Key Takeaways

- Pakistan is structurally exposed to a Gulf oil shock because imported energy remains deeply embedded in the external account, and Gulf-related oil and gas dependence makes the Strait of Hormuz a direct macroeconomic vulnerability.

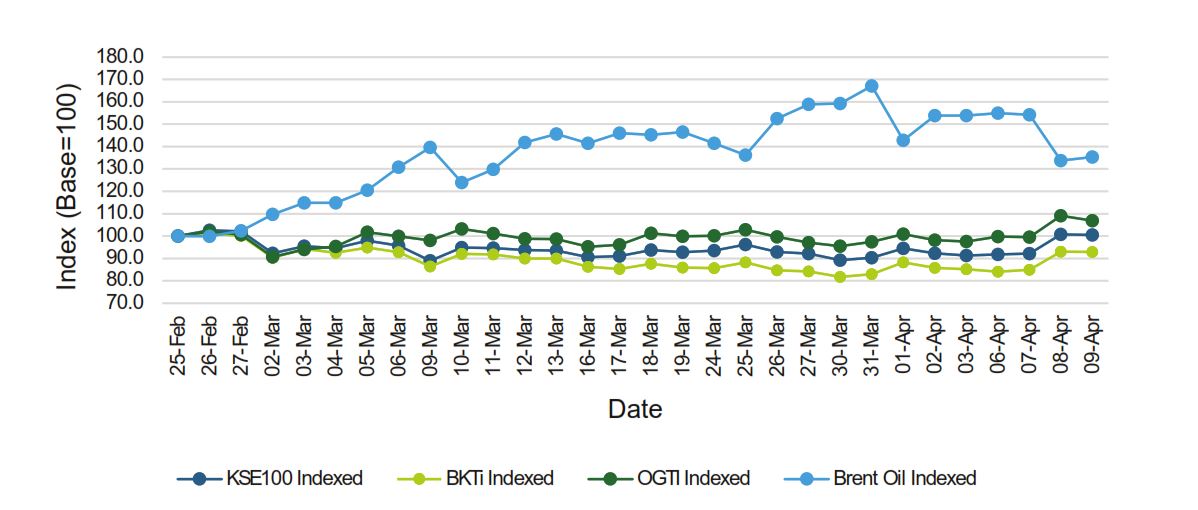

- The market has already priced this vulnerability, but not through a one-directional decline. Over 25 February to 09 April 2026, Brent rose by 35.4 percent, while the Pakistan Stock Exchange (PSX) indices experienced sharp interim corrections, high daily volatility, and then uneven recovery. Over this period, the KSE100 index closed slightly positive at 0.5 percent; KMI30 gained 5.3 percent; PSXDIV20 edged up 0.2 percent; and OGTI rose 6.8 percent. KSE30 ended marginally lower at 0.3 percent, and BKTi remained the weakest segment at negative 7.1 percent. This pattern suggests that the war was priced as a macro-financial shock, but with differentiated sectoral adjustment rather than uniform market collapse.

- The risk is not limited to oil prices alone. The PIDE working paper by Satti and Nawaz (2026) shows that even a mild Hormuz shock can raise the monthly petroleum import bill by about USD 142.3 million and shift the current account from a surplus to a deficit, while the stress and severe cases add 3.41 and 5.34 percentage points to inflation over six months, capturing non-linearities in prices of crude oil and petroleum products.

Executive summary

Pakistan is not watching the Iran-Israel war from a distance. It is absorbing the shock through oil prices, inflation expectations, and equity repricing. As an oil-importing economy exposed to disruption in the Strait of Hormuz, Pakistan faces higher freight and fuel costs, pressure on the current account, and a rise in the discount rate applied to future cash flows. The PSX has already internalized this risk: Brent[1] rose sharply over the sample period, while domestic indices experienced a sharp correction, high volatility, and only uneven recovery. The broader policy lesson is clear. Pakistan needs stronger energy contingency planning, better macro-financial communication, and a durable reduction in its dependence on imported oil.

1. Why this conflict matters for Pakistan

The recent Iran-Israel conflict has served as a live stress test of how quickly geopolitical tension in the Gulf can transmit into oil prices, investor sentiment, and equity valuation in oil-importing economies. For Pakistan, the episode is significant not only because of short-term market volatility, but because it reveals a deeper structural vulnerability linked to imported energy, external financing pressure, and dependence on the Strait of Hormuz. For instance, stock prices of the gas and oil sector in PSX, after a short dip, have been adjusted to their pre-war level, whereas the other sectors’ performance is highly connected with the conflict.

The economic significance of the conflict lies in Pakistan’s structural exposure to Gulf energy routes. The Strait of Hormuz carries a large share of globally traded petroleum, while Pakistan’s import dependence on Gulf suppliers means that any disruption quickly feeds into freight costs, inflation, reserve pressure, and investor sentiment. The conflict, therefore, matters not only as a regional security episode but as a direct macro-financial shock for an oil-importing economy.

Pakistan relies on oil imports primarily from Saudi Arabia, UAE, Kuwait, and Qatar. In FY 2025-26, these imports cost more than USD 15 billion (around 25% of total imports) and have serious implications for inflation that are transmitted to the economy. While LNG supply disruptions may create adverse implications for the economy, they also underscore the importance of encouraging investment in the exploration and development of domestic oil and gas resources.

The conflict should therefore be understood not only as a matter of foreign policy or regional security, but also as a macro-financial shock for Pakistan. A country that depends heavily on imported energy does not need direct military involvement to experience the consequences of conflict in the Gulf. Price movements, expectations, freight costs, reserve pressures, and capital-market adjustments transmit the shock well before official macroeconomic indicators are able to capture its full extent.

2. How the shock travels to Pakistan’s economy and market

Stock prices respond before the full economic damage becomes visible because they reflect the present value of future expected cash flows. Once conflict arises, the probability of higher oil prices, imported inflation, exchange-rate pressure, and tighter macro-financial conditions, investors revise valuations immediately. In this sense, the PSX operates as an early warning mechanism rather than a delayed reflection of published macroeconomic data.

The transmission runs through four linked channels: oil supply and shipping disruption, imported inflation, higher operating costs for listed firms, and financial repricing. Disruption in the Strait of Hormuz raises freight, insurance, rerouting, and fuel costs. These pressures worsen the external balance, revive inflationary concerns, and compress margins across energy-dependent sectors. Because oil is embedded in transport, logistics, packaging, fertilizer, manufacturing, and distribution, even firms that do not import petroleum directly face second-round cost pressures. As expectations of inflation, weaker margins, and tighter policy begin to build, investors demand a higher risk premium. The result is a market adjustment that reaches equities before the full shock becomes visible in growth, trade, or corporate accounts.

3. What the recent market movement is already telling us The recent market evidence shows that the PSX internalized the war shock quickly. Brent recorded the strongest gain over the sample period, while domestic indices moved through sharp correction, elevated volatility, and only uneven recovery by early April. BKTi remained the weakest domestic segment, indicating persistent macro-financial stress, whereas OGTI outperformed the broader market but did not behave like a full hedge. The overall pattern suggests that the war was priced less as a narrow commodity opportunity and more as a systemic risk event for an oil-importing economy.

Figure 1: Indexed movement of Brent Oil and selected PSX indices

Note: Author’s calculations| Brent Oil, KSE100, BKTi, and OGTi are indexed to 10In0 on 25 February 2026.

Source: https://markets.brecorder.com/indices

Table 1. Cumulative return of PSX indices and Brent Oil during the sample period

| Series | Start value

25 February 2026 |

End value

09 April 2026 |

Cumulative return | Performance rank |

| Brent Oil | 70.85 | 95.92 | 35.4% | 1 |

| OGTI | 32109.94 | 34306.12 | 6.8% | 2 |

| KMI30 | 229014.43 | 241192.41 | 5.3% | 3 |

| KSE100 | 164626.29 | 165517.52 | 0.5% | 4 |

| PSXDIV20 | 75339.17 | 75520.69 | 0.2% | 5 |

| KSE30 | 50342.54 | 50169.05 | -0.3% | 6 |

| BKTi | 49028.54 | 45529.23 | -7.1% | 7 |

Note: Author’s calculations| Brent Oil, OGTi, KMI30, KSE100, , PSXDIV20, and BKTi

Source: https://markets.brecorder.com/indices

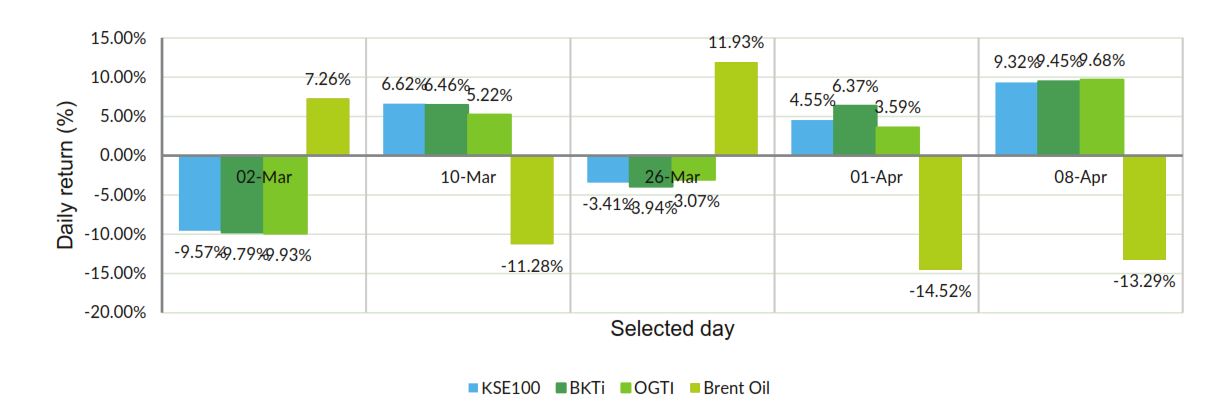

The sharp day-to-day swings reinforce the central argument of this viewpoint. Pakistan’s market response on selected war-related trading days did not follow a simple oil-trade pattern. Figure 2 adopts a hybrid event-selection approach: 02 March 2026 is included as the first domestic market session after the outbreak of war, while the remaining dates are drawn from the largest absolute daily Brent movements in the sample. The figure shows that Brent could rise sharply even as the broader market weakened, while OGTI offered only partial insulation. The war was therefore priced less as a commodity gain and more as a macro-financial risk shock with uneven sectoral transmission.

Figure 2. Daily return response on selected war-event and oil-shock days

Note. Author’s calculations, The bars show one-day percentage returns for Brent Oil, KSE100, BKTi, and OGTi on 02,10,26 March and 01,08 April 2026.

Even if active hostilities recede, the market evidence from this episode remains instructive. The ceasefire may reduce immediate escalation risk, but the broader lesson is that Pakistan’s exposure does not disappear with a pause in fighting. So long as oil flows, freight costs, and investor expectations remain sensitive to developments in the Gulf, domestic markets will continue to price energy insecurity as a macro-financial risk. Shipping through the Strait of Hormuz remains disrupted, and oil markets continue to carry a geopolitical risk premium. In this setting, Figure 2 should be read not only as evidence of wartime volatility, but also as evidence of continued investor caution under a fragile and incomplete de-escalation.

From a policy perspective, the market is now pricing not only conflict risk, but also negotiation credibility. If the ceasefire matures into a successful negotiating process, Brent is likely to soften from emergency levels, shipping constraints may ease, and the PSX could move from defensive stabilization toward broader recovery, particularly in banking and liquid large-cap stocks. If negotiations fail or the truce breaks down, the opposite pattern is more likely: Brent would retain or rebuild its geopolitical premium, macro-sensitive indices would remain under pressure, and BKTi would again be the clearest barometer of unresolved domestic stress.

4. Information transmission channels to the indices

The indices in the sample are not interchangeable. Each one captures a different layer of the war-oil transmission mechanism, and together they show how an external energy shock travels through Pakistan’s capital market. Official PSX methodology also makes clear that these indices represent different slices of the market: KSE100 is the broad benchmark, KSE30 captures the most liquid large-cap names, Karachi Meezan Index (KMI30) tracks liquid Shariah-compliant companies, PSXDIV20 follows the top dividend payers, BKTi represents the banking sector, and OGTi tracks the tradable oil and gas sector[2],[3].

KSE100 is the broadest market signal in the sample and therefore the clearest indicator of how Pakistan repriced the war shock at the aggregate level. Its end-period recovery should not be mistaken for stability. The index corrected sharply during the conflict phase and recovered only after the initial stress began to ease, which suggests that investors first priced the war as a broad macro-financial shock and only later adjusted to a more fragile baseline.

BKTi provides the sharpest signal of unresolved domestic stress. Banking remained the weakest segment because oil-driven inflation, tighter policy expectations, weaker credit conditions, and borrower stress all converged in the financial sector. Its incomplete recovery suggests that the market continued to treat banking as the main carrier of macro-financial vulnerability.

OGTI was the only clear sectoral cushion, but even here the story was not one of clean protection. Higher oil prices improved earnings expectations for upstream firms, yet the index remained volatile and significantly underperformed Brent itself. OGTI therefore signals partial insulation through the oil-price channel, but not full decoupling from Pakistan’s wider country-risk environment.

[1] Brent returns are used for comparison due to data availability constraints of Dubai crude; Pakistan is generally proxied by Dubai crude.

[2] https://www.psx.com.pk/psx/product-and-services/indices

[3] https://www.psx.com.pk/psx/resources-and-tools/shariah-compliant-investment