Macroeconomic Challenges Post-covid

There have been some benign trends in the ‘teen years’ of the 21st century (2013-19) with declining poverty, convergence (reducing gap between rich and the poor), and higher growth rates. All these positive trends have reversed through an encompassing global trend started around 2015-16 till covid-19, that rustled up the so-called Reversal problem.

The Reversal Problem which is demonstrated by World Bank Vice President Carmen M. Reinhart as a major setback on many macro-variables of the economy has been analyzed throughout the webinar. The whole webinar discussion encountered the major changes in macroeconomic activities at a global level. The debate revolved around the major challenges countries faced after the pandemic ended.

According to Carmen, the declines in GDP (output) per capita, widening inequalities across countries, fiscal deficits, rising debt levels, average total external debt servicing, and most importantly inflation and poverty are the key macroeconomic problems posing challenges to policymaking in emerging as well as advanced economies; a more critical scenario than ever.

The speaker sundered the world economies into two blocks: The Emerging and Developing Economies (EMDEs), and the Advanced Economies (AEs).

Key points:

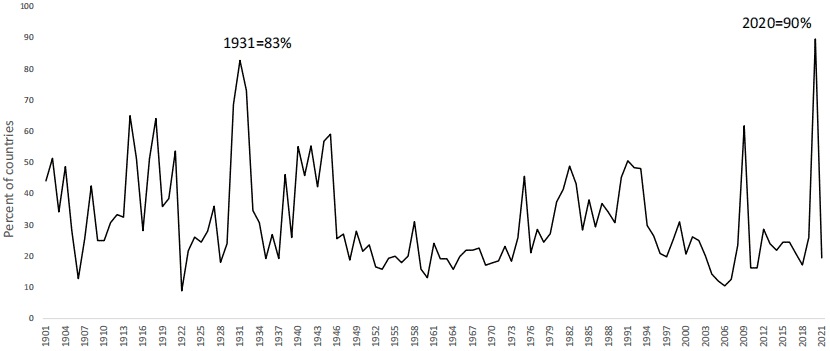

- Shares of countries with declines in per capita GDP (output) globally from 1901 to 2021, show a massive boom only two times. As in 2020, it stood at 90% while this was at the peak before at the times of 30’s great depression, during 1931 stood at 83%.

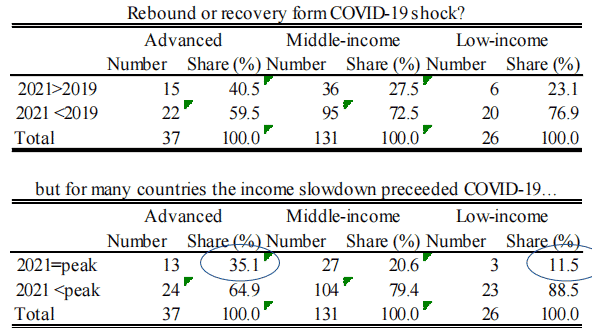

- Rebound or Recovery from such decline in real GDP per capita paints a different picture for advanced and emerging economies separately. Grouping the countries into three subgroups the findings conclude that:

- Advanced economies remained efficient in recovering from Covid-19 shocks by a percentage share of 40.5% in post-pandemic (2021>2019) from pre-pandemic (2021<2019) score of 50.9%.

- Middle-income countries with score of 27.5% (2021>2019) from 72.5% (2021<2019). Which is one of the two sub-categories of countries hit badly by Covid-19 and remained poor in recovery.

- Low-income countries with a score of 23.1% (2021>2019) share of recovery from a share of 76.9% (2021<2019), remain the most lingered in terms of recovery from pandemic shocks.

- Another detrimental impact of the pandemic on global economies has been the widening of inequalities. However, the effects vary by country. Inequalities tend to expand in poor countries following the outbreak from 2020 to 2021, whereas they lessen as one travels from poorest to richest countries. The year 2020-21 remained one of the most uneven reversals years of convergence progress.

- Fiscal deficits remained at the highest levels ever in 1982, 2008-10, and 2020. The uneven recovery from shocks leads to large fiscal deficits. While in the case of Pakistan, the rebound in GDP and the issue of over-heating economy, it sounds according to Carmen, a recovery but when it comes to per capita income it is still below what it was before the pandemic shock. The current reason for an over-heated economy is that the estimated potential outputs have been lowered, not because this has been a full recovery rather as to where the economy was before the crises.

Large financing needs to be accompanied by twin deficits (fiscal plus external) to add fuel to the fire. In the case of Pakistan, it adds more to vulnerabilities of the overall economic environment of the country.

- Rising debts are another problem of the post-pandemic world. The scenario for rising debt levels was being divided into four major debt build-up eras. The point to ponder here was that this scenario in the graph was about pre-shock debt build-ups. The levels for debt rise started quite before the crises and worsened the situation after crises. Debt accumulation averaged 45.8 percent in 1982, 37.6 percent in 2008, 55.9 percent in 2019, and 72.4 percent in 2021.

Debt levels for EMDEs remain significantly lower than those of AEs. However, the issue deteriorated due to the former ones’ scant tolerance level. Debt restructuring is a common practice in emerging markets. Carmen Reinhart stated that “if one scrutinizes foreign debt restructuring in EMDEs since WWII, more than half of them occurred at debt levels that would have met mastery criteria.” It appears that huge debt levels, such as those reported in AEs, are not required to cause a debt crisis.

- Debt servicing is a dilemma of both AEs and EMDEs. It remains clear that the debt servicing and interest payments for AEs have been on a secular downtrend, but this isn’t the case for EMDEs. As debt servicing has been on the rise for external debt. Since 2010, debt servicing as a share of exports has doubled in EMEDs.

- Inflationary pressures are reminiscent of 1970. Supply shocks bottlenecks and specifically increases in transport cost induced inflationary pressures. While Central banks’ stimulus remained ineffective in usual cases in the past. Central banks’ policy in the past, was on doing too little and too late. As central banks’ stimulus packages led to a cumulative increase in inflation. Carmen thinks, there’s a real danger whatever tightening may get in 2022 that the tendency for major banks would be very cautious about the magnitude and timing of their withdrawal.

- Poverty rates are now above pre-covid19. Flagship spot rates state that global poverty rates have increased for the first time since 1988. Considering the table titled ‘extreme poverty in 2021 versus 2019’, it was revealed that the world poverty rate rose to 70% in post-pandemic years while it was 30% in pre-pandemic years. Dividing the world into five major regions, the table further revealed that in Latin America-Caribbean, Middle East-North Africa, Sub-Saharan Africa, and eastern-Europe Central Asia’s poverty rates rose from 32% to 68%, 25% to 75%, 22% to 78%, and 44% to 56% from pre- to post-pandemic years, respectively. While only for East Asia Pacific it declined from 57% to 43% in post-pandemic years.

Considering the poverty rates of Sub-Saharan Africa, the number of poor has increased from 22% in 2019 to 78% in 2021. Carmen dictated that extreme poverty in low-income countries has rapidly increased, setting back progress by eight to nine years, while progress in upper-middle-income countries has been set back by five to six years.

- Covid19 had a significant impact on human capital which is the key driver of long-term economic growth. Though schooling has progressed but unevenly impacted those countries that were already doing worse in terms of human capital accumulation. While transitioning towards a greener economy there is a need for heavy financing and an increase in fiscal expenses so there is a difficult policy dilemma. This could have long-lasting drastic impacts on productivity and output levels. It necessitates that all the indices for human capital (poverty, inequality, education, and health) need to have more or less government spending.

On the contrary, Fiscal expansion despite indebtedness, debt servicing costs suggests that fiscal expansion of continuing build-up debts has additional risks. Similarly, expansionary monetary policy could also not be much beneficial, so it was suggested to use tighter measures by central banks to keep inflation at bay.

Q/A session:

Questions put forward by the moderator, Dr. Nadeem-ul-Haque:

- What could be the impact of tighter monetary policy if a central bank like Federal Reserve, uses tighter measures to curb inflation?

- Where would you put Pakistan’s economy on Phillips’s curve, where the economy is too young with massive poverty and high unemployment rates?

- What are your thoughts on a consensus that needs to emerge the need to meet the very difficult situation?

Emerging markets must indeed do more and sooner than AEs is precise because of the capital inflow and outflow problem. As AEs do a little tightening, this would have a multiplier effect on EMDEs as this would result in capital outflow from developing economies. Sovereign risk premium tends to rise with international interest rates go high. It would have outsized effects on interest rates and debt servicing in emerging markets and a high perception of risk with currency depreciation.

Eventually, central banks’ response in EMDEs in response to higher perceived risk, capital flag, capital flow, reversal currency depreciation is the tightening monetary policy.

Austerity is inflation, and nobody votes for inflation. Inflation is a tax that is levied, and people do not vote for such tax. Austerity is part of the Reversal Problem. And if tightening measures are taken then it would have harsh consequences. As tightening restrictions with harsh times seldom are associated with good outcomes.

The situation is extremely difficult in different dimensions. Debt restructuring is pretty long. It usually takes seven years for creditors and debtors to resolve. So, it will linger and cannot be resolved soon. Whereas the austerity measures are kept in focus. Revenue mobilization can be considered more.