Introduction

Over the course of Pakistan’s history, sustainable economic growth has been hampered by recurring periods of growth followed by spells of economic crisis. This volatile economic growth is because of the balance-of-payments (BOP) constraint. Pakistan’s export-to-import ratio has declined from 86% in 2001 to 53% in 2026[1]. Imports have continued to outweigh exports, leading Pakistan to face a payments imbalance. But the question remains: Why does Pakistan’s economic growth continue to be BOP-constrained? Theoretically, if the BOP-constrained economic growth is less than the actual average growth rate during the same period, the economic growth is said to be BOP-constrained. Practically, there are two underlying reasons for the BOP constraint. One, there is a prevalent current account deficit, and two, there is no considerable financial support in the form of foreign exchange reserves. Thus, it is imperative to promote export-led growth to overcome this constraint.

The Export-led growth hypothesis states that export growth is one of the primary drivers of economic growth. Economic growth can be increased not only by growing the amount of labour and capital in the economy, but also by boosting exports. Empirical evidence[2] indicates that imports are highly correlated with relative prices and income, and that the BOP equilibrium growth rates correspond to real growth rates. However, the literature frequently overlooks the BOP in favor of highlighting the significance of exports for promoting economic development and efficiency. Krugman[3] and other prominent economists have bluntly discarded the demand-side explanation for variations in growth rates being proportionate to differences in demand elasticities. Further, substantial shifts in production specialization are required for countries to sustain high economic growth rates[4]. Thus, it is imperative to achieve both an increase in export growth and a reduction in the income elasticity of demand for imports simultaneously.

Trade Woes

Historically, periods of rapid economic growth in Pakistan have been accompanied by disproportionately large increases in imports. This was attributable to three reasons. First, energy imports accounted for a major portion of the increase in total imports. Pakistan lacked sufficient energy supply and had an energy mix that relied heavily on non-renewable sources, such as imported oil and natural gas. Imported furnace oil was frequently used to power small generators during load shedding, as well as by industries to meet demand during periods of rapid economic growth. Second, as Pakistan did not manufacture essential machinery for infrastructural growth, it continued to rely on imports. Third, previous investments did not strengthen the country’s production capacities, allowing them to replace certain imports and move its pattern of specialization toward more advanced items.

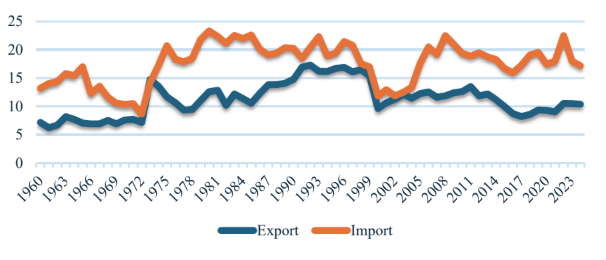

For decades, Pakistan’s export performance has been poor. Since 2005, export growth has remained sluggish, and the average trade imbalance has increased (see Figure 1). Pakistan’s exports continue to lose market share as the share of crude exports increases. Such goods have high price elasticity of demand and low income elasticity of demand. As a result, Pakistan’s exports have lagged international income growth. There is also an anti-export bias, i.e., the ratio of the effective exchange rate for imports to that for exports is high. It is alarming to note that Pakistan’s export-to-GDP ratio has declined from 17.3 percent in 1992 to 10.4 percent in 2024[5]. Moreover, Pakistan continues to struggle to compete globally in trade – it is ranked 99th on the Global Innovation Index.[6]

Figure 1 Pakistan’s Exports & Imports (% of GDP)

Source: World Development Indicators (WDI)

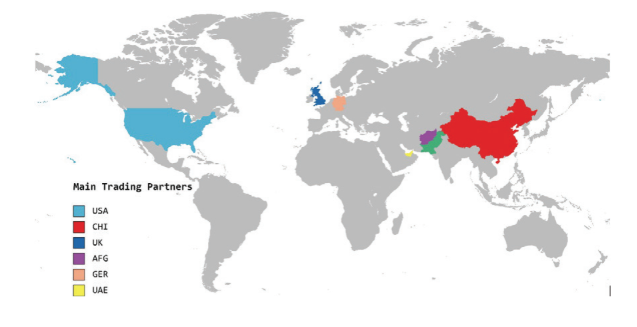

Pakistan continues to trade with nations worldwide (See Figure 2). In doing so, it has incurred trade costs due to the added travel costs. As time is money, we must not forget the immense importance of time in trading. A country like Japan would rather import a slightly less value-added product from a country that delivers it considerably faster. Unfortunately, Pakistan has failed to take these factors into account. Add to this, the trade hampering caused by political tensions between Pakistan and its neighboring countries. Pakistan is not part of any major trading bloc, with only a handful of local firms involved in the global market. Unnecessarily, Pakistan has developed a habit of protecting inefficient industries, particularly large-scale, import-oriented industries. The trade strategy is biased towards merchandise rather than export-boosting products.

Figure 2: Pakistan’s Main Trading Partners

Source: Authors’ Mapping

Sectoral Analysis

Pakistan’s economy is semi‑industrialized, with industry accounting for around 21% of GDP. However, the industrial sector suffers from low export competitiveness, high import dependence, and inadequate value addition.

Steel: The steel sector is highly fragmented, with over 500 mills. The steel industry produces around 9-10 million metric tons of steel per year. Yet the total imports of steel and related products are significantly greater than its exports. Pakistan is self‑sufficient in long products but depends on imports for flat products, especially hot‑rolled coils. In the steel sector, as advocated by the National Tariff Commission (NTC), it is pertinent to rationalize tariffs on raw materials by reducing customs duty on iron ore, pig iron, ferro‑silicon, and shredded scrap to 0%. However, re-rollable scrap now has a 5 percent duty, which should be reconsidered. This will help maintain a cascading tariff differential to protect domestic value addition. It is also essential to establish a Steel Industrial Zone near the port to create a cluster with utilities and export facilitation.

Home Appliances: The home appliances sector suffers from low localization levels for refrigerators, split ACs, and LED TVs. Consequently, most components are imported, adding to the import bill. For the home appliances sector, phased tariff rationalization with components that can be localized at escalating duties of 15 to 30% and finished goods at 40% must be implemented. This should be further promoted by localizing evaporators, motors, and other components through joint ventures and technology agreements, with zero‑duty on raw materials for such investments and the withdrawal of regulatory duties on parts and components that increase production costs and encourage smuggling.

Fans: The fan manufacturing industry imports more than half of its raw materials, including electrical steel sheets, copper, and aluminum. To enhance fan manufacturing, local production of raw materials such as electrical silicon steel sheet, ball bearings, and enameled copper wire must be encouraged. It is equally important to restore regulatory duties on the export of recycled copper, steel, and aluminum to ensure availability for the domestic fan industry.

Mobile Devices: The mobile device manufacturing policy has encouraged local assembly, yet most components remain imported. For mobile manufacturing, the existing duty differential, i.e., CKD/SKD manufacturing enjoys lower duties compared to CBU imports, must be maintained. Additionally, localization of parts and components through favorable tariff treatment and exports of locally assembled handsets must be facilitated.

Cables & Conductors: The cables and conductors industry, with many cottage units, faces high import costs for raw materials such as PVC resin, plasticizers, and XLPE compounds. The industry requires revised duties on finished goods to ensure a level playing field for local manufacturers, especially against imported cables under lower‑duty HS codes. In this regard, an increase in the DLTL rate from 3% to 6% and the extension to non‑traditional markets with an additional 2% drawback are recommended.

Transformers: The transformer industry relies on imported silicon steel, copper rod, and foil. To boost transformer production, it is imperative to reduce or eliminate the regulatory duty on silicon steel (HS 7225.1100) and copper rod/foil (HS 7408.1100, 7409.1100). This can be further supported by simplifying the Duty and Tax Remission for Exports (DTRE) process, cumulatively providing export rebates, and increasing the Drawback on Local Taxes and Levies (DLTL) rates for target markets to 5%.

Pumps, Motors & Electric Meters: Similarly, the pumps and motors industry depends on imported pig iron, electric silicon steel sheet, and ball bearings. For pumps and motors, an increase in customs duty on finished submersible motors (HS 8501.5210, 8501.5320) from 11% to 20% can protect the local industry. There should also be a ban on the import of second‑hand/used motors and pumps and enforcement of valuation rulings to prevent under‑invoicing. In the electric meters sector, reduced duties on four‑layer PCB, high‑accuracy capacitors, and lithium batteries to 0% (HS codes 8534.0000, 8532.2900, 8506.5000) can enhance local production.

Footwears: The footwear sector (the seventh-largest producer globally) ranks 50th globally in footwear exports.[7] The Pakistani footwear industry has immense export potential. It can be untapped by restricting the export of raw leather (HS code 41) through increased export taxes or a complete ban to ensure availability for domestic footwear manufacturing. A cherry on top would be the establishment of a Specialized Industrial Estate for footwear and associated manufacturers, offering land on subsidized rent or easy installments.

Surgical & Pharmaceuticals: The surgical and medical appliances sector, concentrated in Sialkot, exports mainly precision metal instruments but has yet to capture the growing global market for higher‑value appliances. On the other hand, the pharmaceutical sector imports 95% of its active pharmaceutical ingredients, exposing it to exchange rate volatility. The pharmaceutical industry essentially requires the establishment of a quality testing and regulatory authority to certify products in accordance with US and EU standards, reducing the need for expensive foreign testing.

[1]Pakistan (PAK) Exports, Imports, and Trade Partners | The Observatory of Economic Complexity. (n.d.). The Observatory of Economic Complexity. https://oec.world/en/profile/country/pak

[2] Fasanya, I. O., & Olayemi, I. A. (2018). Balance of payment constrained economic growth in Nigeria: How useful is the Thirlwall’s hypothesis? Future Business Journal, 4(1), 121–129. https://doi.org/10.1016/j.fbj.2018.03.004

[3]Krugman, P. (1989). Differences in income elasticities and trends in real exchange rates. European Economic Review, 33(5), 1031–1046. https://doi.org/10.1016/0014-2921(89)90013-5

[4]Holland, M., Vieira, F., & Canuto, O. (2004). Economic Growth and the Balance-of-Payments Constraint in Latin America. Investigación Económica, 63(247), 45-74. Retrieved June 24, 2021, from http://www.jstor.org/stable/42779050

[5]World Bank Open Data. (n.d.). World Bank Open Data. https://data.worldbank.org/indicator/NE.EXP.GNFS.ZS?locations=PK

[6]WIPO. (2025). Pakistan ranking in the Global Innovation Index 2025. World Intellectual Property Organization. Retrieved March 21, 2026, from https://www.wipo.int/edocs/gii-ranking/2025/pk.pdf

[7]TDAP. (2024). Pakistan Footwear Industry. Trade Development Authority of Pakistan. Retrieved March 21, 2026, from https://tdap.gov.pk/wp-content/uploads/2024/05/Footwear-Brochure.pdf