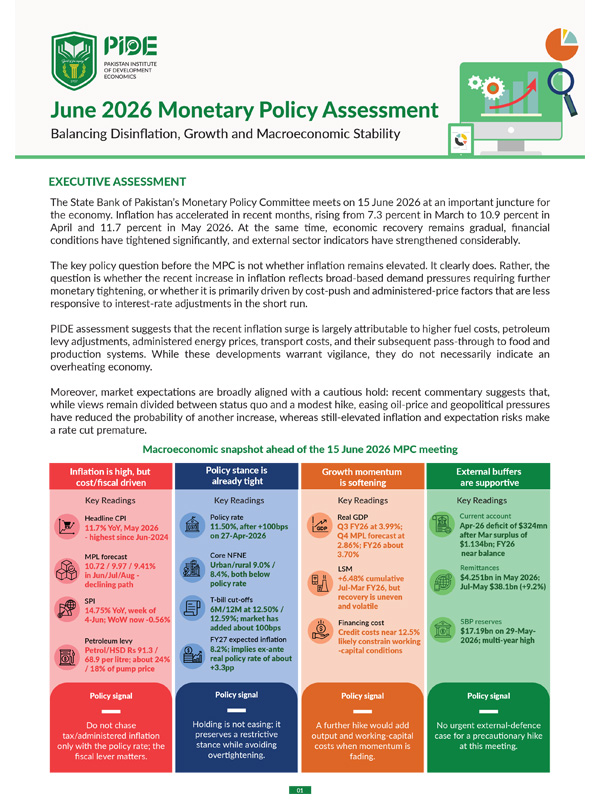

Balancing Disinflation, Growth and Macroeconomic Stability

Executive Assessment

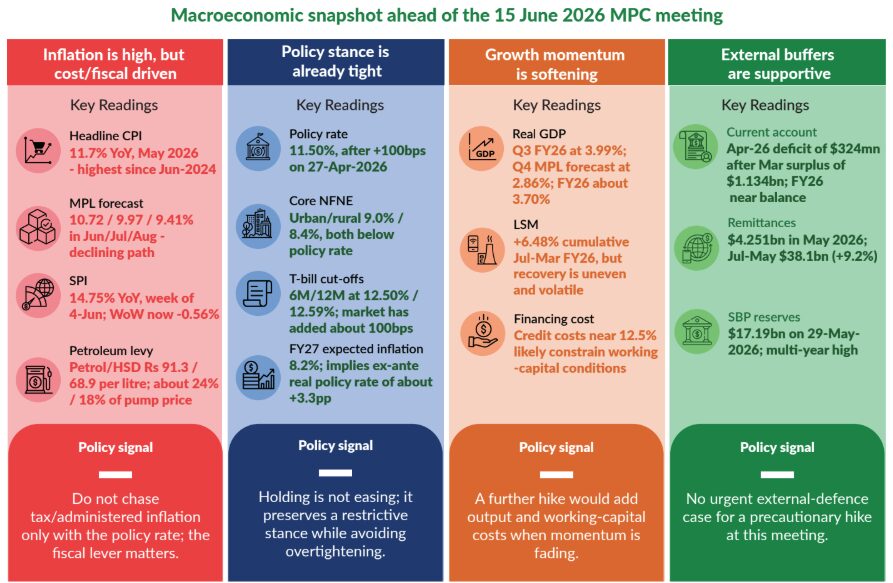

The State Bank of Pakistan’s Monetary Policy Committee meets on 15 June 2026 at an important juncture for the economy. Inflation has accelerated in recent months, rising from 7.3 percent in March to 10.9 percent in April and 11.7 percent in May 2026. At the same time, economic recovery remains gradual, financial conditions have tightened significantly, and external sector indicators have strengthened considerably.

The key policy question before the MPC is not whether inflation remains elevated. It clearly does. Rather, the question is whether the recent increase in inflation reflects broad-based demand pressures requiring further monetary tightening, or whether it is primarily driven by cost-push and administered-price factors that are less responsive to interest-rate adjustments in the short run.

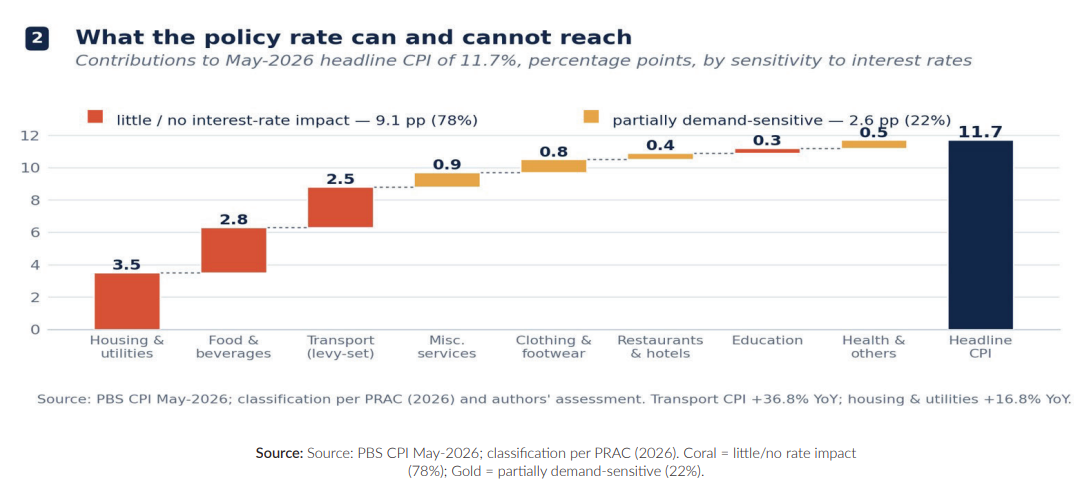

PIDE assessment suggests that the recent inflation surge is largely attributable to higher fuel costs, petroleum levy adjustments, administered energy prices, transport costs, and their subsequent pass-through to food and production systems. While these developments warrant vigilance, they do not necessarily indicate an overheating economy.

Moreover, market expectations are broadly aligned with a cautious hold: recent commentary suggests that, while views remain divided between status quo and a modest hike, easing oil-price and geopolitical pressures have reduced the probability of another increase, whereas still-elevated inflation and expectation risks make a rate cut premature.

Monetary Conditions Remain Restrictive

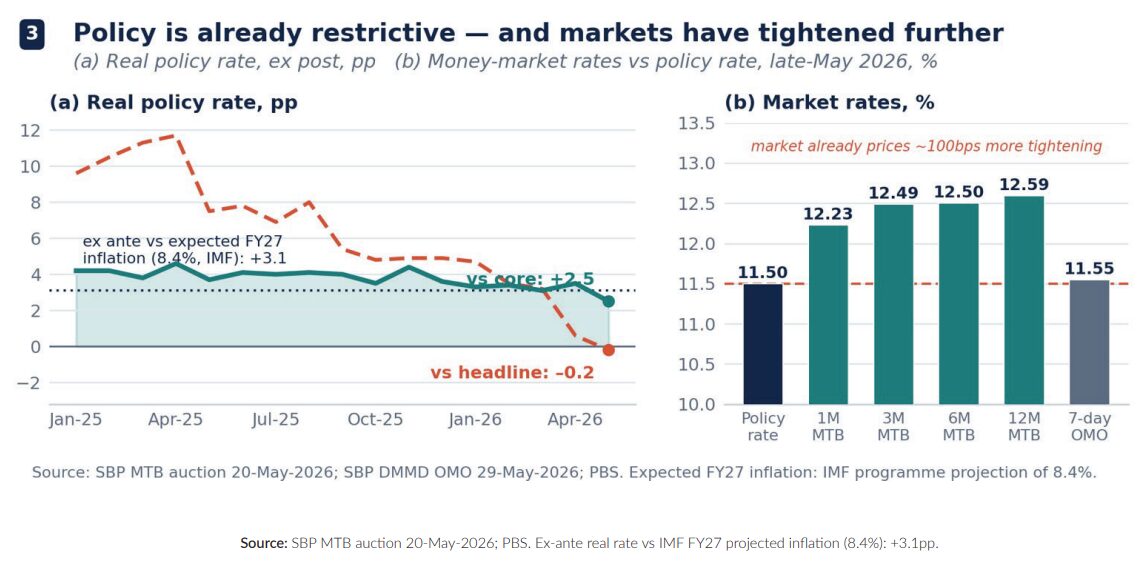

Monetary policy has already moved into restrictive territory. Following the increase in the policy rate to 11.5 percent, both policy and market interest rates remain above prevailing core inflation measures and above expected inflation over the coming year.

Financial markets have also incorporated additional tightening through higher treasury bill yields and interbank rates. Consequently, monetary conditions facing businesses and households are materially tighter than suggested by the policy rate alone.

In this environment, further tightening may yield limited near-term benefits in reducing cost-driven inflation while imposing additional costs on investment, working capital financing, industrial activity and private-sector expansion.

Inflation Risks Require Continued Vigilance

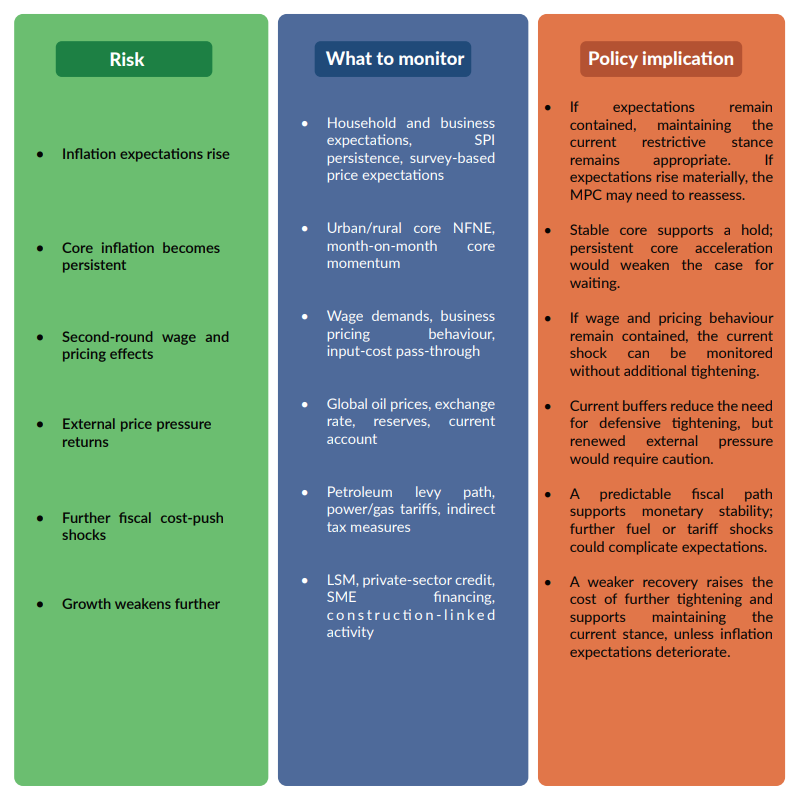

The recent inflation acceleration should not be dismissed. Persistent cost shocks can eventually influence inflation expectations, wage negotiations and price-setting behaviour. If households begin to expect higher inflation, workers demand compensation, and firms adjust prices pre-emptively, a cost-push shock can become more persistent.

Moreover, global energy markets remain vulnerable to geopolitical developments, while imported inflation risks cannot be ruled out. For this reason, maintaining credibility in the monetary policy framework remains essential. Any policy decision should continue to signal the State Bank’s commitment to medium-term price stability and inflation expectations management.

Growth Considerations Matter

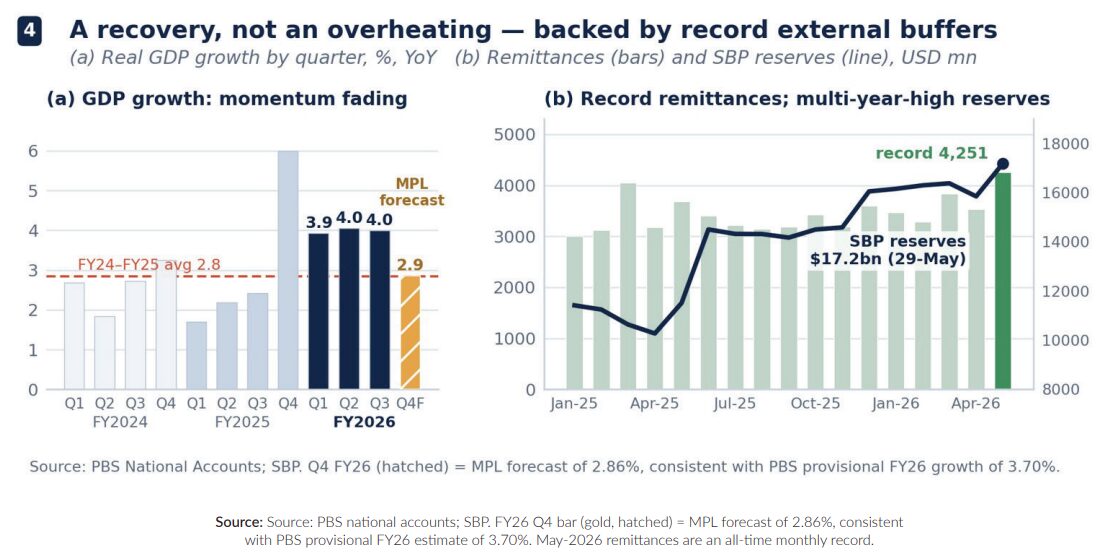

Pakistan’s economy has shown encouraging signs of stabilization during FY2025-26. However, the recovery remains uneven and fragile. Industrial activity, private investment, construction, transport-linked activity and SMEs continue to face elevated financing costs and uncertain demand conditions.

Additional monetary tightening at this stage could disproportionately affect productive sectors without materially reducing the principal drivers of current inflation. This is particularly relevant where firms rely on short-term borrowing for working capital, inventories and production finance.

External Sector Provides Greater Policy Space

The external position has strengthened significantly compared to previous years. Foreign exchange reserves have reached multi-year highs, remittance inflows remain robust, and the current account position remains broadly manageable.

While global uncertainties continue to pose risks, the immediate need for defensive monetary tightening to protect external stability appears considerably weaker than during earlier episodes of macroeconomic stress. External conditions therefore provide some policy space, although continued monitoring of oil prices, import payments, reserves and exchange-rate pressures remains necessary.

Policy Assessment

On balance, current macroeconomic conditions suggest that maintaining the policy rate at its existing level would be consistent with preserving a restrictive monetary stance while allowing policymakers to assess the persistence of recent inflationary pressures.

Accordingly, the most prudent course for the June 2026 MPC appears to be maintaining the current policy rate while closely monitoring inflation expectations, core inflation trends, external developments and evolving domestic demand conditions. A hold should be framed as a conditional and data-dependent pause, not as easing or complacency. If inflation expectations become unanchored, second-round effects broaden, or external pressures intensify, the case for further tightening would strengthen.

ANNEX A: INFLATION DECOMPOSITION

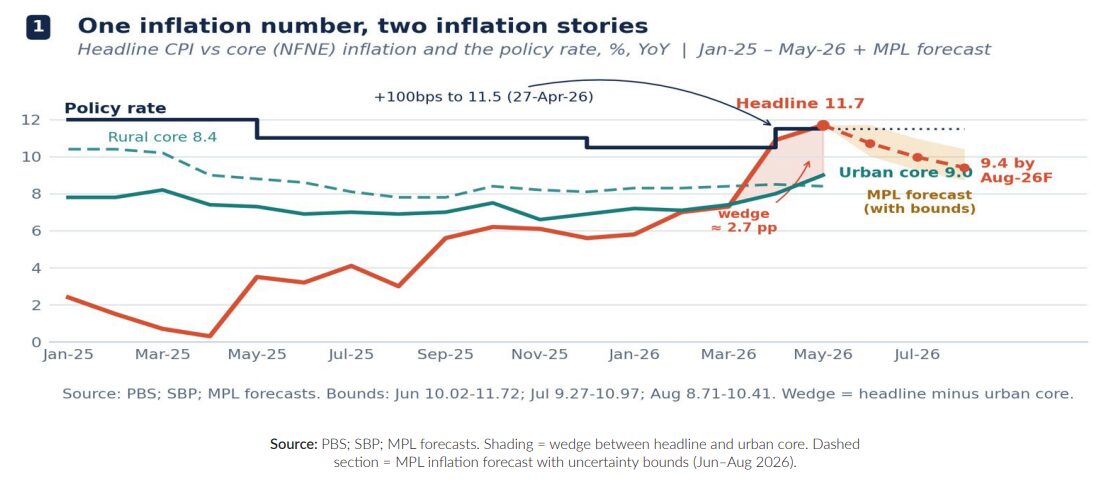

Figure A1: One inflation number, two stories — headline vs core inflation and the policy rate (%, YoY)

Figure A2: What the policy rate can and cannot reach —

contributions to May-2026 CPI (pp) by interest-rate sensitivity

ANNEX B: MONETARY CONDITIONS

Figure B1: Monetary policy already restrictive — real policy rate (a) and money-market rates (b)

ANNEX C: GROWTH INDICATORS

Figure C1: A recovery, not an overheating — GDP growth by quarter (a) and external buffers (b)

ANNEX D: KEY RISKS TO THE OUTLOOK