Tax expenditures have become an increasingly prominent, widely used policy handle, yet insufficiently scrutinized, instrument of fiscal policy. Commonly defined as deviations from a benchmark tax system and categorized such as exemptions, deductions, tax credits, and preferential rates. These reduce tax liabilities for specified sectors, activities, or groups (Asian Development Bank, 2023[1]; World Bank, 2024[2]). While these measures are often justified as tools for promoting investment, supporting industries, and facilitating economic development, they also represent implicit public spending in the form of forgone revenue (International Monetary Fund, 2019)[3] hence need to be scrutinized on similar levels as of the normal budgetary allocations.

However, unlike direct expenditures, tax expenditures are embedded within tax legislation, schedules, and statutory instruments. Consequently, they often escape the determination of volume, degree of scrutiny, prioritization, and performance evaluation typically applied to budgetary spending. This institutional feature raises a central policy question: whether tax expenditures function as effective instruments for influencing business behavior or primarily operate as mechanisms that enhance profitability only without generating meaningful economic outcomes.

Tax Expenditures Behavioral Impact

From a business development perspective, the government’s employ tax expenditures as incentives to promote private investment, encourage sectoral development, and enhance export competitiveness. In principle, such measures are intended to influence firm behavior by altering relative costs and returns. However, the critical element in effectiveness of these instruments depends critically on their design and conditionality.

A key analytical distinction arises between:

Income-based incentives: reduced tax rates and exemptions, and

Input-based incentives: concessions on raw materials and intermediate goods

Both categories reduce the tax burden, but neither necessarily ensures a change in economic behavior. Income-based incentives tend to increase after-tax profitability without guaranteeing additional investment or productivity gains. Similarly, input-based incentives reduce production costs but do not directly promote value addition, export performance, or technological upgrading.

In the absence of clearly defined performance criteria, allowed budget and sun-set clauses the causal link between tax expenditures and desired economic outcomes remains weak. This limits their effectiveness as instruments of business policy and complicates their evaluation.

Global Evidence and Policy Lessons

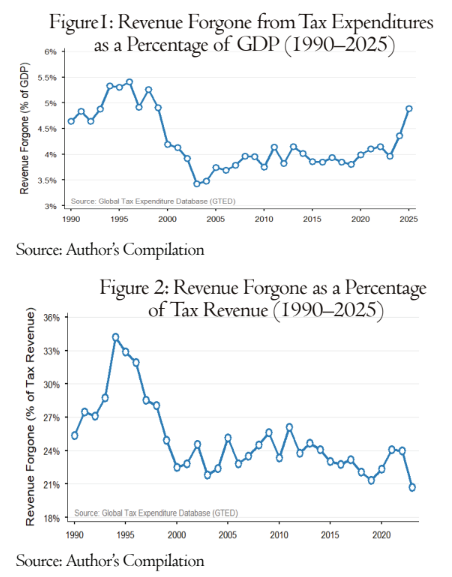

From Figures 1 and 2, based on Global Tax Expenditure Database[4], it can be seen that tax expenditures constitute a significant share of fiscal systems globally, often ranging between 3 and 5 percent of GDP (with increasing trend) and 20-25 percentage of Revenue (decreasing trend). While their magnitude is comparable across countries, their institutional management differs substantially.

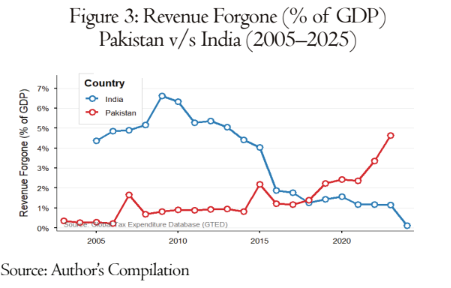

Figure 3 also provides an important comparative perspective for Pakistan in this regard. India’s experience demonstrated that the fiscal cost of tax expenditures can be reduced through policy reform (OECD, 2011)[5], including the rationalization of exemptions and the broadening of the tax base. The observed decline reflects a transition toward a more rule-based and transparent system, supported by periodic review and policy discipline.

In contrast, Pakistan exhibits a persistent upward trend in tax expenditures as a percentage of GDP. This divergence suggests that the issue is not merely the existence of tax incentives but with least impact and the absence of systematic mechanisms for evaluating their relevance, effectiveness, and continuation.

Pakistan’s Case: Structural Imbalance in Fiscal Policy due to Tax Expenditures

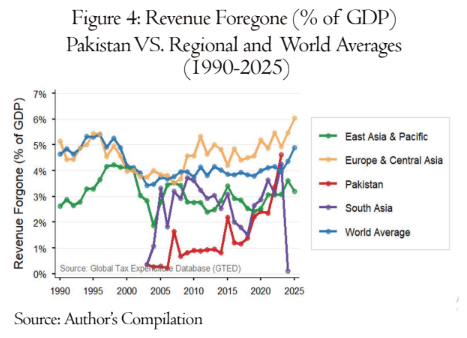

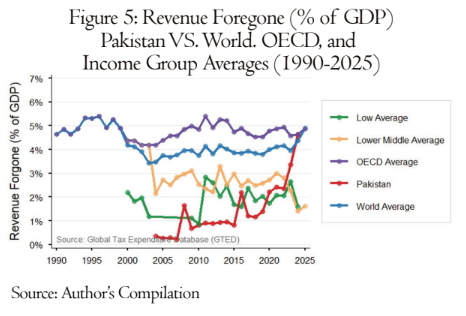

The relationship between tax expenditures and revenue mobilization in Pakistan reveals a notable structural imbalance. Figures 4 and 5 show a steady increase in tax expenditures, approaching 4–5 percent of GDP in recent years. At the same time, Figure 6 indicates that the tax-to-GDP ratio remains persistently low, fluctuating around 10 percent.

This coexistence suggests that tax expenditures have not contributed to a commensurate expansion of the tax base. Instead, they appear to reduce effective tax rates without generating sufficient additional economic activity to offset revenue losses. The result is a weakening of fiscal capacity and a continued reliance on a narrow tax base.

[1] https://www.adb.org/sites/default/files/publication/932086/tax-expenditure-estimation-tool-kit.pdf

[2] https://documents1.worldbank.org/curated/en/099062724151636908/pdf/P174543148ba880bb188fd1ce06f588a6aa.pdf

[3] Tax expenditures—How to measure and evaluate them. International Monetary Fund.

[4] https://gted.taxexpenditures.org/

[5] https://www.oecd.org/content/dam/oecd/en/publications/reports/2011/06/oecd-economic-surveys-india-2011_g1g1166e/eco_surveys-ind-2011-en.pdf