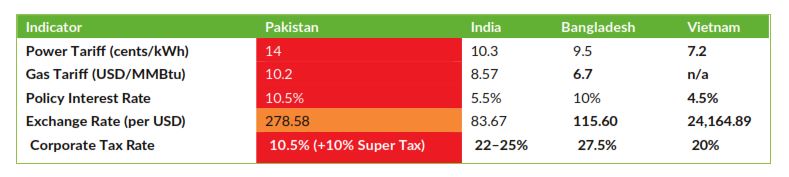

The risks are therefore not purely quantitative but structural. Pakistan enters this new trade environment with a thin competitiveness margin characterized by high electricity tariffs (14 cents/kWh), elevated interest rates (10.5%), taxation complexity, and exchange rate volatility. These constraints limit firm-level upgrading and increase the likelihood that competitive pressure will result in industrial consolidation rather than productivity transformation. Given that the textile sector accounts for over 60% of total exports, nearly 40% of industrial employment, and supports an estimated 15 million jobs, even limited erosion of EU market share could mean concentrated employment uncertainty in key industrial clusters such as Faisalabad, Karachi, and Sialkot.

The EU–India FTA should therefore be taken not as a catastrophic shock, but as a competitiveness test that highlights Pakistan’s structural vulnerabilities. Without timely policy intervention, focused on cost rationalization, export financing, energy reform, and industrial upgrading, Pakistan risks gradual but persistent market share erosion in one of its most critical export markets.

1. Context and Background

The European Union is a key export market for Pakistan, accounting for roughly one-third of total merchandise exports, with access governed not by a bilateral free trade agreement but through the EU’s Generalised Scheme of Preferences Plus (GSP+). Under GSP+, Pakistan enjoys duty-free access on approximately two-thirds of EU tariff lines, a benefit that has underpinned the expansion of textile and apparel exports over the past decade. This preferential access, however, is conditional, time-bound, and subject to periodic political and regulatory review.

Against this backdrop, the conclusion of the EU–India Free Trade Agreement represents a structural change in the competitive environment facing Pakistani exporters. Unlike GSP+, the EU–India FTA provides India with permanent, treaty-based market access, alongside deeper provisions on standards, services, and regulatory cooperation. As a result, Pakistan’s exports to the EU—already highly concentrated in a narrow set of price-sensitive textile categories—now face intensified competition from a regional peer with greater scale, diversification, and supply- chain depth. The agreement therefore interacts with Pakistan’s existing dependence on preferences, rising compliance costs, and internal competitiveness constraints, amplifying the risks of reducing market share even in the absence of any immediate change to GSP+ status.

Pakistan and the EU’s GSP+ Scheme:

| Scope and Benefits | Compliance and Emerging Risks |

| • Coverage: Duty-free access on ~66% of EU tariff

lines • Key Beneficiary Sectors: Textiles and apparel (HS 50–63), leather goods, selected agro- products • Export Dependence: Nearly 80% of Pakistan’s exports to the EU are textiles and clothing • Economic Significance: GSP+ has supported sustained export growth and employment in major industrial clusters (Faisalabad, Karachi, Sialkot) • Nature of Access: Unilateral, conditional, and subject to periodic review by the European Commission |

• Conditionality: Compliance with 27 international conventions covering human rights, labour standards, environment, and governance

• Monitoring: Biennial EU reviews with increasing scrutiny on implementation, not just formal ratification • Political Risk: Heightened sensitivity within the EU to labour rights, environmental compliance, and governance issues • Commercial Implication: Any uncertainty around GSP+ continuity raises buyer risk perceptions and weakens long-term sourcing commitments. On the other hand, EU–India FTA offers India permanent, rules-based access, reducing policy risk for EU importers |

1.1 Comparative Analysis of EU Market Dynamics

The EU serves as a critical destination for both India and Pakistan, though their export trajectories and structures differ significantly. In terms of export growth during the period 2015–2024, India’s exports to the EU doubled from USD 44.7 billion to USD 91.4 billion. During the same period, Pakistan’s exports grew from USD 6.6 billion to USD 11.1 billion. Market Dependency: The EU is disproportionately important to Pakistan, accounting for 30% to 36% of its total global exports, therefore heightening market dependency and placing exports at the whim of EU preferences. For India, the EU accounts for 21% of its global exports.

In terms of structural composition, India is highly diversified across machinery/electrical equipment (21.5%), fuels (20.1%), chemicals (12.6%), and textiles (9.9%). Pakistan on the other hand is narrowly concentrated in textiles and clothing (HS50-63), which represent 79.22% of all EU-bound exports.

1.2 Exposure Analysis: Concentrated Risk Versus Diversified Strength

Pakistan’s reliance on a single sector contrasts sharply with India’s multi-sector resilience, so a shock to textiles is more likely to translate into a system-wide shock, while a diversified portfolio allows India to absorb volatility in a sector.

2. Sectoral Vulnerabilities and Trade Diversion

The primary risk for Pakistan is “preference erosion”. While Pakistan currently enjoys duty-free access under the EU’s GSP+ scheme, the EU–India FTA grants India comparable or superior advantages with greater long-term certainty.

2.1 The Textile and Apparel Conflict

Textiles represent the most intense area of bilateral competition. As of the latest data, Pakistan holds a 3.54% share of total EU textile imports, while India holds 3.81%.

- Overlapping Categories: Pakistan currently leads in made-up textiles (12.86% vs. India’s 6.60%) and cotton (12.75% vs. India’s 10.25%).

- Indian Dominance: India significantly outperforms Pakistan in carpets (10.74% share) and special woven fabrics.

- FTA Impact: Tariff concessions for India are expected to erode Pakistan’s price competitiveness in these overlapping lines, leading global retailers to re-optimize sourcing toward Indian suppliers.

Table 1: Risk Level of Key Pakistan Export Segments to the EU

| Sector | Pakistan EU Market Share | India EU Market Share | Risk Level |

| Total Textiles | 3.54% | 3.81% | HIGH |

| Cotton (HS52) | 12.75% | 10.25% | HIGH |

| Made-up Textiles (HS63) | 12.86% | 6.60% | MEDIUM |

| Carpets (HS57) | 0.51% | 10.74% | LOW |

| Special Woven Fabrics (HS58) | 0.81% | 5.10% | LOW |

2.2 Quantitative Impact Projections

General equilibrium simulations of the EU–India FTA suggest that India’s exports to the EU could increase by approximately 21.23% to 33.63%, depending on the extent of tariff reductions and the easing of non-tariff barriers. These gains are likely to create trade diversion, shifting market share away from competing exporters, including Pakistan. A more rigorous and comprehensive assessment will follow as additional details of the agreement become available.

3. Structural Competitiveness Disadvantages

Pakistan enters this new trade environment from a position of structural weakness. A comparison with regional peers (India, Bangladesh, China, and Vietnam) reveals a “thin competitiveness margin.”

Firms in Pakistan face a variety of constraints, with noteworthy issues in including high input costs and taxation issues. More specifically, in terms of energy costs, Pakistan’s electricity tariff (14 cents/kWh) is the highest in the group, directly inflating unit costs for energy-intensive textile production. Interest rates are nearly double those of India, imposing a financial burden and making it significantly more expensive for Pakistani firms to finance working capital or technological upgrading. While the statutory corporate rate is low, the addition of a 10% Super Tax, withholding taxes, and a weak refund mechanisms create a higher effective tax burden and discourages foreign investment. Frequent and sharp depreciations of the PKR undermine long- term contracting and buyer confidence, particularly in time-sensitive apparel segments.

4. Firm-Level and Macroeconomic Implications

The effects of the EU–India Free Trade Agreement (FTA) on Pakistan’s economy will be felt primarily through three interconnected channels, shaped by the country’s export structure and cost position. Pakistan’s textile and apparel industry, which exports approximately USD 6–9 billion annually to the EU and accounts for close to 40 per cent of Pakistan’s textile shipments, operates in a price-sensitive segment that has historically relied on preferential access under the EU’s GSP+ scheme. Under this arrangement, Pakistan enjoys duty-free access on roughly two- thirds of EU tariff lines, a benefit that has led to export growth since 2014 but remains unilateral, conditional, and subject to compliance with international labour, human rights, and governance standards.

With the FTA granting India near-comprehensive duty-free access to the EU market, Pakistan’s effective tariff margin is largely ended, intensifying competitive pressure in segments where Indian firms benefit from greater scale, deeper vertical integration, and stronger balance sheets. Instead, competitive pressure is expected to reallocate market access toward a subset of larger, vertically integrated firms whose scale, internal financing capacity, and compliance capabilities are aligned with prevailing cost structures and enforcement conditions. Small and medium enterprises, operating with thin margins and limited access to long-term finance, face constrained adjustment options and a heightened risk of exit rather than upgrading.

Pakistan’s labour-intensive textile value chain will enhance these pressures. Even modest declines in exports to EU will impact employment in major production clusters (Faisalabad, Karachi, and Sialkot). At the same time, persistent value-chain constraints, including high energy tariffs and financing costs, limit firms’ ability to upgrade, certify, and also diversify into higher- value segments, leaving many producers locked into low-margin apparel lines where Indian competition is intensifying.

The scale of these risks becomes clearer when Pakistan’s export and employment exposure is quantified. The textile and apparel sector accounts for over 60 per cent of Pakistan’s total merchandise exports and nearly 40 per cent of industrial employment, supporting an estimated 15 million livelihoods directly and indirectly. The EU is Pakistan’s single most important destination, absorbing roughly 27 per cent of total exports, approximately USD 8.8 billion in FY2025, with nearly 90 per cent of textile and apparel shipments entering under duty-free GSP+ preferences. In this context, even limited erosion of market share in the EU can have outsized effects, reinforcing the risks of SME attrition, employment losses, and broader labour-market losses when competitive conditions shift unfavourably.

5. Strategic Recommendations

5.1 Immediate-Term (0–12 Months)

- Liquidity Support: Ensure timely refunds of sales tax and duty drawbacks to ease cash flow constraints for EU-oriented exporters.

- Targeted Financing: Offer time-bound export credit and working-capital facilities through State Bank of Pakistan (SBP) refinance schemes.

- Diplomatic Engagement: Proactively lobby the EU to ensure the uninterrupted and predictable utilization of GSP+ preferences.

5.2 Medium-Term (1–3 Years)

- Energy Rationalization: Prioritize renewable energy expansion and eliminate circular debt to reduce effective electricity and gas tariffs for exporters.

- Regulatory Reform: Streamline customs and logistics procedures to reduce delivery lead times and improve business environment rankings.

- Financial Easing: Gradually reduce policy interest rates while maintaining inflation targeting to lower the cost of industrial upgrading.

5.3. Long-Term (3+ Years)

- Market Diversification: Negotiate a comprehensive bilateral trade deal with the EU to secure long-term market access beyond the GSP+ framework.

- Strategic Integration: Pursue accession to the Regional Comprehensive Economic Partnership (RCEP) to strengthen external competitiveness.

- Industrial Upgrading: Link industrial incentives to productivity improvements and movement into high-value manufacturing segments.

Table 2: Policy Matrix

| Policy Action | LeadInstitution | Time frame | Fiscal Cost | Expected Impact |

| 1. Export Working | Ministry of | 0–12 | Financing for export | Reduces liquidity |

| Capital: Expand | Commerce; | months | sector budgeted at | constraints, lowers |

| concessional export | EXIM Bank; | PKR 539 billion can be | effective financing | |

| financing (Export | SBP | repurposed to support | costs, and improves | |

| Finance Scheme under | short-term liquidity | ability to fill EU | ||

| EXIM Bank) for textile | orders in a period of | |||

| and apparel firms selling | intensified | |||

| in EU. | competition. | |||

| 2. Tax Refund for | Federal Board | 0–9 | Minimal direct outlay. | Improves cash flows |

| Exporters: Streamline | of Revenue; | months | for exporters, | |

| export tax refunds (sales | Ministry of | enhancing price | ||

| tax, drawback schemes); | Finance | competitiveness | ||

| monitor clearance | against Indian | |||

| times. | suppliers. | |||

| 3. Targeted Energy Cost | Ministry of | 0–12 | Recent power tariff | Reduces unit |

| Relief for Export- | Energy; Power | months | cuts (PKR 4.04/unit | production costs |

| Oriented Firms: | Division; ECC | reduction) has fiscal | where energy | |

| Implement temporary | cost. | accounts for a large | ||

| sector-specific energy | share of costs, | |||

| tariff adjustments or | improve | |||

| rebates for textiles. | competitiveness in | |||

| EU markets. | ||||

| Policy Action | Lead Institution | Time frame | Fiscal Cost | Expected Impact |

| 4. Remove of Export | Ministry of | Immediate | Removal of 0.25 % | Improves cost |

| Development Surcharge | Finance; SBP | surcharge has limited | structure for | |

| & Simplify Incentives | fiscal impact. | exporters and | ||

| positive policy signal; | ||||

| complements | ||||

| broader | ||||

| competitiveness | ||||

| agenda. | ||||

| 5. Productivity and | Ministry of | 6–24 | Requires cost–benefit | Raises firm-level |

| Upgrading Scheme: | Industries & | months | analysis. | productivity, |

| Time-bound cost- | Production; | exporters can | ||

| sharing scheme for | TDAP | sustain market share | ||

| technology adoption, | with narrower tariff | |||

| compliance upgrades, | margins. | |||

| process improvements. | ||||

| 6. Trade Facilitation & | TDAP; Ministry | 3–12 | Requires modest | Improves export |

| Market Intelligence | of Commerce | months | budget. | market access and |

| Support: Targeted | diversification of | |||

| market research, buyer | product lines with | |||

| outreach, and export | comparative | |||

| readiness programmes. | advantages. |

Notes:

- https://www.brecorder.com/news/40308211

- https://tribune.com.pk/story/2590027/pm-unveils-major-relief-for-industry-export-sectors

- https://www.brecorder.com/news/40394148