Exchange Rate Policy Must Seek Undervaluation!

Abdul Jalil, Professor of Economics, Pakistan Institute of Development Economics, Islamabad.

| In Pakistan, the exchange rate policy has always tended towards overvaluation (see Box 1). This policy has led to five major currency crises, an attack on foreign exchange reserves, and an eventual IMF programme, over the last 30 years (Haque and Hina, 2020). The present knowledge brief reviews literature on the relationship between exchange rate policy stance and economic growth. Besides, an attempt is also made to estimate the misalignment of the exchange rate for Pakistan using an econometric model. The evidence provides overwhelming support for an exchange rate policy that seeks undervaluation to stimulate growth. In Pakistan, however, the State Bank of Pakistan (SBP) continues to adopt the policy of exchange rate overvaluation. |

| Box 1: Currency Misalignment Misaligned currency means exchange rate that is inconsistent with satisfactory macroeconomic fundamentals of a country. If the currency is misaligned, then it may be overvalued or undervalued. Overvaluation: If the currency of a country is overvalued, then it makes the imports attractive and exports hard to sell. Currency overvaluation leads to an unsustainable current account deficit. Undervaluation: On the other hand, if the currency of a country is undervalued, it results in current account surplus. Undervaluation of currency can stimulate the economy to a higher economic growth level. |

The Impact of Misalignment on Economic Growth around the World

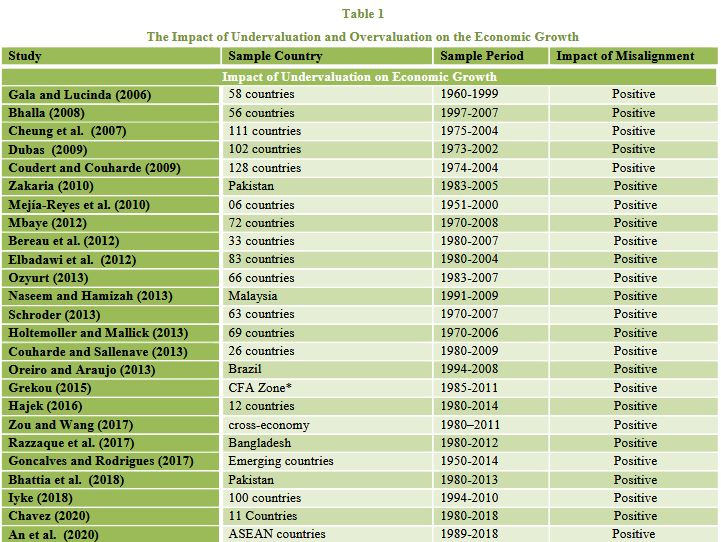

| As mentioned earlier, there is an extensive literature that tests the impact of exchange rate misalignment on economic growth. Three essential points can be inferred from the literature. · There are different concepts of real exchange rate misalignment (see Box 2). · Researchers use different sets of explanatory variables to calculate the equilibrium exchange rate. · The calculation of the equilibrium exchange rate is sensitive to econometric models and econometric techniques. Despite all the technical issues, there is almost a consensus that the real exchange rate undervaluation positively impacts economic growth. More specifically, Bhalla (2008) notes that each 1 percent sustained undervaluation may lead to 0.3 percent to 0.4 percent increase in economic growth. On the other hand, the overvaluation of the real exchange rate negatively impacts economic activities (see Table 1). |

| Box 2: Methodologies for Measuring the Misalignment of Exchange Rate The difference between the prevailing exchange rate and the ‘equilibrium’ exchange rate is called the misalignment of the exchange rate. The measurement of the equilibrium exchange rate is not a straightforward task. The researchers provide various measures depending on the objective, focus, the conceptual framework, empirical methodology, and assumptions (Isard, 2007). Therefore, the literature suggests several empirical methodologies to measure the equilibrium exchange rate. These may be model-independent or model-dependent. In a nutshell, there is not an ‘equilibrium’ exchange rate. All measures provide different numbers for the equilibrium exchange rate depending on the period, methodology, and underlying assumptions about the macroeconomic variables. |

The Channels through which (Mis)Alignment Effect Economic Growth

- The literature cites the example of East Asian countries’ outward-oriented policies when discussing the positive impact of the undervaluation of currency on economic growth. On the other hand, the overvalued currency hurt the Latin American and African countries’ economic growth following inward-oriented policies.

- Rodrik (2008) notes that market failures and bad institutions affect the tradable sector in developing countries. Therefore, currency undervaluation might work to correct market distortions and positively impact economic growth.

- The currency undervaluation may boost the industrial sector through incentives for capital accumulation, technological capabilities, and information spillover. The improved industrial sector will add to the economic growth of the country.

- Theoretically, Gala (2007) suggests that the real exchange rate’s undervaluation may increase profit margins. These profit margins will induce higher savings, investments, and ultimately increase economic growth.

- A stable and competitive (undervalued) real exchange rate may boost economic diversification in developing countries.

The Case of Pakistan

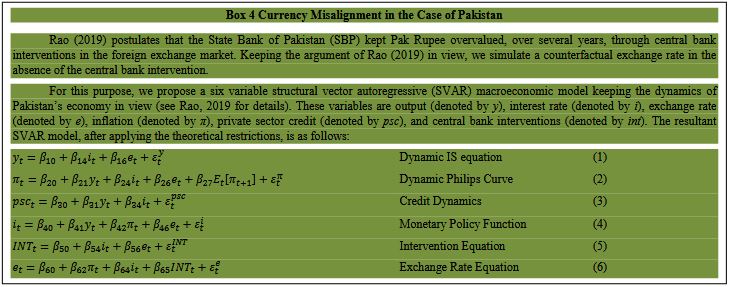

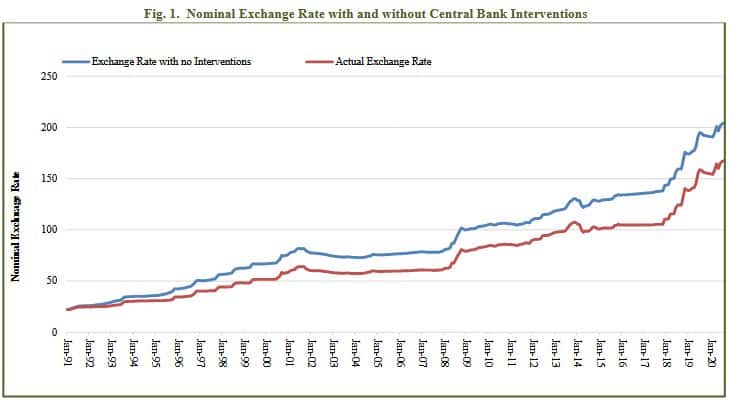

As mentioned earlier, the SBP continuously pursuing the policy of keeping the exchange rate parity overvalued by supporting the foreign exchange market through central bank interventions (see Box 3). Therefore, the prevailing nominal exchange rate in Pakistan does not reflect the equilibrium exchange rate. The difference between the prevailing and the equilibrium exchange rate is called the exchange rate misalignment. As mentioned earlier, there are several methods to calculate the misalignment of the exchange rate (see Box 2). However, we follow the IMF’s suggestions[1] and use an econometric model by taking several variables into account, keeping the dynamics of Pakistan’s economy in view. In this regard, we take Rao’s (2019) guidelines to construct a macro model for Pakistan’s case (Box 4). Since the SBP manages the exchange rate parity through interventions, we simulate the nominal exchange rate with and without foreign exchange interventions (see Figure 1).

_____________________________

[1] Almost all the IMF methodologies are based on econometric estimations.

| Box 3. Central Bank Interventions The central banks intervene in the foreign exchange market through buying and selling of the foreign/local currency to support the nominal exchange rate parity. The support could be to reach a specific desired level of exchange rate parity or to reduce the exchange rate volatility in the currency exchange market. Selling of Foreign Currency: When the local currency is under pressure in the foreign exchange market due to weak macroeconomic fundamentals, the market signals to depreciate the exchange rate. In this scenario, the central bank sells foreign currency and buys local currency to manage the pressure. The exchange rate will be overvalued. Resultantly, the central banks lose foreign exchange reserves. The reserve deficient countries, such as Pakistan, cannot afford this policy for a long time. Whenever the central bank stops the support due to the lack of foreign exchange reserves, the local currency depreciates rapidly to adjusts to its market value. Sometimes, rapid depreciation may lead to currency crises. Buying of Foreign Currency: On the other hand, the central bank buys the foreign currency when the market forces signal the appreciation of the local currency. The central bank builds the international reserves in this process. |

Figure 1 provides a historical evaluation of SBP’s intervention effectiveness in controlling the exchange rate parity.

Our analysis comes up with three main messages, namely:

- First, if the SBP does not intervene to support the foreign exchange market, the exchange rate would have been around 205 per USD at the end of August of 2020. The support of SBP kept the exchange rate overvalued for a long time.

- Second, following Rao’s (2019) methodology, our estimates show that the SBP has provided cumulative direct market support of USD 119 billion from January 1991 to August 2020. However, the support of USD 119 billion has yielded management of the exchange rate by only Rs. 36.

- Third, the overvalued exchange rate largely subsidised imported consumption and distorted the competitiveness of exportable items. This led to a higher trade deficit, balance of payment (BOP) crises, and ultimately the IMF bailout packages. This also suggests that if the SBP adopts a less protective exchange rate regime, we may avoid severe economic outcomes such as the depletion of foreign exchange reserves, BOP crises, and currency crises (Haque and Hina, 2020).

Conclusion

This note provides overwhelming evidence that currency undervaluation is beneficial for economic growth. A macro-econometric model shows that the SBP continually used our scarce foreign exchange reserves to keep the exchange rate arbitrarily overvalued throughout history. This is one important factor that has contributed to our repeated BOP crises and IMF programmes. We hope that this note will inform the exchange rate policy to keep an undervalued target exchange rate and not use reserves to fight overvaluation (see also Jalil, 2020).

References

Abida, Z. (2011). Real exchange rate misalignment and economic growth: An empirical study for the Maghreb countries. Zagreb International Review of Economics & Business, 14(2), 87–105.

Akram, V. & Rath, B. N. (2017). Exchange rate misalignment and economic growth in India. Journal of Financial Economic Policy, 9, 414–434.

An, P. T. H., Binh, N. T., & Cam, H. L. N. (2020). The impact of exchange rate on economic growth case studies of countries in the ASEAN region. Global Journal of Management and Business Research, 9, 965–970.

Baxa, J., & Paulus, M. (2020). Exchange rate misalignments, growth, and institutions (IES Working Paper No. 2020/27). Charles University Prague, Faculty of Social Sciences, Institute of Economic Studies.

Béreau, S., Villavicencio, A. L., & Mignon, V. (2012). Currency misalignments and growth: A new look using nonlinear panel data methods. Applied Economics, 44, 3503–3511.

Bhall, S. (2008) Economic development and the role of currency undervaluation. Cato Journal, 28, 313–340.

Bhatti, A. A., Ahmed, T., & Hussain, B. (2018). Growth effects of real exchange rate misalignment: Evidence from Pakistan. The Pakistan Journal of Social Issues, 9, 70–88.

Chavez, C. (2020). How is the dynamic impact of undervaluation on economic growth in Latin American countries? A panel VAR analysis [forthcoming] DOI:10.21203/rs.3.rs-25367/v1

Cheung, Y. W., Chinn, M. D., & Fujii, E. (2007). The overvaluation of renminbi undervaluation. Journal of International Money and Finance, 26(5), 762–785.

Chen, S. S. (2017). Exchange rate undervaluation and R&D activity. Journal of International Money and Finance, 72, 148–160.

Coudert, V., & Couharde, C. (2009). Currency misalignments and exchange rate regimes in emerging and developing countries. Review of International Economics, 17(1), 121–136.

Couharde, C., & Sallenave, A. (2013). How do currency misalignments’ threshold affect economic growth? Journal of Macroeconomics, 36, 106–120.

Dubas, J. M. (2009). The importance of the exchange rate regime in limiting misalignment. World Development, 37(10), 1612–1622.

Debowicz, D., & Saeed, W. (2014). Exchange rate misalignment and economic development: The case of Pakistan. Global Development Institute, GDI, The University of Manchester. (Working Paper Series 21014).

Elbadawi, I. A., Kaltani, L., & Soto, R. (2012). Aid, real exchange rate misalignment, and economic growth in Sub-Saharan Africa. World Development, 40(4), 681–700.

Gala, P., & Lucinda, C. R. (2006). Exchange rate misalignment and growth: Old and new econometric evidence. Revista Economia, 7(4), 165–187.

Goncalves, C., & Rodrigues, M. (2017). Exchange rate misalignment and growth: A myth? International Monetary Fund. (Working Paper No. 17/283).

Grekou, C. (2015). Revisiting the nexus between currency misalignments and growth in the CFA Zone. Economic Modelling, 45, 142–154.

Haque, N. and Hina, H. (2020). Pakistan’s five currency crises. Pakistan Institute of Development Economics (PIDE), Islamabad. (Knowledge Brief 7).

Hajek, J. (2016). Real exchange rate misalignment in the Euro area: Is the current development helpful? (IES Working Paper No. 11/2016).

Hall, S. G., Kenjegaliev, A., Swamy, P. A. V. B., and Tavlas, G. S. (2013). Measuring currency pressures: The cases of the Japanese yen, the Chinese yuan, and the UK pound. Journal of the Japanese and International Economies, 29, 1–20.

Holtemöller, O., & Mallick, S. (2013). Exchange rate regime, real misalignment and currency crises. Economic Modelling, 34, 5–14.

Isard, Peter (2007), Equilibrium exchange rate: Assessment methodologies. (IMF Working Paper, WP/07/296).

Iyke, B. N. (2018). The real effect of currency misalignment on productivity growth: Evidence from middle-income economies. Empirical Economics, 55(4), 1637–1659.

Jalil, A. (2020) What do we know of exchange rate pass-through? Pakistan Institute of Development Economics (PIDE), Islamabad. (Knowledge Brief 1).

Jehan, Z., & Irshad, I. (2020). Exchange rate misalignment and economic growth in Pakistan: The role of financial development. The Pakistan Development Review, 59(1), 81–99.

Karahan, Ö. (2020). Influence of exchange rate on the economic growth in the Turkish economy. Financial Assets and Investing, 11(1), 21–34.

Kemme, D. M., & Roy, S. (2006). Real exchange rate misalignment: Prelude to crisis? Economic Systems, 30(3), 207–230.

Mbaye, S. (2012). Real exchange rate undervaluation and growth: Is there a total factor productivity growth channel? CERDI. (Working Papers 201211).

Mejía-Reyes, P., Osborn, D. R., & Sensier, M. (2010). Modelling real exchange rate effects on output performance in Latin America. Applied Economics, 42(19), 2491–2503.

Morvillier, F. (2020). Do currency undervaluations affect the impact of inflation on growth? Economic Modelling, 84, 275–292.

Naseem, N. A. M., & Hamizah, M. S. (2013). Exchange rate misalignment and economic growth: Recent evidence in Malaysia. Pertanika Social Sciences & Humanities, 21, 47–66.

Nouira, R., and Sekkat, K. (2012). Desperately seeking the positive impact of undervaluation on growth. Journal of Macroeconomics, 34(2), 537–552.

Oreiro, L. J., & Araujo, E. (2013). Exchange rate misalignment, capital accumulation and income distribution: Theory and evidence from the case of Brazil. Panoeconomicus, 60(3), 381–396.

Özyurt, S. (2013). Currency undervaluation and economic rebalancing towards services: Is China an exception? China & World Economy, 21(1), 47–63.

Rafindadi, A. A. (2015). Are the contentious issues of exchange rate misalignment in Nigeria a prelude to the country’s currency crisis? International Journal of Economics and Financial Issues, 5(3), 716–731.

Rao, N. H. (2019) Effectiveness of monetary policy in controlling exchange market pressures: Case of Pakistan. Department of Economics and Finance, Pakistan Institute of Development Economics (PIDE). (MPhil Thesis).

Razin, O., & Collins, S. M. (1997). Real exchange rate misalignments and growth. National Bureau of Economic Research. ((Working No. 6174).

Razzaque, M. A., Bidisha, S. H., & Khondker, B. H. (2017). Exchange rate and economic growth: An empirical assessment for Bangladesh. Journal of South Asian Development, 12(1), 42–64.

Rodrik, D. (2008). The real exchange rate and economic growth. Brookings Papers on Economic Activity 2008 (2), 365–412.

Ribeiro, R. S., McCombie, J. S., & Lima, G. T. (2020). Does real exchange rate undervaluation really promote economic growth? Structural Change and Economic Dynamics, 52, 408–417.

Schröder, M. (2013). Should developing countries undervalue their currencies? Journal of Development Economics, 105, 140–151.

Wong, H. T. (2013). Real exchange rate misalignment and economic growth in Malaysia. Journal of Economic Studies, 40, 298–313.

Zakaria, M. (2010). Exchange rate misalignment and economic growth: Evidence from Pakistan’s recent float. The Singapore Economic Review, 55(03), 471–489.

Zou, J. & Wang, Y. (2017). Undervaluation, financial development, and economic growth. Asian Development Review, 34(1), 116–143.