In today’s globalized economy, countries are in constant competition to attract foreign investment, stimulate economic growth and integrate globally. To address this, after WW-II developed countries came together and created an international economic agreement designed by developed countries which is built upon two type of agreements; International Trade Agreements (ITAs) and Double Taxation Agreements (DTAs). These were intended to support the flow of investment, promote exports and fairly divide taxing rights between countries. These instruments, particularly double tax treaties, have become a popular tool to reduce tax related barriers and provide certainty to foreign investors. The underlying assumption is simple, if investors are protected from being taxed twice on the same income, they will be more willing to invest across borders. Over the past few decades, both developed and developing countries have actively signed these treaties, expecting to boost the foreign direct Investment (FDI), create jobs and accelerate economic growth. These agreements are a debate for researchers, some have suggest that double tax treaties are eroding the domestic tax base of developing countries while others have concluded that double tax treaties promote development, encourage investors to invest and thereby expand the tax base[1].

Internationally there are more than 2500 International Investment Agreements (IIAs) in effect. This includes over 300 bilateral treaties and also contains important rules and protections related to investment. In this connection, Pakistan may also list and adopt these treaties and is a useful case to study because it signed many international economic agreements quickly during 1980s, 1990s, 2000s and 2010s. Interestingly, Pakistan signed the world’s first ever investment agreement with Germany in 1959. It was one of the first developing country to sign tax treaties with major powers like UK and then with USA and so on. Infact, Pakistan was the first developing country to sign a treaty with the United States. However, this rush may have come with a cost. It is believed that due to these agreements, Pakistan bears a significant loss and this loss is linked to tax base erosion, tax evasion and illegal movement of money, called illicit financial flow by multinational companies operating in the country[2]. Such studies clearly highlight that the majority of developing countries are now generally thought to have entered into these treaties without first going through a cost-benefit analysis and without become integrated into or associated with broader macroeconomic structure.

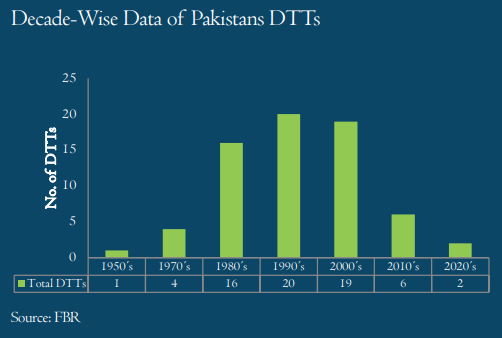

So far, Pakistan has signed 68 DTTs with the expectation that these agreements would bring in foreign investment and contribute to the country’s economic growth. However looking at the outcome so far, these goals have not been achieved and have created loopholes that are being misused. For example the domestic investors, in the hope of gaining some incentives, send their capital abroad through any illegal sources or shelf companies and then bring it back into home countries as indirect FDI known as Round tripping FDI. They often invest this money in brownfield projects, allowing them to claim tax benefits meant for genuine foreign investors. As a result, the government gains nothing from such arrangements and continues to face a growing budget deficit and during the period for making policies of trade liberalization amounting to $30 billion capital flight takes place[3].

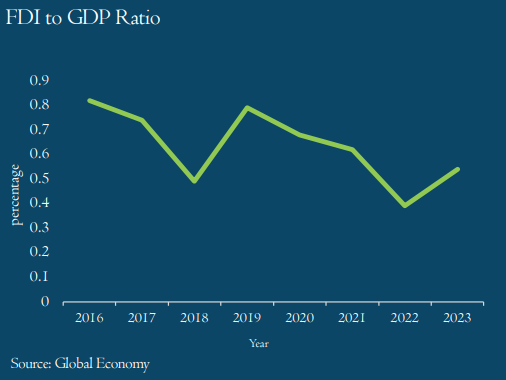

In many developing countries, including Pakistan, a lack of proper record-keeping makes it challenging to distinguish between value-seeking investments which contribute to growth and rent-seeking investments, which may lead to revenue loss. In 2023, Pakistan’s FDI-to-GDP ratio stood at 0.54%, up from 0.39% in 2022. However, this ratio remains relatively low compared to India, which had an FDI-to-GDP ratio of about 1.5% in 2022 and 2% in 2023, as shown in the figure below.

There are two distinct concepts at play, trade and tax treaties. It is a common misconception that both serve the same purpose. In reality, they are designed for different economic objectives. While both may involve the use of tax rates as a tool, trade treaties primarily focus on reducing tariffs to promote the exchange of goods and services, whereas the tax treaties aim to eliminate double taxation to encourage cross border investment and promote easy of doing business. Since early 2000, Pakistan participation in ITAs is steadily proceeding. In 2004, Pakistan has joined the South Asia Free Trade Area (SAFTA) along with Afghanistan, Bangladesh, Bhutan, India, Maldives, Nepal and Sri Lanka. This marked a significant step in economic integration efforts. Subsequently Pakistan has operationalized its FTA with Sri Lanka in 2005, followed by the Pakistan-Iran PTA, which became effective on September 2006. The trend continued with the signing of PTAs with Mauritius on July 2007. During this period, Pakistan also engaged in negotiation with china. Below the graph provides a decade wise ITAs Pakistan sign.

This distinction between trade and tax treaties become even more important in light of rising concern over the abuse of tax treaties, particularly by multinational enterprises engaging in treaty shopping, tax avoidance and profit shift to low tax jurisdictions. To address these challenges, the Organization for Economic Corporation and Development (OECD) launched the Base Erosion and Profit Shift (BEPS) initiative. This global reform aims to close the loopholes in international tax rules and minimum corporate tax rate of 15% reducing the incentives for companies to shift profit to tax heavens to avoid paying taxes. The OECD inclusive framework on BEPS is a global platform established in 2016, for cooperation and collaboration on international tax matters to try and improve global tax problems and the framework was created as a way for countries to work collaboratively on solution. One of the key elements of the BEPS action plan is the Multilateral Instrument (MLI), which seeks to update existing tax treaties in line with new anti-abuse standards. For developing countries like Pakistan which has signed a large number of bilateral tax treaties over the decades without computing their benefits and the BEPS framework offer both a challenges and opportunities. On one hand it exposes the vulnerabilities in Pakistan tax treaty network and other side, it provides a framework to renegotiate outdated agreements and protect the domestic tax base more effectively.

As a part of its commitment to international tax reform under the BEPS framework, Pakistan became a signatory to the Multilateral Instrument (MLI), allow updating and aligning its existing tax treaties with international standard aimed at preventing treaty abuses. Through the MLI, 21 of Pakistan’s bilateral tax treaties have been brought under the new global standards, particularly to limit treaty shopping, strengthen anti-abuse provisions, and improve dispute resolution mechanisms. The BEPS framework is not necessarily easy for developing countries to adopt, even though it includes a well define 15 point action plan because BEPS action requires technical expertise, legal reform, administrative capacity and international negotiation skills, which developing countries often lacking.

In the race to attract foreign investment, developing countries like Pakistan have embraced international tax treaties with high expectations but often without fully assessing their long-term consequences. Rather than delivering sustainable economic growth, these agreements have opened doors to tax avoidance, capital outflows, and abuse by both foreign and domestic actors. This paper sheds light on how Pakistan’s rapid and extensive adoption of such treaties, absent strong oversight and strategic alignment, has weakened its tax base and distorted investment incentives. By contrasting trade and tax treaties, and examining global corrective measures like the OECD’s BEPS framework and the Multilateral Instrument (MLI), the analysis calls for a more cautious, evidence-based, and reform-oriented approach to international tax policy, one that protects national interests while engaging with the global economy on fairer terms.

Ms. Karishma Kiran is a M.Phil. scholar at the Pakistan Institute of Development Economics

[1] https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2398438

[2] https://poverty.com.pk/index.php/Journal/article/view/469/414

[3] https://file.pide.org.pk/pdf/PDR/2013/Volume1/1-15.pdf