“PayPal is not Coming Soon”. Why?

Abdul Jalil, Pakistan Institute of Development Economics, Islamabad.

PayPal is a US-based electronic payment system that acts as a third party for financial payments between two parties. After signing up for the PayPal platform, the customer is supposed to link PayPal with their debit card, credit card or bank account. After completing the procedure, the customer may receive and send money to/from their cards or bank accounts.

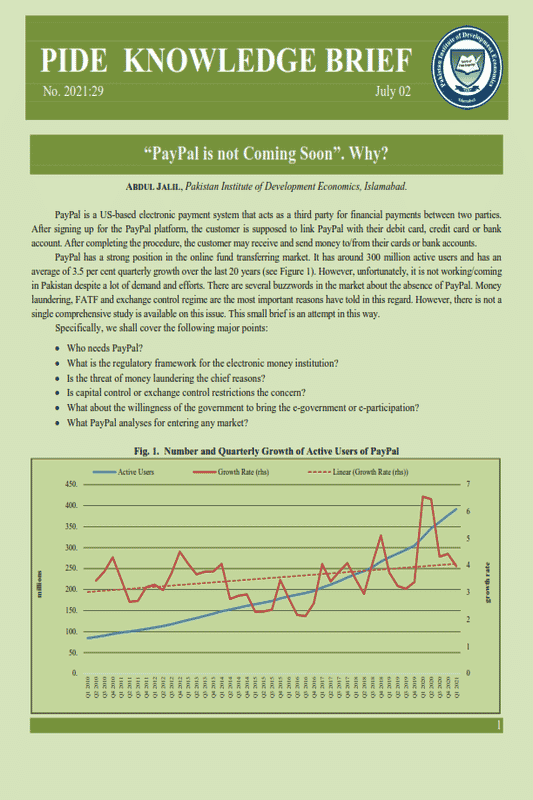

PayPal has a strong position in the online fund transferring market. It has around 300 million active users and has an average of 3.5 per cent quarterly growth over the last 20 years (see Figure 1). However, unfortunately, it is not working/coming in Pakistan despite a lot of demand and efforts. There are several buzzwords in the market about the absence of PayPal. Money laundering, FATF and exchange control regime are the most important reasons have told in this regard. However, there is not a single comprehensive study is available on this issue. This small brief is an attempt in this way.

Specifically, we shall cover the following major points:

- Who needs PayPal?

- What is the regulatory framework for the electronic money institution?

- Is the threat of money laundering the chief reasons?

- Is capital control or exchange control restrictions the concern?

- What about the willingness of the government to bring the e-government or e-participation?

- What PayPal analyses for entering any market?

1. WHO NEEDS PAYPAL

1. WHO NEEDS PAYPAL

Though PayPal is needed for a variety of financial transactions, but the freelancing community is directly connected with this service. Notably, Pakistan is a significant freelance exporter with a growing market over the last three years. Therefore, the freelancing community is facing massive trouble in receiving payments in the absence of well-trusted electronic payment service providers. Resultantly, they use informal/illegal or indirect ways for creating PayPal accounts in Pakistan.[1]

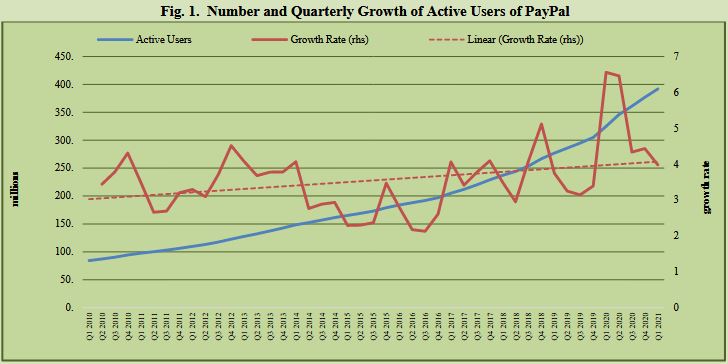

Pakistan has a good contribution in the freelance markets and has an attractive destination for offshore service. Kearney’s Global Service Location Index (GSLI) scales the location attractiveness of the countries.[2] According to GSLI of 2019, Pakistan is the 11th most attractive location in Asia for the offshore service, and its placement is at 30th number is the world’s list (see Figure 2). However, the most encouraging number is the financial attractiveness. Pakistan is 5th largest amongst the 50 country index and 3rd most prominent place in the Asian countries. Despite these encouraging facts, they do not have a trusted, user friendly, safe and worldwide accepted electronic payment system. Resultantly, they end up using risky, informal and illegal platforms for the fund transfer. In this situation, they would prefer and require PayPal, which is safer, trustworthy and offers quick services for customers. _______________________________

_______________________________

[1] There are several YouTube video available for creating/acquiring the PayPal accounts/cards in Pakistan.

[2] https://www.kearney.com/digital/gsli

2. WHY IS PAYPAL NOT COMING?

Although there are some online fund services like Skrill and Payoneer are working in Pakistan. Both platforms are linked with the bank accounts of the customers and the JazzCash account. However, there is little chance for the coming of PayPal, the most widely trusted and accepted mode of fund exchange in the world, soon despite the government’s efforts. Now the question is why PayPal is reluctant to come? There are several reasons like regulatory restriction, money laundering, fraudulent activities and capital flight.

2.1. Regulatory Concerns

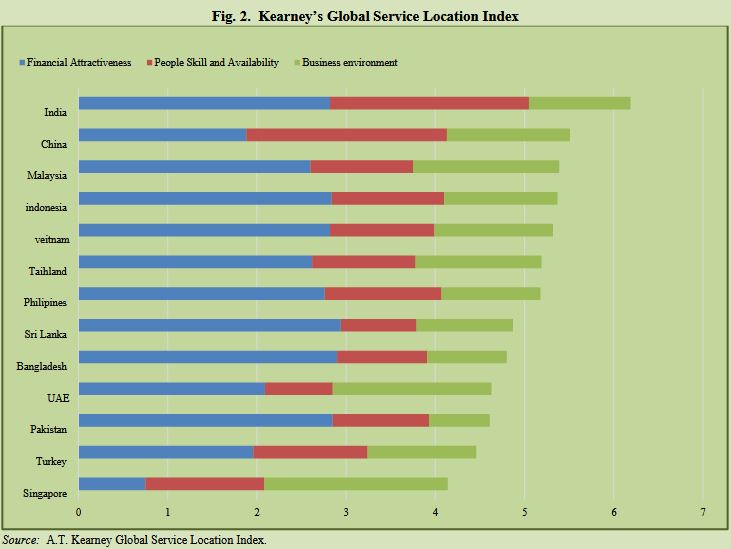

If not the only, the key concern for PayPal for entering the Pakistani market is the long list of regulatory restrictions.[3] According to the State Bank of Pakistan regulations for Electronic Money Institution (EMI), the EMI has to maintain the initial/startup capital requirement of PKR 200 million for operating in Pakistan. Furthermore, the EMIs also required to maintain the minimum ongoing capital at all times. There are different slabs of ongoing capital according to the Outstanding E-money Balance (OEB).

The second important issue in the regulatory restriction is that the payment service providers, that is EMI, would have to undergo a 3 stage approvals process for a license. First, in-principle approval, second pilot operations and third complete operations. Thus they have to give a lot of time and money to be a payment service provider in Pakistan.

In addition to this, the multiple regulations regarding customer due diligence would also be needed to be followed. After reviewing the regulations for EMI, one can easily deduct that the whole responsibility will be transferred to EMI in case of any illegal or suspected transfers of money. So, if such strict regulations existed in the US, perhaps such firms could not start a business. It may also be noted that PayPal is said to operate with minimum profit margins as compared to other online fund transfer system like Payoneer, and such high cost for regulatory purposes would not fit in their business model.

Sadly, the regulatory quality of Pakistan is almost the lowest, just above Bangladesh, amongst the Asian countries (see Figure 3). We plot the regulatory quality index. The index reflects perceptions of the ability of the government to formulate and implement sound policies and regulations that permit and promote private sector development.[4] In addition to this, the ‘Economic Freedom Index (EFI) ranks Pakistan 135th out of 180 countries (2020). Therefore, the unnecessary regulations are one of the key hurdles to invite PayPal into our market. PayPal is a business entity. Therefore, they will not come in presence of strict regulations and low profit. The Pakistani market is not a low hanging fruit for them. Businesses always flourish with incentives instead of restrictions.

_________________________

[3] See ‘Regulations for Electronic Money Institutions (EMI)’ of State Bank of Pakistan https://dnb.sbp.org.pk/psd/2014/C3-Annex.pdf

[4] See Worldwide Governance Index (2020) for more details. www.govindicators.org

2.2. Money Laundering and FATF

The other vital concern of PayPal for not entering into the Pakistani market is money laundering. There is a concern that money laundering activities have been increased in Pakistan over the past few years. Therefore, the Financial Action Task Force (FATF) has placed Pakistan on the grey list. Therefore, due to FATF, the international electronic payment service providers or EMIs have to comply with strict regulations for customers and avoid money laundering. Otherwise, the SBP has the power to cancel their licenses.[5] Therefore, the PayPal company is reluctant to come due to the strict restrictions.

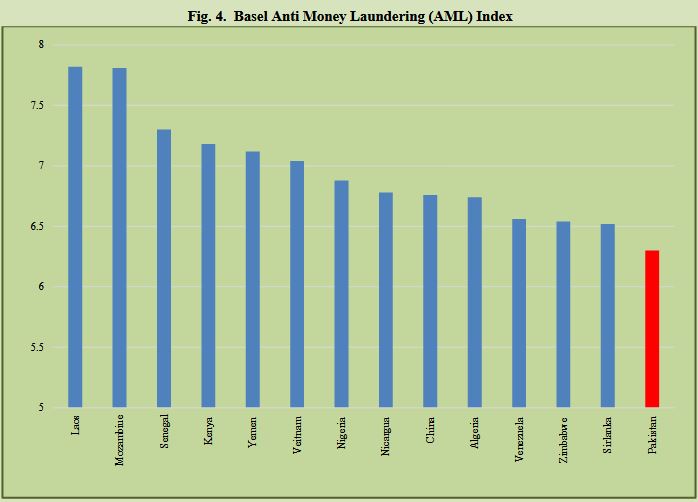

We argue that money laundering is not a big issue for the PayPal company. The company is working in several countries with a higher risk of money laundering than Pakistan (see Figure 4). We plot the Basel Anti-money laundering (Basel AML) Index.[6] It is an independent annual ranking that assesses the risk of money laundering and terrorist financing (ML/TF) worldwide.

The figure shows the countries where PayPal is working or providing full or partial services have a much higher risk of money laundering than Pakistan.[7] Interestingly, several countries are placed on the grey list of FATF but the PayPal is working in those countries fully or partially. So, the AML and the FATF is less concern from the PayPal point of view.

______________________________

[5] See ‘Regualtions for Electronic Money Institutions (EMI)’ of State Bank of Pakistan https://dnb.sbp.org.pk/psd/2014/C3-Annex.pdf

[6] See https://baselgovernance.org/basel-aml-index/public-ranking for details and data.

[7] There are three types of countries or regions according to the services of PayPal. First, the countries with the ability to send and receive payments, second countries/Regions with the ability to send and receive payments and have Automatic Transfer and, third the countries/regions with the ability to send payments.

2.3. Willingness of Government and SBP

Overall government attitude in Pakistan is not supportive of digital currency and digital payments. For example, digital currency like Bitcoin is not allowed in Pakistan. The ratio of regular users of alternate delivery channels (ATM, electronic transfers, e-wallets) is still very low in Pakistan.[8] There may also have been the issue of a central payment gateway. Although, PayPal acts as a digital wallet in the USA market, however for some countries it only acts as an institution for money transfer.[9] However, for this, there must be a central platform from where they can transfer to any bank. Such a central platform does not exist in Pakistan.

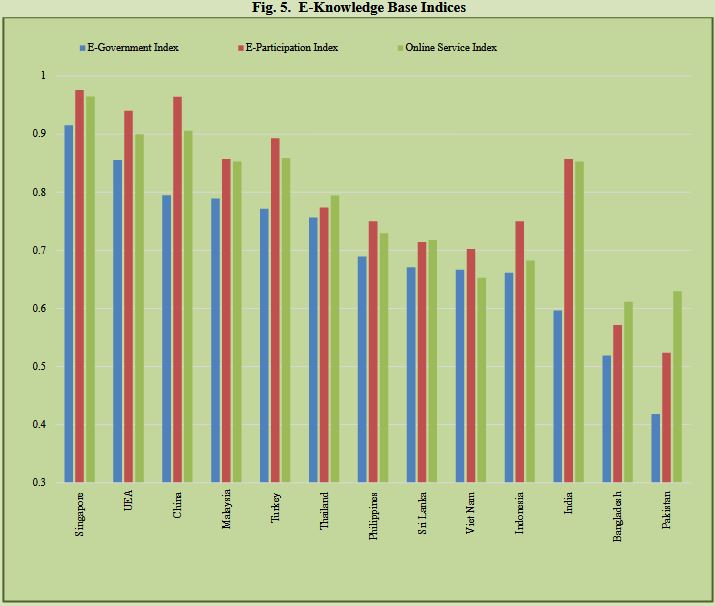

Pakistan is at the lowest position of various E-knowledgebase indices as compared to selected Asian countries. These indices are prepared by the United Nations.[10] We plot three important indices, that is, E-government Development Index (EGDI), E-participation Index (EPI) and Online Service Index (OSI). The EGDI is based on the access characteristics. That is, how the access and inclusion of information technologies are being reflected in the infrastructure and educational levels.[11] It is alarming that Pakistan is still struggling in all three indices as compared to other competitors in Asia (see Figure 5). So, there is a long way to go in this area.

_______________________________

[8] See the Payment System Review reports of SBP for further details.

[9] https://www.paypal.com/sg/webapps/mpp/ua/residence-full

[10] https://publicadministration.un.org/egovkb/en-us/Overview

[11] See the exact definitions and methodologies of all three indices at https://publicadministration.un.org/egovkb/en-us/Overview

2.4. The Capital Controls

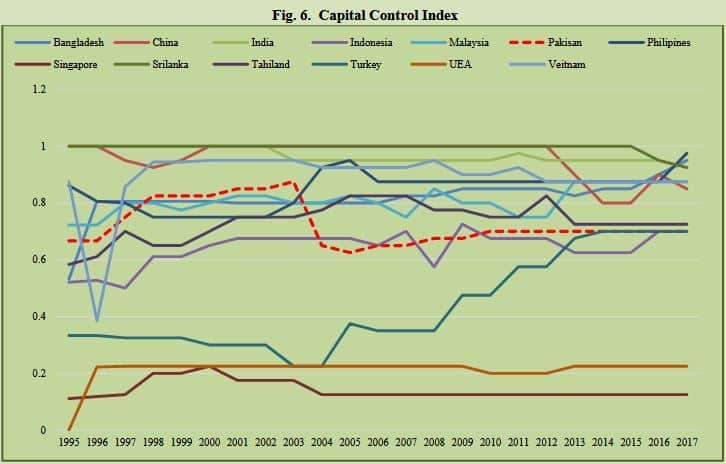

From the SBP point of view, the exchange control regime and data privacy are the major obstacles in the way of PayPal entering the Pakistani market. According to the SBP, the PayPal funds transfer mechanism is based on the bidirectional way. Therefore, the outflow of foreign exchange may create extra pressure on the external sector of Pakistan. This may be true for the other countries which have weak foreign exchange buffers. It is also interesting to note that Pakistan is not the only country that has strict capital control. In almost all countries, except Singapore and UAE, the Capital control regimes of the countries are at par or stringent than Pakistan (see Figure 6). We plot the overall capital control index (capital inflow +capital outflow) index based on IMF’s Annual Report on Exchange Rate Arrangements and Restrictions. We use Fernández, et al. (2016) version of the index.[12] Interestingly, PayPal is working in almost all countries. So, capital control is not the biggest concern of PayPal.

__________________________

[12]http://www.columbia.edu/~mu2166/fkrsu/

WHAT PAYPAL ANALYSES?[13]

We establish an argument that the FATF, money laundering, exchange control restrictions are not the bigger concerns of PayPal for entering any market. PayPal is a business company, a business with a good profit margin with a lot of ease of doing business. So, what PayPal exactly analyses before entering a market. There are a lot of things, but here we mention a few which are based on anecdotal shreds of evidence. These are related to E-commerce, payment methods, online merchants and risk management.

E-Commerce

The e-commerce business is the pivotal detriment to the existence of PayPal in any market. They are interested to look into:

- The total volume and value of online purchases by Pakistani consumers.

- Similarly, the total volume and value of online selling by the Pakistani merchants.

- The PayPal company is also interested to look into the growth rates of sale and purchase for a longer period.

- The percentage of the total online intra-border transferred money, that is, the transfer between local consumer and merchants.

- Similarly, the percentage of the online international transferred money, that is, the transfer between Pakistani and non-Pakistani consumer and merchants.

______________________________

[13] This section is based on the anecdotal evidences.

Payment Methods and Penetration Rate

- PayPal looks that what are and how many electronic/online payment methods, payment systems and platform are available for online transactions.

- What is the penetration rate of each payment system or payment method? That is, what percentage of the population owns the online payment, that is credit/debit cards. How actively they are using it.

- What is the percentage of total e-commerce activities are used by each electronic payment system?

- Importantly, they also analyse the risk profiles of these payment methods.

Online Merchants

- They also closely look at a list of some main merchants that may use the services of PayPal for their incoming or outgoing payments.

- The total online transaction volume of the major merchants is also monitored.

- The concentration of e-commerce is also important in this regard. That is, what percentage of total e-commerce/online transactions are related to top merchants.

Risk Management

- The company also analyses the list of data privacy, compliance of due diligence, and regulations that are relevant to PayPal or payment service providers.

- If there are easy ways to adopt these rules and regulation by PayPal without making major product changes then it will be a healthy sign for the starting of the business in any market.

- Are there some authentication methods available for establishing the identity of the merchant and consumers?

-

CONCLUSION

This note concludes that the regulatory framework for EMIs in Pakistan, the e-knowledgebase of the government and the market, especially, friendly market environment are the bigger concerns for PayPal. On the other hand, PayPal does not have a big issue with money laundering, FATF and exchange control regimes. If the government of Pakistan and the SBP is really serious to invite PayPal, then they have to take serious actions in this regard. The recently launched reform agenda of PIDE (2021) also argue that e-governance, optimal regulations, internet access and a friendly market environment are the key drivers for future economic activities. Therefore, this note suggests to the policymakers that this is a very critical time to think in this way. Otherwise, we will be far behind the competitors in the field of the electronic payment system, which is a key component of future transactions, in the next 5 to 10 years.

REFERENCE

Fernández, A., Klein. M. W., Rebucci, A., Schindler, M. and Uribe, M. (2016). Capital control measures: A new dataset. IMF Economic Review, 64(3), 548–574.