1. INACCURACY OF REVENUE FORECAST

The effective management of resources, physical, financial or natural, is the key for success and prosperous life of an individual as well as nations of the world. Governments prepare plans so as to materialise their short and long term goals needed for the peace and prosperity of the country. The plans are implemented through the effective use of human, natural and financial resources available to the country. The expenditures, either for development purposes or for current need, depend upon the resource envelope of the country. The resource envelop of a country consists of two major components namely internal resources and external resources. The availability of total internal resources depends upon tax and non-tax measures.

For any government of a country, accuracy of tax revenue forecasting is important for materialising its projected programs. Otherwise the degree of deviation from accurate forecasting would eventually cause government to lose its esteem among the public. In Pakistan, historically there has been a shortfall in actual revenue receipts against the projected values. The shortfall in revenue receipts causes cuts mainly in capital /development expenditure which lowers the pace of future growth of the country

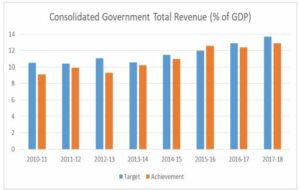

The budget preparation is annual feature and is being practiced by each country of the world. The first and the most important step towards budget preparation is the determination of resource envelop available to the country. Serious efforts are made to determine the appropriate level of revenue receipts which constitute major portion of internal resources. Apparently, the annual budget in Pakistan is also prepared on the principles being followed by most of the countries of the world. The targets for government receipts are determined and the expenditures are made accordingly. However, these targets are hardly achieved in any fiscal year. The graph contains the consolidated government targets for total revenue receipts as a percentage of GDP for the last Eight years. The targets lay down for revenue receipts did not materialised for most of the period. If we do the same for absolute targets, then this situation further exacerbates. Missing the revenue target clearly indicates that either the targets are based on inaccurate forecasts or the tax collection machinery is inefficient. The accuracy of revenue receipts of Federal Government has become important, especially after 18th constitutional amendment, because any shortfall in federal revenue receipts would has two important effects: one it will jeopardise federal government’s development plan and secondly the provincial governments would have lesser resources at their disposal because more than 80 percent of provincial resources depend upon the transfers made by the Federal Government.

In their study Qasim and Khalid (2016) have noted that as per Accounting Policies and Procedures Manual, Government of Pakistan, the revenue forecasting is defined as:

“Forecasts of revenue are to be prepared on a cash basis that is, based on what can reasonably be expected to be paid and collected in the financial year. This will be calculated from prior year collection figures, adjusted for changes in revenue collection policy. The forecasts will be provided in gross amounts (e.g. revenues will not be shown net of any related costs). This is also consistent with the related accounting policy for the recognition of revenues”.

The above stated revenue forecasting procedure is very simple and it is not based on any forecasting model/procedure/technique which usually takes into account all economic agents that are likely to play key role in the determination of revenue for the coming year. The reason for over or under estimation is due to non-adoption of proper model/procedure to determine the revenue forecasts. The study further notes that FBR (Federal Board of Revenue) is the major tax collecting authority of the country and is collecting about 90 percent of tax revenue. It has its own procedure/method for setting the revenue targets for the coming year (or next year). The procedure/method adopted by FBR to set the next year revenue target is not available in the documented form. However, the discussions with the officials of FBR reveal the following combination of procedure/method adopted by FBR to set the revenue targets for the coming year