The Cost of Disinflation: The Sacrifice Ratio?

NADEEM UL HAQUE, Vice Chancellor, PIDE

ABDUL JALIL, Professor of Economics, PIDE

PRICE STABILITY IS IMPORTANT

Price stability is an imperative in economics. Independent central banks have therefore been encouraged by the IMF in all countries with a clear mandate to achieve a low inflation target. It is well accepted that long run sustained growth requires a stable low inflation environment (Barro, 1996 and Feldstein, 1996). Curbing inflationary pressures is not costless. The tradeoff between growth and inflation is well known ever since the famous Phillips curve. The recessionary impact of IMF programs at least in their early stages is also well known (Haque and Khan, 1998). Studies also show that disinflation is associated with possibilities of a recession in United States of America (Romer and Romer, 1989) and Japan (Fernandez, 1992) among other countries. Yet in most economies there is no clear growth target, nor an agency for attaining it. One approach to measuring the tradeoff between growth and inflation is the Sacrifice Ratio (SR) which is defined by the ratio of accumulated loss in real GDP during a particular episode of disinflation to the overall fall in inflation during this particular episode (See Box 1).

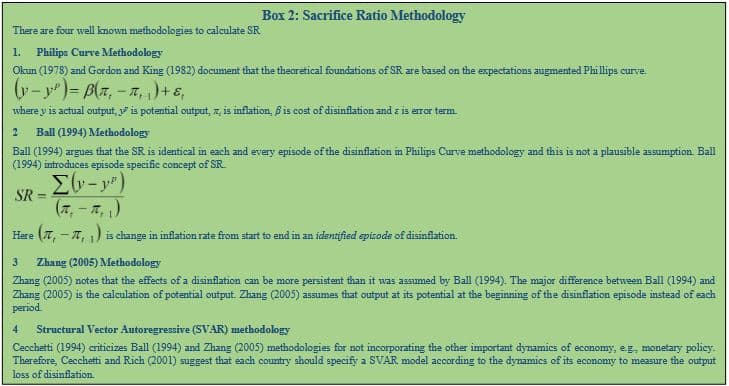

| Box 1: Definition of Sacrifice Ratio (SR) It is well accepted that disinflation produces output losses. The quantification of these losses due to disinflation is termed as SR. More clearly, SR is used to gauge the cost of disinflation in terms of accumulated loss in real gross domestic product (GDP) due to monetary policy. |

Several methodologies are suggested by the existing literature for the calculation of SR (see Box 2)

In this Knowledge Brief, we will:

- Review estimated SR in various

- Develop estimates of the SR for Pakistan based on Ball (1994).

SR AROUND THE WORLD

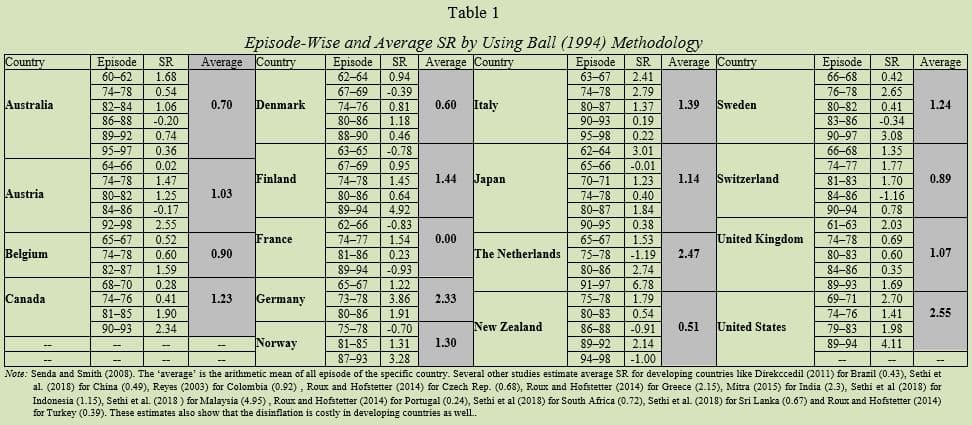

Estimates of SR from many emerging markets are presented in Table 1.[1] In understanding these estimates the following considerations should be borne in mind.

- Estimates may vary with

- The SR may vary with the level of inflation and its

We will also examine the determinants of the SR such as speed of disinflation, length of episode from inflation to disinflation, credibility and independence of monetary authority to pursue disinflation policy, initial level of inflation in later studies (see Box 3).[2] This particular study discusses the size of SR.

| Box 3: Determinants of Sacrifice Ratio The literature on the loss of output due to disinflation suggests that the size of SR depends on several factors. These include speed of disinflation, trade openness, central bank independence, inflation targeting, governance and political regime. It appears that SR ratio will be lower in • a quick disinflation episode (Ball, 1994), • a stable political regime (Caporale, 2011), and • more open economies (Temple, 2002 and Bowldler, 2009), • the presence of good governance (Caporale and Caporale, 2008). The role of central bank independence and inflation targeting in determining the size of SR is less clear. • Brumm and Krashevski (2003) and Diana and Sidiropoulos (2004) and Daniels et al. (2005) suggest that SR will be lower where the central banks are more independent whereas Fischer (1996), Jordan (1997), and Down (2004) find evidence to the contrary. • Goncalves and Carvalho (2008, 2009) find lower SR in the countries which are pursuing inflation targeting while Brito (2010) notes that the sample of Goncalves and Carvalho (2008, 2009) is based on only low inflationary OECD countries. If the sample is expanded, then the inflation targeting does not matter a lot for a lower SR. |

____________________________

[1]We present the findings which are based on Ball (1994) methodology to allow us to capture a larger comparable sample of countries.

[2]As mentioned earlier, we only present the size of SR. This note will follow Senda and Smith (2008) by taking the average SR for every country.

Table 1 reports 77 episodes of disinflation of 17 different countries. It is observed that the ratio is positive in 64 of 77 cases. This suggests that disinflation is usually costly.[3] More clearly, on average there is 0.7 percent accumulated loss in real GDP during a particular episode of disinflation to the overall 1 percent fall in inflation during in the case of Australia. It is also evident from the table 1 that there is a huge variation in the SR of different countries.[4] One can infer that the cost of disinflation may vary from country to country. However, it is also important to note that the direct comparison among countries is not sensible due to several reasons (see Box 4).

SACRIFICE RATIO IN PAKISTAN

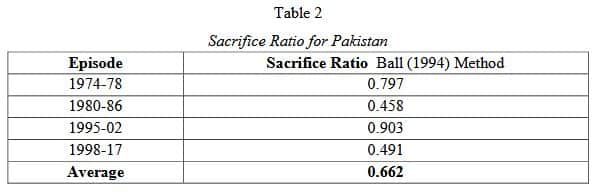

We calculate SR by well-known Ball (1994) methodology using HP filter method for potential real output and three years centered moving average inflate rate from period of 1973 to 2018. We find four episodes of inflation in the case of Pakistan (see Table 2). It is evident that from the table that SR is different for all four episodes. It ranges from 0.458 to 0.903 and the average of all four episodes is 0.662. It implies that on average 0.662 percent of the real GDP will be forgone for the permanent reduction of one percent of inflation. However, these findings are highly sensitive to measuring of SR and real output loss.

| Box 4: Interpretation of Sacrifice Ratio As mentioned earlier, SR is a ratio of accumulated loss in real GDP during a particular episode of disinflation to the overall fall in inflation during this particular episode. By definition, there are two major parts of the ratio. First, the loss in real output (relative to trend) in the numerator and the slowing of the consumer price index in the denominator. Therefore, the magnitude of SR can be determined by two different elements. • First, the accumulation of output loss (numerator) and • second, the slowing of consumer price index (denominator). It simply implies that the magnitude of SR will be different with a different denominator even if the nominator (loss of output) is same for each country and vice versa. Suppose, a country has a smaller difference between start and end of the disinflation episode of a country as compared to any other country, then the SR of this country will be higher even with the same loss of output. This means that the SR of two different countries are not directly comparable. We must take care of a number of issues. First, the numerator. The numerator is the accumulated difference between potential output and actual output. It is well accepted in the literature that calculation of potential output is sensitive to the methodology. Therefore, the SR may differ due to the change in the methodology of calculating the potential GDP. Second, the denominator. There are several concerns in the denominator like the definition of the episode of disinflation, length of the disinflation episode, peak and trough of inflation in that particular episode and speed of disinflation. Therefore, we must have same elements/assumptions both in numerator and denominator to calculate a comparable SR for different countries. |

__________________________

__________________________

[3] The negative SR may imply that the disinflation may have a positive impact on economic growth.

[4] Cecchetti and Rich (2001) is a good read in this context. Their estimates range from about 1 to nearly 10, suggesting that somewhere between 1% and 10% of one year’s GDP must be sacrificed for inflation to fall one percentage point only in the case of United States based on the different specifications of SVAR.

CONCLUDING REMARKS

This note serves two purposes. First, it reviews the literature on the estimated size of SR for several countries. Second, it estimates SR for Pakistan, based on the most prominent methodology of Ball (1994). We estimate that the average SR is 0.667 in the case of Pakistan which implies that the disinflation is costly in the case of Pakistan as well. Disinflation will, therefore, be costly as expected.

It must be noted that this estimate is not an argument against disinflation. This estimate merely informs policy-makers of what to expect for growth and employment in an adjustment program. With an employment elasticity of 0.1, we can expect that employment will be reduced by 0.06% (Zulfiqar and Choudhry, 2008). Policy must seek structural reform in a disinflation episode (adjustment program) to generate some growth momentum in the economy, if costs of disinflation are to be mitigated.

REFERENCE

Ball, L. (1994) What determines the sacrifice ratio? NBER Chapters. In Monetary Policy, pages 155-193, National Bureau of Economic Research, Inc. The University of Chicago Press.

Barro, R. (1996) Inflation and growth. Federal Reserve Bank of St. Louise Review. May-June.

Bowdler, C. (2009) Openness, exchange rate regimes and the Phillips curve. Journal of International Money and Finance 28, 148–160.

Brito, R. D. (2010) Inflation targeting does not matter: Another look at OECD sacrifice ratios. Journal of Money, Credit and Banking, 42:8, 1679–1688.

Brumm, H. & Krashevski, R. (2003) The sacrifice ratio and central bank independence revisited. Open Economies Review, 14, 157–168.

Caporale, B. & Caporale, T. (2008) Political regimes and the cost of disinflation. Journal of Money, Credit and Banking, 40, 1541–1554.

Caporale, T. (2011) Government ideology, democracy and the sacrifice ratio: Evidence from Latin American and Caribbean disinflations. The Open Economics Journal 4, 39–43.

Cecchetti (1994) Comments in Ball, L. (1994). What determines the sacrifice ratio? NBER Chapters, In: Monetary Policy, pages 155-193, National Bureau of Economic Research, Inc. The University of Chicago Press.

Cecchetti, S. G. & Rich, R. W. (2001) Structural estimates of the US sacrifice ratio. Journal of Business and Economic Statistics, 19, 416–427.

Diana, G. & Sidiropoulos, M. (2004) Central bank independence, speed of disinflation and the sacrifice ratio. Open Economies Review, 15, 385–402.

Daniels, J., Nourzad, F. & Van Hoose, D. (2005) Openness, central bank independence, and the sacrifice ratio. Journal of Money, Credit and Banking, 37, 371–379.

Direkccedil, T. B. (2011) Determination of the sacrifice rate in Turkey, Brazil and Italy: A comparison among countries. Journal of Development and Agricultural Economics, 3, 335–342.

Down, I. (2004) Central bank independence, disinflations, and the sacrifice ratio. Comparative Political Studies, 37, 399–434.

Feldstein, M. (1996) The costs and benefits of going from low inflation to price stability. (NBER Working Paper No. 5281).

Fernandez, D. (1992) Bank lending and the monetary policy transmission mechanism: Evidence from Japan. Princeton, New Jersey: Princeton University.

Fischer, A. (1996) Central bank independence and sacrifice ratios. Open Economies Reviews, 7, 5–18.

Goncalves, C. & Carvalho, A. (2009) Inflation targeting matters: Evidence from OECD economies’ sacrifice ratios. Journal of Money, Credit and Banking, 41, 233–243.

Gonçalves, C. E. S. & Carvalho, A. (2008) Inflation targeting and the sacrifice ratio. Revista Brasileira de Economia, 62:2, 177–188.

Gordon, R. & King, S. R. (1982) The output cost of disinflation in traditional and vector autoregressive models. Brookings Papers on Economic Activity, Economic Studies Program. The Brookings Institution, 13, 205–244.

Haque, N. U. & Khan, M. S. (1998) Do IMF-supported programs work? A survey of the cross-country empirical evidence (December 1998). (IMF Working Paper 98/169).

Jordan, T. (1997) Disinflation costs, accelerating inflation gains, and central bank independence. Weltwirtschaftliches Arch, 133, 1–21.

Mitra, P., D. Biswas, & Sanyal, A. (2015) Estimating sacrifice ratio for Indian economy: A time varying perspective. (RBI Working Paper Series No. 01).

Okun, A. M. (1978) Efficient disinflationary policies. The American Economic Review 68:2, 348–352.

Reyes, J. D. (2003) The cost of disinflation in Colombia:—A sacrifice ratio approach. Departamento Nacional de Planeación.

Romer, C. & Romer, D. (1989) Does monetary policy matter? A new test. In the Spirit of Friedman and Schwartz. (NBER Working Paper No. 2966).

Roux, N. D. & Hofstetter, A. (2014) Sacrifice ratios and inflation targeting: The role of credibility. International Finance, 17:3, 381–401.

Senda, T. & Smith, J. K. (2008) Inflation history and the sacrifice ratio: Episode‐specific evidence. Contemporary Economic Policy, 26:3, 409–419.

Sethi, D., Wong, W. K. & Acharya, D. (2018) Can a disinflationary policy have a differential impact on sectoral output? A look at sacrifice ratios in OECD and non-OECD countries, margin. The Journal of Applied Economic Research, 12:2, 138–170.

Temple, J. (2002) Openness, inflation, and the Phillips curve: A puzzle. Journal of Money, Credit and Banking, 34, 450–468.

Zhang, L. H. (2005) Sacrifice ratios with long‐lived effects. International Finance, 8:2, 231–262.

Zulfiqar, K. & Chaudhary, M. Aslam (2008) Output growth and employment generation in Pakistan. Forman Journal of Economic Studies, 4, 41–57.