Higher Taxes Reduce Economic Growth: Overwhelming International Evidence

Sarah Nizamani, Research Associate, PIDE

“Taxation may be so high as to defeat its object, and that, given time to gather the fruits, a reduction of taxation will run a better chance than an increase of balancing the budget”[1]

John Maynard Keynes

For decades, the topic of economic growth and its prosperity has been the heart of debate all over the world. Without any doubt, technology, investment (in both human and physical capital) and new techniques of production are the growth fundamentals. Due to its power to affect investment and profitability, taxation plays a fundamental role in choices made and ultimately, the pace of development and growth. In nations of the world, the rate of taxation has risen consistently through the course of the last century. Such huge increments in tax collection bring up significant issues about the impact they have upon the growth of the economy.

Individuals including researchers, economists, and some politicians, at different places and times, find it difficult to come to a consensus regarding two fundamental tax issues.

First, the effects of taxation on economic growth and secondly, the rate of taxes (high or low) to maximise the tax revenue. Some argue that governments collecting high tax rates could collect more tax revenues if they bring the tax rate down. The rationale behind lower tax rates argument is that lowered rates could change the economic incentives and lead to higher economic activity hence generating more revenue as compared to high tax rates. This is a testable hypothesis that could be proved on the empirical and analytical ground, however, that is seldom what happens. This knowledge brief plans to look at the literature for understanding the relation between growth and taxation and the impact of tax rates on the economy, but before we do that, we will revisit some basics of economics and its lost concepts.

____________________________

[1]John Maynard Keynes, “The Means to Prosperity,” The Means to Prosperity, by J. M. Keynes, et al., (Buffalo: Economica Books, 1959), p. 11.

The Lost Concepts of Economics

The truth often is not difficult to comprehend. As Thomas Sowell says, “The facts are unmistakably plain, for those who bother to check the facts”[2]. Two basic economic concepts are frequently lost in the shuffle. The first concept is the concept of cost. The more something costs, the less of it you get. Pricier cars sell less than low-cost cars to a great extent on account of cost. A similar idea applies to employment. The more jobs cost, the less of them we get as the general public (Ample evidence is available on the negative effect of minimum wage laws on employment). Examples would be organisations declining to hire because of those higher costs.

Important but not understood largely, is that the same concept applies to income as well. The higher the income costs, (for example, the higher the income and corporate tax rates) the less income you see. History is full of examples of individuals who have done numerous things to keep away from taxes including move, deal, defer and hide investments and face less risk, as they choose not to attempt to make more cash. To put it plainly, as Chief Justice John Marshall said, “The Power to Tax is the Power to Destroy”

The second concept is that if the administration takes your money, you do not have it. By the day’s end, what makes a difference is the amount the money the government removes from the general economy and when. If the government’s chunk is excessively huge in forms of taxes, duties, and regulatory fees, the investment and purchasing power decreases for people and organisations. Consequently, the economy decreases and becomes smaller. The government exacerbates these issues when it burdens the economy with high taxes intending to collect greater revenues in a damaged economy. The administration seems to forget the fact that individuals who make countless decisions each day for their benefit and ultimately benefiting society drive the economy. Micromanaging and regularising these decisions can bring more harm than benefit. Keynes needed others to comprehend that taxation policy ought to be guided to the right level to not demoralise income but rather support in boosting incomes and eventually revenues.

“At a beginning of a dynasty, taxation yields a large revenue on small assessments. At the end of the dynasty, taxation yields a small revenue from a large assessment.”

Ibn-Khuldun

_____________________________

[2]Thomas Sowell “Trickle Down” Theory and “Tax Cuts for the Rich”, by T. Sowell (Hoover Institution Press, Stanford University, 2012), p.3.

A Review of the Recent Literature

This section explores the literature on taxation and growth conducted based on both national and international studies.

Evidence from Cross-sectional Studies

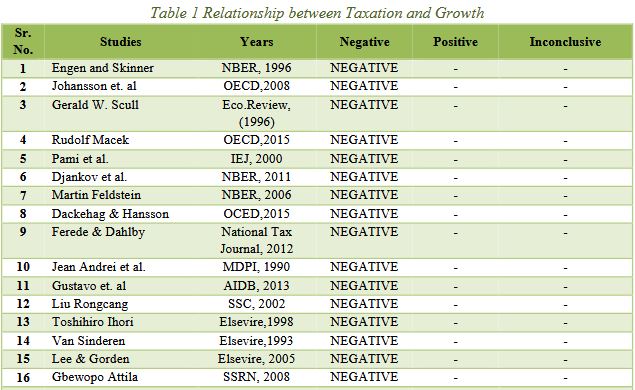

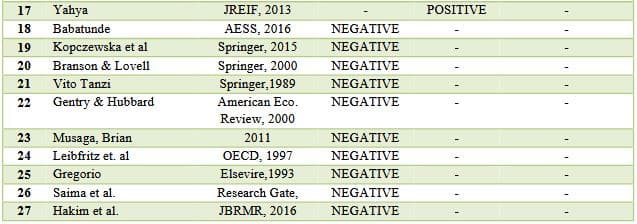

Analysing the cross-sectional and time-series data for 1970-1997, Lea and Gordon (2005) visualise the effect of taxation on growth and concluded that corporate tax was negatively related to growth for all seventeen nations. In case the tax was reduced by ten per cent, it could increase the growth rate by 1.1 percent. A study by Pami et al. (2000) identifies the negative effect of income tax on GDP where exports taxes were also identified as negative and significant. Dackehag and Hansson (2012) used fixed-effect regression for 25 OECD countries from 1970 to 2010, finding that both income and corporate taxes were negatively affecting economic growth in the OECD region. Abdioglu et al. (2016) examines the relationship between corporate income taxes and foreign direct investment level in OECD countries and found that FDI increases significantly followed by tax rate reductions in the region. The study concludes that countries that reduced their tax rates attracted higher levels of FDIs. Djankov et al. (2011) in an investigation of 85 countries discovered a large negative effect of corporate income tax on aggregate investment, FDI and entrepreneurship. The finding quotes “For example, a 10 percent increase in the effective corporate tax rate reduces aggregate investment to GDP ratio by 2 percentage points”.

“There’s only one way to kill capitalism—by taxes, taxes, and more taxes.”

—Karl Marx

Evidence from Panel Studies

An investigation of taxation in Canada by Ergete and Bev (2012) signifies that a higher income tax is related to lower private investment and slower economic development. They suggest that to increase federal tax revenue, corporate and personal income tax rates have to decrease. Jules (2008), using regression analysis for states for data from 1964 to 2004, confirms a similar result of a significant negative impact of marginal tax rates on economic growth. Feldstein (2006) confirms the distortion of factor prices and efficiency loss in resource allocation caused by taxes. Taxes affect total factor productivity induced by efficiency loss. Other ways taxes affect the total factor productivity is its negative effect on entrepreneurship. Entrepreneurship leads to new ideas for higher productivity. Higher taxes discourage entrepreneurial activities, which is indicated in several studies including Gentry and Hubbard (2000) and Cullen and Gordon (2007). Jaimovich and Rebelo (2015) find the effect of taxation on growth non-linear and that low or moderate tax rate have a small impact on the long-run growth rate, however, as the tax rate rises, the negative impact of taxation on growth increases dramatically.

Evidence from Pakistan

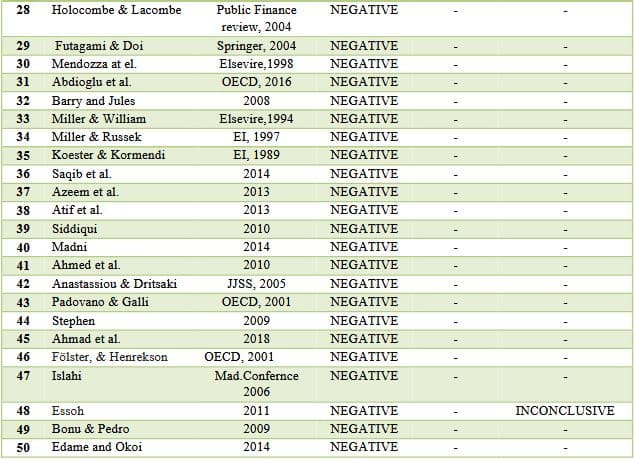

Saqib et al. (2014), Azeem et al. (2013), Atif et al. (2013) and Siddiqui (2010) confirm the negative effect of taxation on real per capita GDP. Madni (2014) discovers that both direct and indirect taxes were causing inflation to increase in the country. Ahmed et al. (2010) run a micro-simulation analysis for tax reform in the country and conclude that almost simulations of increasing the tax rate in the country result in a decrease in investment levels, reduced consumption, and an increase in poverty. Ahmad et al. (2018) analyses the impact on indirect taxation in the country for time series data (1974-2010) and confirms the negative effect of indirect taxation on growth. The study declares that one percent increase in indirect taxes reduces growth by 1.68 percent.

| Chapter 57 of the Tao Te Ching, written in approximately the fifth century BC, reads: Run the country by doing what’s expected. Win the war by doing the unexpected. Control the world by doing nothing. How do I know this? By this. The more restrictions and prohibitions in the world the poorer the people get. The more experts a country has the more of a mess it’s in. The more ingenious the skillful are the more monstrous their inventions. The louder the call for law and order the more the thieves and con men multiply. So a wise leader might say: I practice inaction, and the people look after themselves. I love to be quiet, and the people themselves find justice. I don’t do business, and the people prosper on their own. I don’t have wants, and the people themselves are uncut wood [naturally virtuous] |

Pakistan and Taxes

Time after time, the people of Pakistan are often called “Tax Cheats” by their government and are embarrassed by donors at various forums. The depressing stats that only one per cent of the population pays income tax is mentioned whenever taxation revenue of this country is discussed but is it true? Do we only pay such minimal taxes? The country has no tax-free goods or services. The Federal Board of Revenue (FBR) in its pre-COVID-19 time was celebrating higher tax revenue collection but all without generating new income. Instead, the taxes on utilities like energy prices went up by 20-30 percent, further tightening the grip on the income of the country, which was already struggling with double-digit inflation. The list of indirect taxes in the country is long. According to a recent article,[3] the country’s 96 million mobile phone users and 82 million internet users are paying advance, adjustable income taxes of 12.5 percent, all without the data that how many of them are eligible for taxable income. The solution everyone seems to suggest is “Progressive taxation”, but one enlightening example of progressive taxation in South Africa, where the progressive taxation rate is the highest in the world and is still the country with highest income inequality.[4] The question remains, is it solely the problem of tax evasion (which is true for Pakistan to some extent like rest of the world) or the issue of incompetent and complicated tax policy, public trust issues, frequently changing SROs, poor taxation education and lack of research and development in the tax department?

The Table 1 concludes the results of taxation and growth from studies mentioned in the literature review and more.

______________________________

______________________________

[3]Dr. Ikramul Haq- Huzaima Bukhari, “Finance Act 2020: Lack of initiatives and innovations”, Business Recorder.

[4]Max Ehrenfreund, “The country with the world’s most progressive taxes has the world’s highest income inequality”, Washington Post.

Taxes for Growth and Citizenship?

Frequently Pakistan is advised from donors to increase taxation for two basic reasons.

(1) To allow for more resource collection for the government to finance development.

(2) The citizenship and ownership in the country would increase if we adopt a western welfare model with social security nets.

While on the face of it these objectives are laudable, however, these arguments miss some fundamental points.

- First, Pakistan does not have a competent state that will use the increased revenues wisely. Some, including Haque (2017 and 2020), argue that the state is wasteful and incompetent. The state keeps wasting resources on poorly thought projects, building official housing and other low return or negative return projects (Haque et al. 2020).

- Second, high taxation is required to return the debt accumulated by the government. Instead of building checks on the government’s capacity to acquire debt and sign poorly planned contracts such as Reko Diq and Karke cases, the people of Pakistan are told these mistakes have to be paid by more taxes.

- Third, Pakistan is asked to copy the western social safety nets and welfare state while it stands at the stage of development without growth. This “isomorphic mimicry” merely stretches our already poor administration capacity to reduce growth and require more and more taxes – a vicious cycle. Rather than following the Haque proposition and reforming the state for efficiency, we are told to finance the inefficient state (Haque, 2017 and 2020). Our top priority in a series of IMF programs has been to increase taxation.

This survey shows that international and national evidence points out that taxation and growth are negatively correlated. It is time Pakistan took this seriously and changed the adjustment and growth model. If Pakistan thinks it through and can develop a good policy, the country can negotiate better with its international partners. Our growth is our responsibility and we should not follow anyone else’s model.

References

Abd Hakim, T., Karia, A. A., & Bujang, I. (2016). Does goods and services tax stimulate economic growth? International evidence. Journal of Business and Retail Management Research, 10(3).

Abdioğlu, N., Biniş, M., & Arslan, M. (2016). The effect of corporate tax rate on foreign direct investment: A panel study for OECD countries.

Ahmad, S., Sial, H. M., & Ahmad, N. (2018). Indirect taxes and economic growth: An empirical analysis of Pakistan. Pakistan Journal of Applied Economics, 28(1), 65-81.

Ahmed, S., Ahmed, V., & Abbas, A. (2010). Taxation reforms: A CGE-microsimulation analysis for Pakistan.

Anastassiou, T., & Dritsaki, C. (2005). Tax revenues and economic growth: An empirical investigation for Greece using causality analysis. Journal of Social Sciences, 1(2), 99-104.

Atif, M., Shahab, S., & Mahmood, M. T. (2012). The nexus between economic growth, investment and taxes: Empirical evidence from Pakistan. Academic Research International, 3(2), 530.

Attila, J. (2008). Corruption, taxation and economic growth: Theory and evidence.

Azeem, M. M., Saqi, M., Mushtaq, K., & Samie, A. (2013). An empirical analysis of tax rate and economic growth linkages of Pakistan. Pakistan Journal of Life and Social Sciences, 11(1), 14-18.

Bonu, N. S., & Motau, P. (2009). The impact of income tax rates (ITR) on the economic development of Botswana.

Branson, J., & Lovell, C. K. (2000). Taxation and economic growth in New Zealand. In Taxation and the Limits of Government (pp. 37-88). Springer, Boston, MA.

Dackehag, M., & Hansson, Å. (2015). Taxation of dividend income and economic growth: The case of Europe (No. 1081). (IFN Working Paper).

Dahlby, E. F. B., & Ferede, E. (2012). The impact of tax cuts on economic growth: Evidence from the Canadian provinces. National Tax Journal, 65(3), 563-594.

De Gregorio, J. (1993). Inflation, taxation, and long-run growth. Journal of Monetary Economics, 31(3), 271-298.

Djankov, Simeon, Tim Ganser, Caralee McLiesh, Rita Ramalho, and Andrei Shleifer. The effect of corporate taxes on investment and entrepreneurship. American Economic Journal: Macroeconomics 2, No. 3 (2010): 31-64.

Edame, G. E., & Okoi, W. W. (2014). The impact of taxation on investment and economic development in Nigeria. Academic Journal of Interdisciplinary Studies, 3(4), 209-209.

Engen, E. M., & Skinner, J. (1996). Taxation and economic growth (No. w5826). National Bureau of Economic Research.

Essoh, F. (2011). Effects of corporate taxes on economic growth: The case of Sweden. Jonkoping International Business School, Jönköping University.

Feldstein, M. (2006). The effect of taxes on efficiency and growth (No. w12201). National Bureau of Economic Research.

Fölster, S., & Henrekson, M. (2001). Growth effects of government expenditure and taxation in rich countries. European Economic Review, 45(8), 1501-1520.

Futagami, K., & Doi, J. (2004). Commodity taxation and economic growth. The Japanese Economic Review, 55(1), 46-55.

Gentry, W. M., & Hubbard, R. G. (2000). Tax policy and entrepreneurial entry. American Economic Review, 90(2), 283-287.

Gustavo, C., Jorge, M., & Violeta, V. (2013). Taxation and economic growth in Latin America. Inter-American Development Bank http: http://www20. iadb. org/intal/catalogo/PE/2013/12729. pdf (accessed: 11/04/2018).

Hamilton, S. F. (2009). Excise taxes with multiproduct transactions. American Economic Review, 99(1), 458-71.

Haque, N. (2020). Macroeconomic Research and Policy Making: Processes and Agenda [Ebook]. Pakistan Institute of Development Economics. Retrieved 26 July 2020.

Haque, N. (2017). Looking Back: How Pakistan Became an Asian Tiger by 2050. Kitab.

Haque, N., Mukhtar, H., Ishtiaq, N., & Gray, J. (2020). Doing Development Better. Pakistan Institute of Development Economics. Retrieved 26 July 2020, from.

Holcombe, R. G., & Lacombe, D. J. (2004). The effect of state income taxation on per capita income growth. Public Finance Review, 32(3), 292-312.

Ihori, T. (2001). Wealth taxation and economic growth. Journal of Public Economics, 79(1), 129-148.

Islahi, A. A. (2006, November). Ibn Khaldun’s theory of taxation and its relevance today. In Conference on Ibn Khaldun, Madrid, during (pp. 3-5).

Johansson, Å., Heady, C., Arnold, J., Brys, B., & Vartia, L. (2008). Taxation and economic growth.

Keho, Y. (2013). The structure of taxes and economic growth in Cote d’ivoire: An econometric investigation. Journal of Research in Economics and International Finance, 2(3), 39-48.

Koester, R. B., & Kormendi, R. C. (1989). Taxation, aggregate activity and economic growth: Cross‐country evidence on some supply‐side hypotheses. Economic Inquiry, 27(3), 367-386.

Kopczewska, K., Kudła, J., & Walczyk, K. (2017). Strategy of spatial panel estimation: Spatial spillovers between taxation and economic growth. Applied Spatial Analysis and Policy, 10(1), 77-102.

Lee, Y., & Gordon, R. H. (2005). Tax structure and economic growth. Journal of Public Economics, 89(5-6), 1027-1043.

Leibfritz, W., Thornton, J., & Bibbee, A. (1997). Taxation and economic performance.

Liu, R., & Ma, S. (2002). On taxation and economic growth: The effects of taxation imposed on labour, capital and consumption. Social Science in China, 1, 67-76.

Macek, R. (2015). The impact of taxation on economic growth: Case study of OECD countries. Review of Economic Perspectives, 14(4), 309-328.

Madni, G. R. (2014). Taxation, fiscal deficit and inflation in Pakistan. The Romanian Economic Journal, 17(53), 41-60.

Mendoza, E. G., Milesi-Ferretti, G. M., & Asea, P. (1997). On the ineffectiveness of tax policy in altering long-run growth: Harberger’s superneutrality conjecture. Journal of Public Economics, 66(1), 99-126.

Miller, S. M., & Russek, F. S. (1997). Fiscal structures and economic growth: International evidence. Economic Inquiry, 35(3), 603-613.

Mullen, J. K., & Williams, M. (1994). Marginal tax rates and state economic growth. Regional Science and Urban Economics, 24(6), 687-705.

Musaga, B. (2007). Effects of taxation on economic growth: (Uganda’s Experience: 1987-2005) (Doctoral dissertation, Makerere University).

Onakoya, A. B., & Afintinni, O. I. (2016). Taxation and economic growth in Nigeria. Asian Journal of Economic Modelling, 4(4), 199-210.

Padovano, F., & Galli, E. (2001). Tax rates and economic growth in the OECD countries. Economic Inquiry, 39(1), 44-57.

Pami, D., Aneesa Ismail, R., & Dominick, S. (2000). The impact of financial and fiscal variables on economic growth: The case of India and Korea. International Economic Journal, 14(2), 133-150.

Poulson, B. W., & Kaplan, J. G. (2008). State income taxes and economic growth. Cato J., 28, 53.

Saqib, S., Ali, T., Riaz, M. F., Anwar, S., & Aslam, A. (2014). Taxation effects on economic activity in Pakistan. Journal of Finance and Economics, 2(6), 215-219.

Scully, G. W. (1996). Taxation and economic growth in New Zealand. Pacific Economic Review, 1(2), 169-177.

Siddiqui, D. M. (2010). Tax revenue and economic growth: An empirical analysis for Pakistan. World Applied Sciences Journal, 10(11), 1283-1289.

Tanzi, V. (1989). The impact of macroeconomic policies on the level of taxation and the fiscal balance in developing countries. Staff Papers, 36(3), 633-656.

Van Sinderen, J. (1993). Taxation and economic growth: Some calculations with a macroeconomic semi-equilibrium model for the Dutch economy (MESEM). Economic Modelling, 10(3), 285-300.