Export-led growth remains a distant dream in Pakistan and the country’s exports have not seen any remarkable increase. Effective policymaking and institutional competency remain the biggest bottlenecks. The establishment of Export Processing Zones (EPZs) in Pakistan began in the 1980s and after four decades of operation, the exports from the EPZs have hovered around $1 billion. Investors face bureaucratic hurdles, manual procedures, and dual controls, contributing to the high cost of doing business and stagnation.

Pakistan began establishing EPZs with the objective of promoting and facilitating exports. The rationale for establishing bonded areas was to ensure the efficient provision of services and to avoid the bureaucratic hurdles that are prevalent throughout the country (Akhtar, 2003[1]). The unique feature of EPZs is a special regulatory environment with additional fiscal and non-fiscal incentives (Aggarwal, 2005[2]). One-window facility eases investors’ access to the requisite approvals and infrastructure to facilitate manufacturing activities. It is pertinent to highlight that EPZs were designed for micro and small-scale industries, which have limited capital to purchase land and build infrastructure, and require government support and facilities to enable them to compete globally. Moreover, a cluster-based approach is usually adopted, in which the cohabitation of suppliers, manufacturers, and service providers optimizes supply chains, transfers knowledge and skills, and leads to joint ventures, business development, and economies of scale.

This article is based on the research carried out for the Export Processing Zones Authority (EPZA[3]), which evaluates the performance of EPZs, highlights the challenges faced by investors and presents a way forward to improve the performance of the zones.

Background and Performance Assessment

Pakistan initiated work on EPZs with the promulgation of the EPZA Ordinance, the formation of the Export Processing Zones Authority in 1980, and the issuance of guiding principles in the form of the EPZA Rules in 1981. There are six operational export processing zones in Pakistan: Karachi, Sialkot, Gujranwala, Risalpur, Daddur and Saindak, with cumulative exports of $910 million[1] in 2023. Karachi Export Processing Zone (KEPZ) has two operational phases, covering 211 acres and 94 acres, with the third phase under planning. Rislapur Export Processing Zone (REPZ) has an area of 92 acres and operations started in 2002. Saindak Export Processing Zone is a single industrial unit zone operational since 2003, covering 1,284 acres. Sialkot Export Processing Zone (SEPZ) has an area of 238 acres and became operational in 2005. Gujranwala Export Processing Zone (GEPZ) has an area of 113 acres and became operational in 2013. Dadduar Export Processing Zone is also a single industrial unit that started operations in 2009.

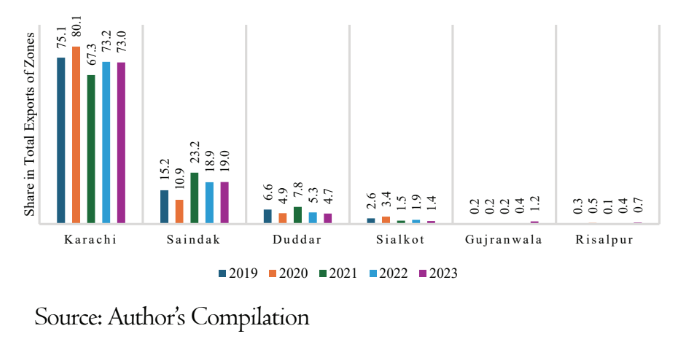

Exports from zones have not shown substantial improvement over the last couple of years. The share of zone exports in the country’s total exports increased from 2.85 percent in 2019 to 3.28 percent in 2023, amounting to $218 million. The comparative analysis of zone exports indicates that KEPZ has the highest share. The export of KEPZ stood at $665 million while its share declined from 75.1 percent in 2019 to 73.1 percent in 2023 (Figure 1). Export of Saindak stood at $173 million and its share increased from 15.2 percent in 2019 to 19 percent in 2023. Export of Duddar cloaked at $43 million and its share in total exports of zones declined from 6.6 percent in 2019 to 4.7 percent in 2023. The shares of Sialkot, Gujranwala, and Risalpur have been less than 2 percent, with exports of $11.8 million, $10.3 million, and $6.3 million, respectively.

Figure 1: Export Performance of EPZs

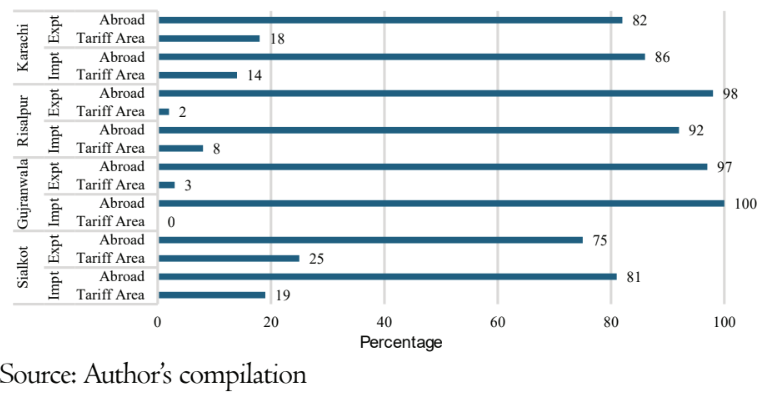

The analysis of trade composition is important, as EPZs were developed to use local raw materials and export at least 80 percent of production. In the case of KEPZ, around 86 percent of the raw materials used are imported from abroad, while 14 percent is imported from the tariff area (Figure 2). Moreover, KEPZ is exporting 82 percent abroad, while 18 percent is to the tariff area. In the case of GEPZ, the industrial units are consuming 100 percent of imported raw materials, which contradicts one of the objectives of using local raw materials. Moreover, GEPZ exports 97 percent abroad and 3 percent to the tariff area.

In the case of SEPZ, around 81 percent of the raw materials used are imported from abroad, while 19 percent is imported from the tariff area. Moreover, SEPZ is exporting 75 percent abroad while 25 percent to the tariff area, which is in contradiction to the EPZA rules. In the case of REPZ, around 92 percent of the raw materials used are imported from abroad, while 8 percent are imported from the tariff area. Moreover, REPZ is exporting 98 percent abroad, while 2 percent to the tariff area. The analysis indicates that all zones use imported raw materials rather than local inputs.

Figure 1: Composition of Trade

The zones have shown some improvement in exports. However, it is critical to evaluate the growth in real terms, which could be indicated by value addition. The value addition implies a difference between imports and exports in dollar terms. Value addition is higher in zones with higher levels of manufacturing and processing activity. The highest value addition is observed for REPZ cloaking at 54 percent or $2.6 million. In the case of SEPZ, exports stood at $12.4 million, imports at $8.5 million, and value addition are $3.9 million, or 46 percent (Figure 3). In the case of KEPZ, exports stood at 585.7 million, imports at $333.7 million, and value addition are $143.5 million, or 43 percent.

In comparison, the exports of GEPZ are $11.4 million, imports are $9.8 million and value addition are $1.6 million or 16 percent. The lower value addition of GEPZ results from its narrow focus on recycling and processing, importing scrap and exporting raw metal billets without graduating to manufacturing sophisticated or consumer goods.