Remove Service Charge on IBFTs to Encourage Digital Transactions

The State Bank of Pakistan (SBP) announced on June 16, 2021, that it has now allowed banks to charge a transaction fee of 0.1 percent of the transaction or PKR 200, whichever is lower on Inter-Bank Funds Transfers (IBFTs). SBP has made compulsory free-of-cost IBFTs of up to PKR 25,000 per month per account. For accounts exceeding the limit, the banks will charge the transaction fee as mentioned above.

Following the onset of the COVID-19 pandemic, on March 19, 2020, the Government of Pakistan and SBP decided to make all IBFTs free of charge. The idea behind this decision was to limit consumer visits to banks and thus restrict the COVID-19 threat. Before that, the banks were allowed to charge a transaction fee on IBFTs as per SBP’s defined schedule of charges.

The practice did continue for a little over a year until after the third wave, the state bank, as mentioned above, assumed an improved COVID-19 position for reviewing the policy and thus reimposed the charges on digital funds transfer. Since then, Pakistan has entered the fourth pandemic wave as a much deadly delta variant and other new variants grow rapidly in Pakistan. Consequently, the basis of this review and policy change can be contested on the pandemic spread grounds, but for now, this policy viewpoint discusses the decision from an economic and financial perspective.

The policy viewpoint will establish an evidence-based impact of change in transaction fees by looking at transaction data, the volume of IBFTs, and other relevant data points. The initial hypothesis is that transaction fee on IBFTs discourage the public from adopting digital transactions and instead pushes them to return to cash-based dealings.

| Inter-Bank Funds Transfers Inter-bank funds transfer is the term used to define transactions where funds are instantly transferred from an account of a bank to an account of another bank. In this case, funds are deducted from one bank’s reserve, the one with the sender’s account, and are added to the reserve of the other bank, the one with the receiver’s account. Moreover, there are intra-bank funds transfers as well where funds are transferred from one account to another, but both the sender’s and receiver’s accounts are in the same bank. This way, the bank’s reserves are neither depleted nor expanded and the only change is which account in the bank holds those funds. Such transfers are exempted from the digital transaction service fee that the SBP has allowed banks to charge. |

IS THE SERVICE CHARGE A CONSUMER PROTECTION POLICY?

The SBP clarified that this should be considered a service charge collected by the banks rather than a government tax. As the SBP explains, the reason behind allowing banks to collect this charge is to help the banks cover their costs for digital funds transfer services. This, as per the SBP, will aid in ensuring a sustainable supply of digital services by fintech and banks without discouraging digital transactions in the economy.

On the one hand, considering the scenario painted by the SBP, we can see this not as a charge imposed on consumers but as a consumer protection policy by setting a maximum limit of charge applicable while allowing banks to decide individually whether they wish to charge the fee or not.

It is essential to note that the transaction fee on IBFTs forms a very small and/or negligible portion of non-interest earnings of the bigger banks, but without collecting this service charge the smaller banks are expected to suffer severely. Subsequently, the main target of SBP’s policy is to cater to the issues these banks might face.

This, though, could result in a possible consumer shift towards those offering free IBFTs, and the smaller banks will continue to suffer, one way or the other, indicating the solution lies elsewhere.

| What are Consumer Protection Policies? Consumer protection rules, regulations and laws are meant to safeguard the rights of buyers of goods and services from any kind of exploitive, deceptive, or fraudulent practices by the sellers of these goods and services. Various state institutions, agencies and statues are employed by the government to enforce these consumer protection policies and keep the power of exploitation shifting towards the seller and thus ensuring in maintaining fair transactions in the market. |

DOES SERVICE CHARGES DISCOURAGE IBFT?

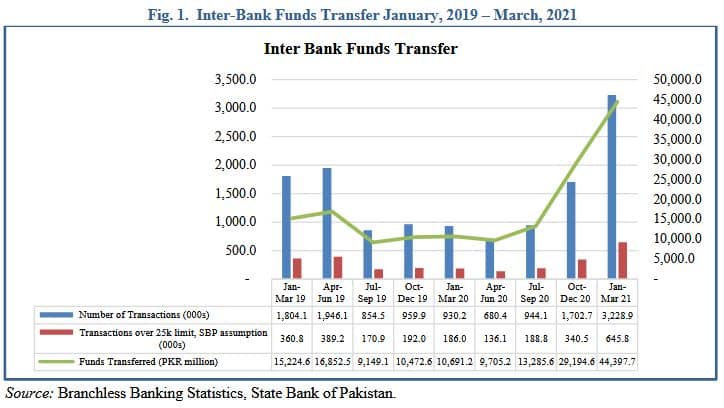

Figure 1 represents the total number of IBFT transactions every quarter over two years from January-March 2019 to January-March 2021. Figure 1 also shows the number of transactions that would have been charged the service fee had this rule been applicable throughout the mentioned period under the 80-20 ratio as defined by the SBP. The graph also displays the total funds transferred in these transactions during the time.

| According to the SBP, around 80 percent of monthly IBFT do not cross the PKR 25,000 limit, therefore, the charge will be applicable on only 20 percent of the transactions. Using this information, we work under the assumption that of the total IBFT transactions in a month, 80 percent of those did not cross the PKR 25,000 limit while the remaining 20 percent are the ones over and above this limit. As we assume this ratio on monthly transactions, the same will hold true for quarterly transactions. We then use data from ‘State Bank of Pakistan’s Branchless Banking Statistics’ to assess the IBFTs and the impact of service charges on them. |

As shown in Figure 1, the IBFT has been on the rise in Pakistan, especially in the post-pandemic period. Even if only 20 percent of transactions cross the PKR 25,000 limit, around 200,000 to 300,000 transactions cross the PKR 25,000 limit every quarter. This means, on average, 100,000 IBFT transactions every month are over and above the PKR 25,000 limit. It is equally important to note that the IBFT became free of charge at the end of the January-March 2020 quarter, while the April–June 2020 quarter was marred by the first wave peak of the COVID-19 pandemic. Since then, as some normalcy was restored and economic activity resumed, the IBFT has shown an unparalleled rise in three quarters in terms of the number of transactions and funds transferred.

In October–December 2020, IBFT transactions were slightly lower but at almost the same level as during the two quarters January–March 2019 and April–June 2019. The funds transferred in October–December 2020, a quarter with no service charges, were almost twice as much as the two quarters in 2019. This shows that not only were the number of transactions on a constant rise during the period no service charges were being collected, but the funds being transferred were much higher as well.

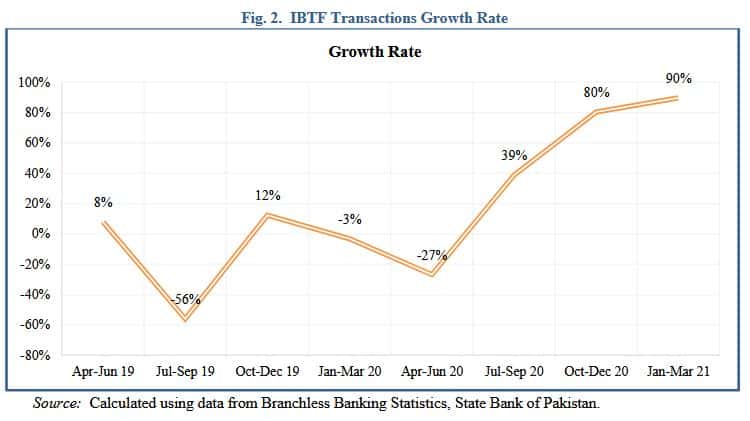

Figure 2. represents the growth rate of Inter-Bank Funds Transfer transactions over this period..

The positive impact of free-of-charge IBFTs is quite evident in Figure 1 and Figure 2. The significant rise in IBFTs following the removal of charges in March 2020 means more transactions were happening through banking channels instead of cash dealings, resulting in a more documented economy and transaction history, which has been the aim of all recent fiscal policies in the country. With the imposition of transaction charges on IBFTs again, this could be reversed as people would be tempted to revert to dealing in cash.

The positive impact of free-of-charge IBFTs is quite evident in Figure 1 and Figure 2. The significant rise in IBFTs following the removal of charges in March 2020 means more transactions were happening through banking channels instead of cash dealings, resulting in a more documented economy and transaction history, which has been the aim of all recent fiscal policies in the country. With the imposition of transaction charges on IBFTs again, this could be reversed as people would be tempted to revert to dealing in cash.

IMPACT OF POLICY CHANGE ON SPECIFIC SECTORS

Above, we have talked about the impact of allowing banks to collect service charges on IBFT on banks, consumers, and the transactions in the economy. This policy will undoubtedly have a direct effect on various economic agents in multiple sectors and industries. In this policy viewpoint, we touch upon a few of those.

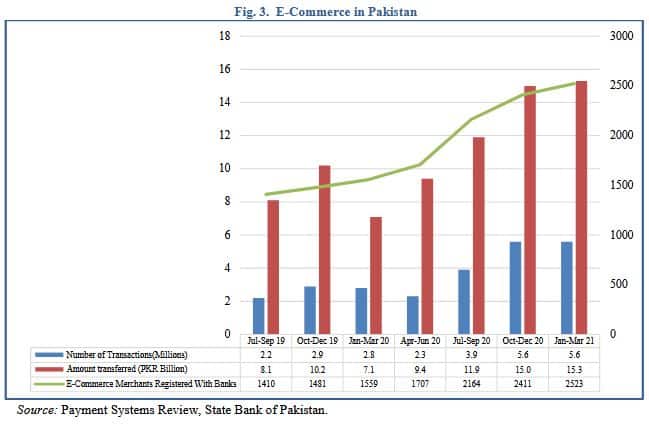

While the COVID-19 pandemic proved to be a health problem, it also caused a nuisance in various social and economic sectors. Realising the need of the changing times, numerous people globally adjusted to new ways of doing business and other activities. Adopting the new normal and favourable policies during the COVID-19 peak to facilitate the public brought many changes in Pakistan’s landscape.

The rise in E-Commerce Merchants Registered with Banks is proof that online business dealings are now on the rise in Pakistan, and facilitating policies will continue to grow. Figure 3 below shows how significantly E-Commerce businesses and transactions have increased ever since the pandemic began and the SBP removed the transaction fee on IBFTs.

Reimposing the transaction fee will prove detrimental to the growth of E-Commerce businesses and their transactions. The increased cost due to transaction fees will either increase the cost of business for E-Commerce merchants or discourage customers regarding the adoption of digital purchasing methods.

This will hurt the E-Commerce merchants in their dealings with their suppliers as well. If the burden remains untransferable to the suppliers, then the cost of business for E-Commerce merchants will increase. However if they manage to transfer the expense to their suppliers, then they (suppliers) will naturally prefer doing business with those dealing in cash rather than with E-Commerce merchants. The transaction fee thus will automatically add distortions in the supply chain, hampering the rise of E-Commerce businesses in Pakistan.

Graduate unemployment is on the rise in Pakistan, and the COVID-19 pandemic made matters worse for the employment aspirant youth in the country. This, though, did present them with an opportunity to look elsewhere. The rise in earnings through freelancing and IT services during the recent past, especially in the post-COVID period, is something that the government has regularly talked big about as the IT exports have now crossed the $200 billion per month mark.

Figure 4 shows the quarterly trend of Computer Services Exports by Pakistan. While the exports were steadily increasing, following the onset of the COVID-19 pandemic, there was a sharp increase in exports. The majority of the financial dealings of freelance and IT services cannot escape the banking channels, which means they will suffer highly due to the transaction fee imposition. Freelancing has been a source of support and income for many skilled professionals who could not secure a decent job while also a source of second income for those pressed by their socio-economic conditions. The distortions by the imposition of the transaction fee will put a barrier in the growth of freelancing activities and the IT services sector of the country, as all stakeholders will be adversely affected.

Moreover, local remittances will be affected severely as well as transferring from a bank account in a commercial bank to mobile wallet accounts also falls under the IBFTs. In most rural areas, commercial bank branches are not as accessible as in cities; therefore, many people use mobile wallet services such as ‘easypaisa, upaisa, jazz cash’ etc. for remittance purposes. Households in rural areas are supported by any family member employed in major urban centres, where salaries are often deposited in commercial banks. Consequently, the compulsion to pay a transaction fee will adversely affect the low-income and lower-middle-class families.

Moreover, local remittances will be affected severely as well as transferring from a bank account in a commercial bank to mobile wallet accounts also falls under the IBFTs. In most rural areas, commercial bank branches are not as accessible as in cities; therefore, many people use mobile wallet services such as ‘easypaisa, upaisa, jazz cash’ etc. for remittance purposes. Households in rural areas are supported by any family member employed in major urban centres, where salaries are often deposited in commercial banks. Consequently, the compulsion to pay a transaction fee will adversely affect the low-income and lower-middle-class families.

WHAT IS THE WAY FORWARD?

As established through evidence-backed analysis of the impact of IBFTs, it is recommended that the transaction fee be immediately waived once again. This will encourage people to adopt digital banking channels and formalise more transactions as it did during the past year. The PIDE Reform Agenda[1] highlights and emphasises the need for easing up regulations to facilitate boosting the size markets, economic activity, and transactions in the economy. This policy recommendation follows the same principles, as also represented by data that removal of transaction fee on IBFT will have a significant impact on increasing IBFT thus documenting and formalising transactions in the economy.

However, if the SBP considers it essential to help banks cover the operational costs, which, as mentioned above, could be necessary for smaller banks, alternative measures to help the banks must be adopted.

- One way is to reduce the corporate tax rate for the banks by a slight amount which will not make a significant difference in overall tax collection but will help banks cover their costs of providing free-of-cost digital funds transfer facilities. The banking sector forms the largest taxpayer unit among the corporate taxpayers, and extending some relief from the fiscal side to help increase financial inclusion in the economy will be a good deal. The overall gains from free-of-cost digital transfers will be higher than the reduction in revenue due to a slight decrease in the corporate tax rate.

- The second alternative could be to reduce the capital gain tax on investment in government securities for the banks. The rate currently lies at 10 percent, and a slight reduction could help cover the banks’ costs without hampering the tax revenues if the government is unwilling to alter the corporate tax rates, which form a much higher revenue stream.

- Besides, the State Bank of Pakistan and the government can reduce either tax rates above conditional to providing free-of-cost digital funds transfer. In other words, the SBP may allow them to charge a service charge on digital funds transfer as per the current guidelines. However, if they decide to provide free-of-cost services, they shall be incentivised by a reduced tax rate on either corporate tax or the capital gains tax on investment in government securities.

- This way, the government and SBP will have protected consumers by putting a maximum limit on service charges and encourage the banks to reduce their tax liability by providing free-of-cost services. In such a way, the banks will have the choice while consumers will be fully aware of government, SBP and banks to facilitate them, thus, being able to make an informed choice regarding which bank services they must opt for.

______________________

[1] https://pide.pk/research/the-pide-reform-agenda-for-accelerated-and-sustained-growth/