The Pension Bomb and Possible Solutions

OVERVIEW

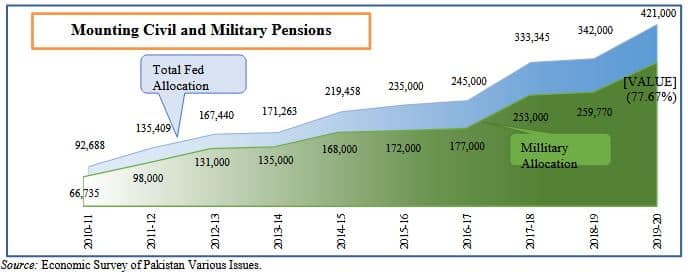

Public sector employment remains an attraction for two important reasons: job security and a guaranteed pension (Dixit, 2002).[1] Unlike other countries Pakistan has not reformed its public sector pension system and maintains a pay-as-u–go defined benefits type pension system which has resulted in build up of unfunded liability for the government. Pakistan practices a legacy pension system where pensioners are paid directly from the revenues as part of the current expenditures. This practice is inherently unsustainable as pension expenditure growing at around 25%, cannot be provided from an economy growing at a significantly lower rate. The pension burden is therefore bound to grow, doubling every four-years. In the fiscal year 2018-19 federal superannuation and pension expenditures were almost 78% of the value for PSDP expenditures and it increased in FY 2019-20 to 87%(463,419 million Rupees and 533,220 million Rupees respectively). The share of pensions as a percentage of current expenditures is also increasing overtime (for FY 2019-20 it stood around 7.6%).

It is estimated by 2050, pensions will account for 56% of current expenditure. The government will not have the funds for pension expenditure after 8-10 years.[2] The pension outlay in Punjab Budget equals 95% of the revenue of the province. Railway pensions stand at 70% of its annual revenue.

In 2003, Pension Review Working Group had recommended the Funded Pension Scheme with Defined Benefit part to be funded by the state and Defined Contributions by the employees. The government however did not approve. The fact remains; Pakistan is already in deep crisis will little time left for the transformation of the pensions system.

| Box 1: Pension Driven Fiscal Burden · Pension expenditures growth: 25%. · Pension expenditures constitutes approximately 80% of the value for PSDP expenditures. · Projected pension values suggest that it will rise to 56% of current expenditure in 2050. · Ageing population, increased medical expenditures, and forced inflation indexing will continue to put pressure on the pension bill. |

FEDERAL PENSIONS—MILITARY AND CIVILIAN GOVERNMENT EMPLOYEES

It is worth noting; the share of military pensions stands at 75.67% of the Federal Pension Budget 2019-20 though the number of the Federal and Military retirees stands at around 1.2mn each. Three times the bigger expenditure of the military is on account of the early retirement of soldiers resulting in pension durations twice the federal employees who retire at 60. However Civil pension itself is rendering into an unsustainable territory of public financial management. In FY 2019, pension rose to 40 percent of federal public expenditures on salary for civil servants due to longevity, increasing health costs and liberal reforms overtime. Ageing population[3], increased medical expenditures, and forced inflation indexing will all continue to put pressure on the pension bill.

_____________________________

[1]Dixit, Avinash (2002) Incentives and organisations in the public sector: An interpretative review. Journal of Human Resources, 37(4), Fall, 696–727.

[2]Addressing the Pension Liability by Hasaan Khawar, April 18, 2018 https://tribune.com.pk/story/1681449/addressing-pension-liability

[3] According to World Bank Pakistan had a life expectancy at Birth of 45.3 in 1960, which have improved to 67 years in 2017. Although it ranked 186th in 249 entries of the data in 2017 which was 166th in 1960. Which reflects that relatively speaking its not that impressive rather it has worsened.

NATIONAL COMMISSION FOR GOVERNMENT REFORMS (NCGR) RECOMMENDATIONS: MOVE TO A DEFINED CONTRIBUTION (DC) SYSTEM

The existing system has multiple payout systems to pensioners, is actuarially unfair, biased upward and above all its financing is becoming expensive since it competes for tax payers money. The system is a DB which requires flexibility in terms of contribution, vesting period and other parameters in case of any reform or shock such as increase in life expectancy, cost elements, inflation indexing etc. But since here its a Pay-As-You Go System these options are not considered. This system is unsustainable and world over considered as a least preferred one.

This is not the first incidence earlier NCGR in its report (Vol-I, 2008) recommended to reform pensions and the recommendation was presented as a guiding principle. It stated that: “The Pension System should be revised from defined Benefits, to defined contribution and should be funded.”

NCGR further recommended to only index the pensions for maintaining the purchasing power of pensioners, which lately is being overprovided. The commission proposed a complete road map which required “Complete Analysis of Pension Options and made recommendations guided by the advice given to the government by the Pay and Pension Committee of the Finance Division, Establishment Division and an Actuarial firm/consultant”. This recommendation could not mature so far.

PENSION FUND PRACTICES

In the case of armed services all other countries facilitate soldiers for their second careers. This, on one hand, increases the contributions towards the pension fund, and the other hand delays reimbursement of retirement benefits. It results in significant long-term savings at the national level that are mostly invested in the assets which fuel economic growth.

For Civil services having a DB system which is unfunded creates barriers for entry and exit into the civil services. Turnovers are not possible because of the unrealised pension benefits. If this system is converted into a DC system then employees would have more leverage for switching across governments/autonomous bodies/ recruitment types and private sector as well. This would help attract qualified and talented individuals in service in various stages of service.

However an actuarial analysis has to be done for identifying the possible benefits which these funds can offer. World over these pension funds are operated by trusts, private funds managers and even governments themselves. But these funds play a pivotal role in providing for the financing requirements of the economy as well. So this system would also unleash the growth along with making this sustainable for the government. The role of Pension Funds in the economic growth can be assessed from the fact that around 76% of assets in the US Stock Exchange are owned by the Pension Funds.[5]

Pension Funds will be required management under a strict regulatory regime by a highly competent team of fund operatives and an investment board. Pakistani record in pension funds like EOBI and Volunteer Pension Scheme is well below par.

CASE STUDY OF FEDERAL CIVIL PENSIONS

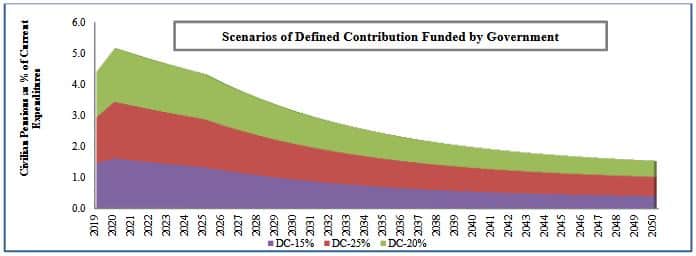

Below we have done projections for a DC system on financing side based on the following assumptions:

- Existing Pensioner would get the same pensions as they are receiving now. Overall volume is freezed, exits from the system would allow inflation indexing for remaining. Using the budget estimates of Civil Federal Pensions for 2019-20 these are projected to remain constant for next five years and then start to decline @ 5% per annum due to reduction in exiting pensioners.

- For those in government service assuming emoluments reckonable for pension to be current pay bill along with 30% of current allowances. Three scenarios of defined contribution funded by government of 25%, 20% and 15% are developed. Final outlay of DC and ongoing existing pension expenditure as a percentage of current expenditures is plotted.

- Current Expenditures are assumed to increase by 5% per annum.

This basic exercise identifies that initially total pension outlays increase from 1.5% of the total current expenditures to around 1.83%, 1.72% and 1.61% for the three scenarios respectively in the 2020-21 that is the first year of reform. This initial rise tapers down to starting level of 1.5% in the 6th, 5th and 3rd year respectively for the three scenarios and then continuously decline and converge around 0.50% in thirty years’ time period. Thus making pension payouts to be sustainable in the longrun.

This basic exercise identifies that initially total pension outlays increase from 1.5% of the total current expenditures to around 1.83%, 1.72% and 1.61% for the three scenarios respectively in the 2020-21 that is the first year of reform. This initial rise tapers down to starting level of 1.5% in the 6th, 5th and 3rd year respectively for the three scenarios and then continuously decline and converge around 0.50% in thirty years’ time period. Thus making pension payouts to be sustainable in the longrun.

____________________________

[4]Comparing pension schemes for civil servants across comparable regional countries, we show that there are more than one method being practiced. In some countries pensions are tailor made for different professions and in some it’s a universal pension scheme exists irrespective of being a civil servant or otherwise.

[5]Research Journal of Finance and Accounting www.iiste.org ISSN 2222-1697 (Paper) ISSN 2222-2847 (Online)Vol.7, No.16, 2016.

THE WAY FORWARD

Pension Funds usually become operative after eight years once sufficient funds have accumulated and investments have started generating revenues. It is therefore of critical importance that pensions are transformed into Contributory Funded Pension System to allow time for these funds to become operational before the prevailing system runs out of the stream.

The following policy measures will be required for moving towards the Defined Contribution System of Pensions.

Legislation should be enacted for;

- Establishing the Central Pension Development and Regulatory Authority along with an Investment Board.

- Special provisions/exemptions for investments for such projects as; Housing Scheme through the Supplementary Pension Fund.

- Investment in listed and private equities and Venture capital.

On the other hand a Pension Review Working Group (PRWG) need be formed to formulate policies, structural framework, rules, and procedures;

- The PRWG should comprise the following;

- Officer with Corporate Exposure.

- Reps from Existing Armed Services, Federal Services, and Pensioners.

- Tech Team: Fin and Accounts, Banking, Insurance, Asset Management, Actuarial, Risk Assessment, Corporate Law.

- Consultancy from Pension Fund Managers, Actuarials and Corporate managers if needed.

OPTIONS

We have two broad options.

- Centralised Pension Funds at the Federal and Provincial levels for both; Defined Benefits (Pensions) and Defined Contributions (Retirement Benefits).

- Combination of Centralised Defined Benefits for Pensions but Decentralised Supplementary Fund for the Defined Contributions. An option of the Supplementary Fund for the Military Pension Fund for Defined Contributions, like the Turkish Pension Fund (Oyak), can also be considered.

However an actuarial analysis has to be done for identifying the possible benefits which these funds can offer.

MoF should urgently initiate Actuarial Study and identify the major issues with government pension schemes, EOBI, and VPS (Voluntary Pension System). It should be aimed at broadening participation of the general public in Pension Funds as seen in western countries.