ABSTRACT

Pakistan’s export performance has remained chronically weak despite numerous trade liberalisation efforts and its strategically advantageous geographic position. This study synthesises over three decades of empirical literature to understand the structural, institutional, and policy-related impediments to the country’s lagging exports. The evidence demonstrates that high tariffs on intermediate inputs, limited compliance with international certification standards, energy sector inefficiencies, and exchange rate volatility significantly undermine export competitiveness. These challenges are further exacerbated by a narrow export base concentrated in low-value-added textiles, ineffective subsidy schemes, and limited utilisation of trade agreements. As a result, Pakistan has struggled to diversify into higher-value-added sectors. Addressing these constraints requires coordinated reforms, including tariff rationalisation, development of certification and quality infrastructure, improvement of the business and regulatory environment, and targeted support for sectoral upgrading to facilitate sustainable export growth.

1. INTRODUCTION

Over the past three decades, exports have emerged as a critical growth engine for sustainable and inclusive development in developing nations. However, despite successive policy reforms and a strategically advantageous location, Pakistan has struggled to develop a resilient and diversified export base to support its economy. According to the World Bank (2025), Pakistan’s export-to-GDP ratio declined from 15.4 percent in 1999 to 10.4 percent in 2024, indicating stagnation in external competitiveness, even as regional peers rapidly expanded their trade footprints. Bangladesh dominates value-added downstream textile products, India leads in IT and pharmaceuticals, Vietnam excels in high-tech and global value chains, and China is establishing itself as a global manufacturing hub. These countries focused on developing industries capable of competing globally, with substantial investments in the manufacturing and technology sectors. On the other hand, the export basket of Pakistan remains heavily concentrated, with roughly 74 percent of exports comprising low-value-added textile and apparel, leather, and rice products (Pakistan Economic Survey, 2025). From 2001 to 2024, the share of high-skill and technology-intensive exports increased only marginally, from 3.6 percent to 6.4 percent, while Vietnam and China reached 33.9 percent and 41.1 percent, respectively (UNCTAD, 2025). This limited progress reflects a continued dependence on labour-intensive sectors and a limited capacity to move up the value chain. Therefore, drawing lessons from economies such as India, Vietnam, and even Bangladesh is imperative to attain diversification and mitigate the risks associated with sectoral dependence.

A growing body of research highlights several reasons for this underperformance. On top of this, Pakistan has a cascading tariff regime that imposes an implicit anti-export bias, especially for firms dependent on imported intermediate inputs. This discourages firms from upgrading their quality or becoming globally competitive (Varela, et al. 2020; Jamil & Arif, 2019). Similarly, energy sector inefficiencies and inadequate infrastructure constitute major structural constraints, contributing to high production and trade costs. (Siddiqui, et al. 2008; Hussain, et al. 2012). Pakistan also ranks low in logistics performance, placing 122nd globally in the World Bank’s Logistics Performance Index, with weaknesses in customs processing, tracking systems, and transport infrastructure (World Bank, 2025). Governance level constraints further limit export growth. Moreover, export subsidies exist to support exporters; studies show that these often benefit large and well-connected firms rather than growing or smaller exporters (Zia, 2008; Defever, et al., 2020). Many firms also struggle to meet international quality standards due to cost and limited awareness, as Wadho & Chaudhry (2025) show that certifications facilitate exports; however, adoption is uneven, and costs remain prohibitive for smaller firms. The European Union’s Generalised Scheme of Preferences Plus (GSP+) program has facilitated growth in textile exports, although its long-term benefits depend on compliance with labour, governance, and environmental standards (Nakhoda, 2023).

In addition, Pakistan’s export markets remain highly concentrated, with over 62 percent of exports directed to the top 10 destinations as of 2024 (ITC Trade Map, 2025). This limited geographical spread reflects untapped potential in both regional and non- traditional markets. Moreover, product diversification has been modest, mainly due to small volumes and low complexity (Ahmad, et al. 2024).

This review paper synthesises over three decades of empirical research to understand the factors behind Pakistan’s stagnant export performance. Drawing on peer-reviewed articles, working papers, and policy reports, it organises evidence across key areas: tariff and non-tariff barriers, export subsidies, trade agreements, exchange rate dynamics, structural constraints, and sector-specific challenges.

2 . TRADE PROFILE AND POLICY INDICATORS

2.1. Historical Perspective on Exports

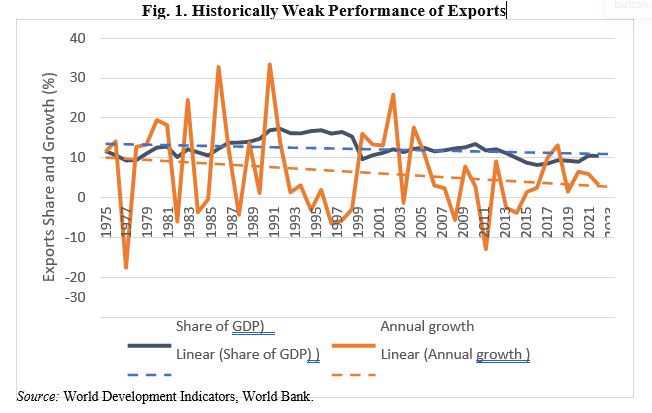

In 2024, Pakistan exported products and services worth USD 40.19 billion, representing a 10.6 percent increase compared to the previous year (Figure 3). Nevertheless, the growth of exports over the years has been highly volatile, spiking one year and bottoming out the next, reflecting structural gaps (Figure 1).

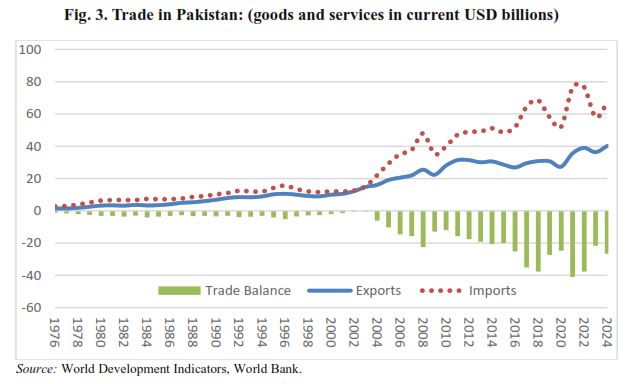

Pakistan’s key exports are textiles and related goods, which depend on raw agricultural materials such as Cotton. This dependence links export performance to the volatility of agricultural output and global demand for low-value-added goods. As a result, export growth remains vulnerable, limiting long-term sustainability and contributing to the country’s chronic trade deficit (Figure 3).

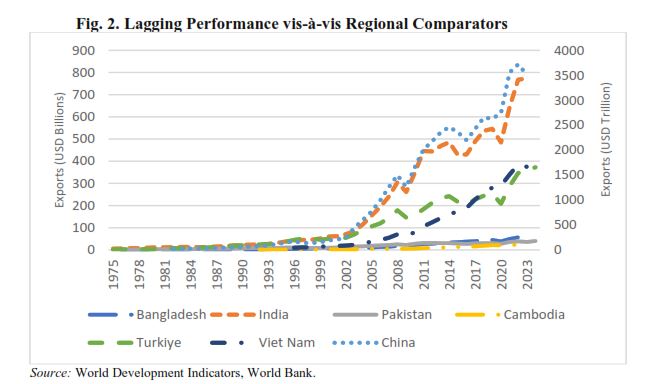

Pakistan’s exports over the past two decades have not been impressive compared to its comparators, i.e., Bangladesh, India, Vietnam, and China (Figure 2). China’s exports skyrocketed from USD 208.6 billion in 2001 to over USD 3.5 trillion in 2023, driven by structural reforms, integration into global value chains, and sustained industrial upgrading. Vietnam followed a similar trajectory, with exports increasing from USD 17.8 billion in 2001 to USD 375.1 billion in 2023, reflecting its transition to a competitive export-led economy. Bangladesh also recorded steady progress, with exports growing from USD 6.8 billion in 2001 to USD 47.3 billion in 2023, largely supported by its garment sector and policy consistency. In contrast, Pakistan’s exports increased from USD 10.5 billion in 2001 to USD 36.2 billion in 2023, reaching USD 40.2 billion in 2024, highlighting persistent structural challenges and missed opportunities in competitiveness.

Note: China is measured using the secondary (right-hand) axis due to the significantly larger export volume (in USD billion).

This stagnant performance is evident in Table 1, which, in comparison to Pakistan, shows a substantial shift in the merchandise export structures of comparator countries from 2001 to 2024.

There has been a noticeable decrease in labour intensity in China, indicating a move towards more technology-intensive industries. Remarkably, Vietnam’s transformation is prominent, from being primarily labour- and resource-intensive in 2001 to becoming more technology-intensive by 2024. In 2023, Vietnam’s key exports included broadcasting equipment (USD 83.2 billion), integrated circuits (USD 32.5 billion), and computers (USD 15.9 billion). Notably, Vietnam’s top export, broadcasting equipment, surpassed the total merchandise exports of Pakistan and Bangladesh combined (OEC, 2025). This transition reflects Vietnam’s successful move towards higher value-added and technology-intensive industries, improving its global market competitiveness.