Abedullah and Abida Naurin[1]

Background of the study

The agriculture sector contributes 19.2 percent to GDP and provides the raw material for textile and other agro-based industries. The textile industry accounts for 60 percent of the ‘country’s export. Agriculture employed roughly 38.5 percent of the workforce in 2020-21, while more than 65-70 percent of the people relied on it for their living. The target amount of formal credit was fixed at Rs. 1,500 billion for 2020-21 but only 63.6 percent was disbursed during the fiscal year (GOP, 2020-21).

In Pakistan, the informal credit market is strong to cater to the demand of small farmers through a network of financiers known as “arthis”. To better understand the role of the arthi in the agricultural supply chain, this article attempts to examine the arthi system by mapping the network and linkages, understanding its operations and financing mechanisms such as interest rates, costs, and risk management techniques. This will help to understand why formal institutions have failed to replace the role of arthi in the agricultural supply chain. It may also help financial institutions to improve their economic model to minimize credit risk so that they can penetrate into the farming credit market more efficiently, to capture a significant share.

Who is arthi?

Arthi is a commission agent who facilitates buying or selling agricultural produce, including livestock and collects payment thereof, if required, from the buyer and pays it to the seller. Arthi also receives a commission or a fixed percentage of the transaction value by way of remuneration. Usually, arthies operate in grains, fruits, and vegetable markets where different players in the supply chain of each food commodity interact.

A brief investigation was conducted with 20 arthis from different Mandis of Punjab, Pakistan. It is observed that five of the twenty arthies were Kacha (unregistered), twelve were Pakka arthi (Registered). Pacha arthies provide finance in two ways to the farmers. Some provide credit in terms of cash and some others support farmers in terms of supplying inputs. It is also revealed that registered arthies have business experience ranging between 10 to 30 years.

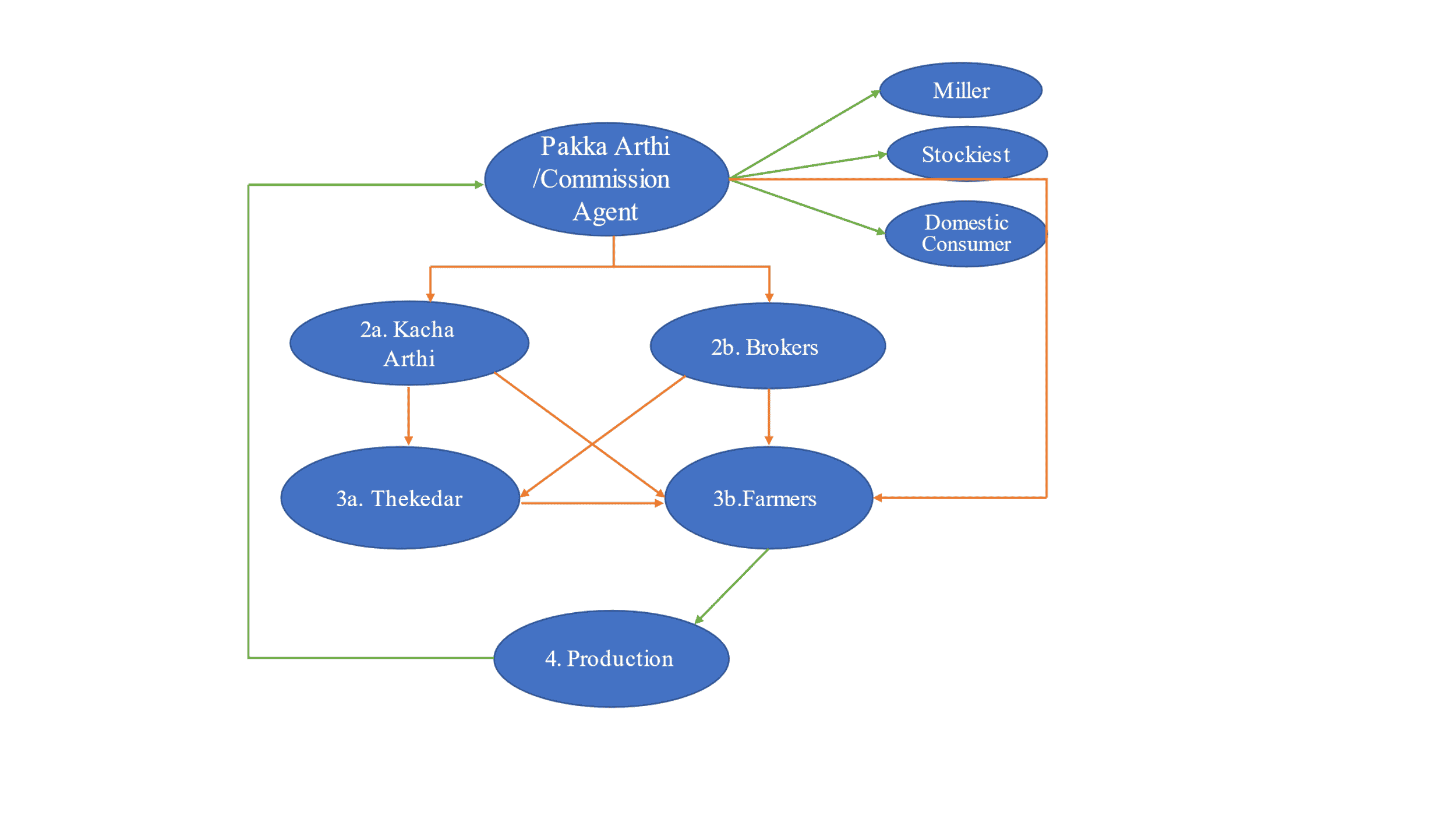

Figure 1 depicts the agricultural supply chain of the grain market in Pakistan[2]. Our survey reveals that pacha arthi rarely deals directly with the farmer rather he approaches the farmer through kacha arthi and broker in the grain market.

______________________________

[1] Abedullah ([email protected]) and Abida Naurin ([email protected]) are respectively Chief of Research and Research Associate at Pakistan Institute of Development of Economics (PIDE), Islamabad.

[2] Red arrow lines show the channels of credit flow from arthi/commission agent to the farmer. Green arrows show the flow of production from farmer to arthi both in figure 1 and figure 2.

The kacha arthi and broker charge a commission from the farmer on the lending amount and acquire the crop title to assure that the output will be sold to the prescribed arthi. Kacha arthi and broker serve as a middleman between the pukka arthi and the farmer. Sometimes this supply chain of informal credit further expands where kacha arthi and broker involve thekedar for the delivery of credit to the farmer. The additional involvement of thekedar increases the cost to the farmer. It only happens when the small farmer has no direct excess to kacha arthi or broker.

Figure 1: The agriculture supply chain in ‘Pakistan’s Grain Market.

Figure 1: The agriculture supply chain in ‘Pakistan’s Grain Market.

The Pakka Arthi is a crop buyer and takes possession of the produce after striking a bargain with the farmer. According to this food supply chain, pakka arthi received production and sold it to three different stakeholders, i.e. Miller, Stockiest, and domestic consumer. Thus, kacha arthi and brokers are playing a major role in lending informal credit to the farmer and bringing the produce from the farmer to the pacha arthi.

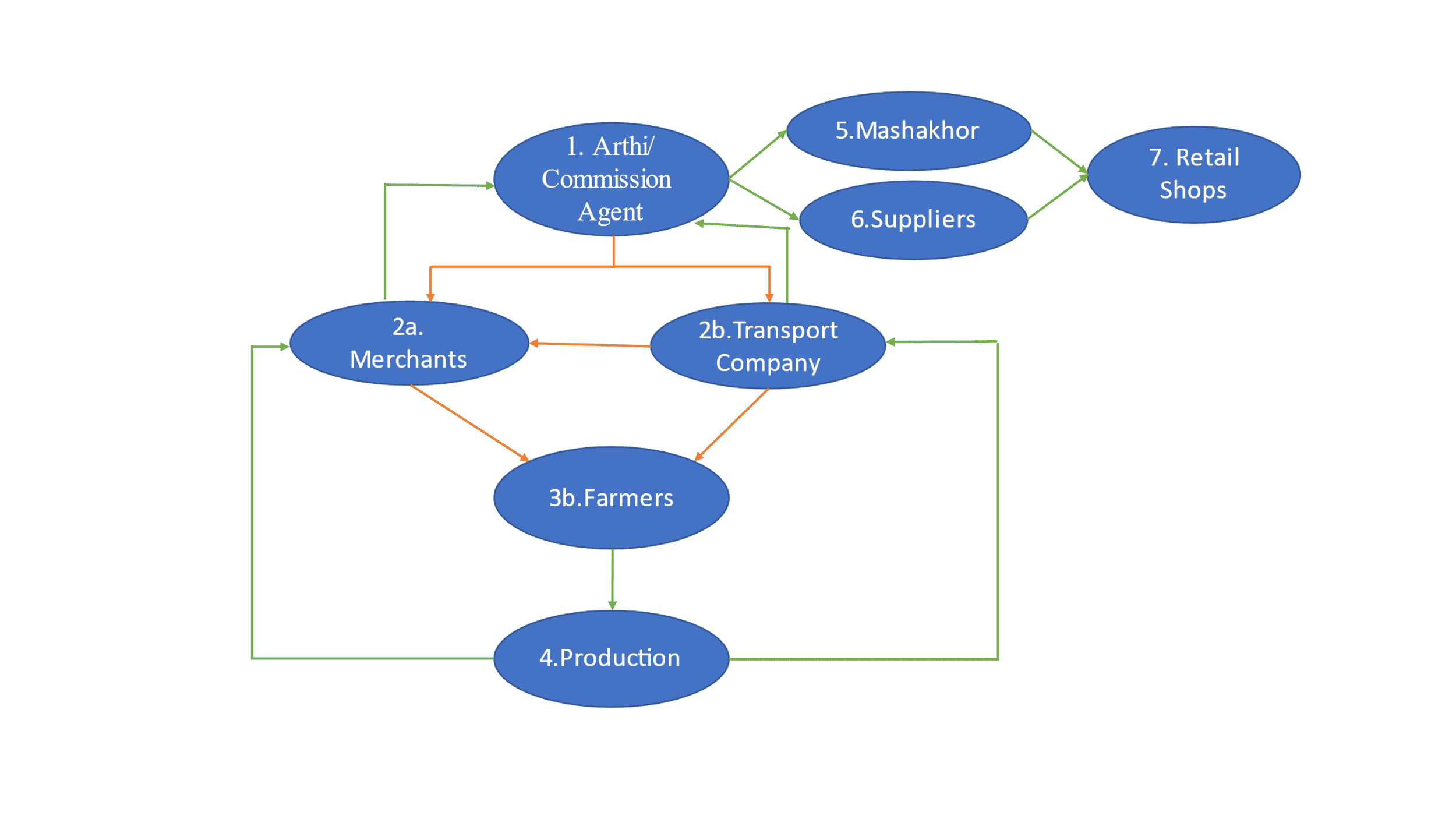

Based on the survey, the role of arthi in fruits and vegetable markets has been elaborated in Figure 2. Arthi/commission agent lends cash to merchants and transport companies and rarely deals with the farmer directly. Merchant either give this amount directly to the farmer as a loan with the binding condition that farmers will sell the output back to him or use this amount to purchase the standing crops from the farmer. However, transport companies take the loan from arthi and give it to the farmer with the binding condition that the output will be delivered to the prescribed arthi by using the transport of the lending companies.

Both merchants and transport companies are bound to sell or bring the product to the Arthi/commission agent who provided the credit. The arthi disbursed it to suppliers, Mashakhor, and retail shops (Figure 2).

Figure 2: The agriculture supply chain in the local fruit/vegetable market.

The role of arthi and the services offered

There are two primary sources of agricultural credit: informal and formal. Informal sources usually include commission agents (also called arthies), input suppliers, village shopkeepers, friends, and relatives. Among these, arthies play the most dominant role and have a significant share in informal credit disbursement.

Our survey reveals that registered arthies have long-term relationships with many farmers. Many admitted that their relationship with farmers had entered the second generation. In some cases, both arthies and farmers invite each other into family gatherings and marriages, indicating that the relationship extends beyond professional to personal lives.

Our discussions with farmers and arthies lead us to conclude that services offered by arthies are not uniform but instead depend on the type of market, its structure, and farmer’s demand. Our investigation of food supply chains reveals that arthi provides two significant services to the farmer. First, he gives cash/inputs on credit at the time of sowing of a particular crop, and second, he acts as the sale agent for the farmer to dispose of his produce.

The poor financial situation of the farmer, long distances from organized markets, and lack of understanding of post-harvest crop management practices are among many factors that play a vital role in ‘farmers’ decision-making process whether to sell the produce at the farm gate or bring it to the Mandi to sell it through the arthi. Selling at the farm gate is preferred by many farmers due to the shortage of labor, high cost of transportation, and high commission expenses. All products that enter the Mandi are immediately auctioned to avoid the risk of price fluctuation, and payments are made the same day to the farmer.

Arthi provides credit or inputs to meet the liquidity gap that farmers face. The timely provision of credit allows farmers to purchase necessary inputs and machinery for farm operations (Saboor et al., 2009). Agricultural credit is considered one of the strategic resources of crops and plays a vital role in improving agricultural productivity. This implies that arthi indirectly contributes to improving farm productivity. Higher productivity raises the standard of living among rural communities. Hence, arthi plays a significant role in the process of rural development.

But the interest rates charged by the arthi show that he makes money by lending to small and medium farmers. The literature reveals that operational cost is less than 2.5 percent of the total lending volume and interest rates range between 62 to 80 percent (Haq et al.; 2013). This implies a significant profit margin exists for the arthi, 5 to 7 percent higher than the formal lending sources. In addition to earning from lending operations, he makes 2 percent to 4 percent commission depending on crop type and terms and conditions with the client (Haq et al.; 2013). But despite the high interest charged by the arthi, it is essential to investigate the reasons that force farmers to secure credit from non-formal over formal resources.

Why do farmers prefer informal over formal credit sources?

Formal credit sources (Government and private banks) have low-interest rates, but excessive procedural requirements delay credit release. Delays in supplying inputs to crops make credit less productive and increase ‘farmers’ risk.

Moreover, the demand for collateral by formal credit institutions is difficult to fulfill because of an inefficient system of land transfers in Pakistan. Due to problems in the inheritance process, a large part of agricultural land is still in the name of forefathers or grandparents and thus collectively managed by families. Since families are not legal persons but financial institutions are reluctant to lend against collateral not owned by the borrower alone; this limits farmers’ choice to avail of agriculture credit facilities from formal institutions.

On the other hand, farmers are also opposed to mortgaging their land as collateral, given that it is their only significant asset in many cases. Farmers must place their passbooks (ownership documents for agricultural holding) as collateral with the bank when they borrow. In case of failure in returning the borrowed credit, banks pledge ‘farmers’ entire holding. This may occur even if the per-acre value of land, in many cases, is higher than the State Bank’s approved per-acre credit ceiling for different crops (Younus, 2019).

Since, farmers are risk-averse (Sulewski et al. 2020) and avoid taking credit from formal institutions in the presence of alternates, i.e. informal sources. Because under informal arrangement farmers are certain that major asset “land” will not be grabbed in case of a defaulter. Religion is another factor as scholars declare charging of interest as forbidden. Farmers thus may also be reluctant to commit any sin intentionally.

If arthi faces any problem in recovering the lending amount from a farmer due to crop failure or any personal circumstances faced by the farmer at the time of repayment (such as the illness of a family member or marriage of a daughter etc.) arthi does not let the farmer force-close due to non-payment. Under such circumstances, the arthi recovers what the farmer can afford to repay, reschedule the outstanding amount, and extends a new loan to allow the farmer to plant his next crop. This implies that arthi rolls over the loan and reflects a flexible attitude to get his money back. Our discussion with farmers from different areas of Pakistan shows that it is an opposite model compared to the formal credit institutions. In the case of formal credit, if the farmer defaults, there is no other option except for the mortgage of land to face foreclosure. Even though, in some cases, a loan taken from the formal institution is only a small percentage of the total value of the collateralized asset. It might be because of strict policies introduced by the state bank of Pakistan implemented by commercial banks. However, in any case, it needs to be re-visit. Any flexibility from the formal institutes to reschedule the credit reimbursement could help to win the ‘farmer’s trust. This may help to increase the share of formal credit in the total credit market.

Arthies are more flexible and ready to work on a risk-sharing basis (crop failure, sickness in the ‘farmer’s family, and unforeseen events) which would otherwise place the farmer at a massive disadvantage in dealing with the lender. But still, as a common practice, arti ‘doesn’t demand any signature from farmers on any legal document (except arthi unilaterally noting it down for his record) while also no collateral is required either. In addition, no questions are asked regarding the purpose or utilization of the borrowed amount or the schedule for the release of funds to match with crop production stages.

But in return, the farmer must bring his produce for auctioning at the ‘lender’s shop and pay a commission on the value fetched. In case of failure, the farmer is accountable for paying interest in proportion to the shortfall that the farmer was supposed to bring for auction. However, in case of any disaster that leads to crop failure, the farmer is allowed to extend the repayment period of debt to enable him to plant the next crop and repay the combined outstanding loan amount upon harvest. Under these circumstances, the farmer is liable to pay interest only on the unpaid loan.

Is arthi an exploiter?

The availability of informal credit on flexible terms without stringent conditions or collateral requirements is no less than a blessing for poor farmers. No formal sector financial institution offers unsecured credit to farmers in Pakistan. This is one of the reasons why farmers prefer to avail credit facilities from informal sources even if they have to pay a high-interest rate in terms of commission on their products or in some other form.

Arthi, who is deeply embedded in the farm loan market, has fine-tuned his model to avoid adverse selection, reduce moral hazard, mitigate risk, and generate substantial profits in a sector that commercial bankers considered risky and unprofitable (Haq et al., 2013). Hence, commercial banks can learn from arthi’s experience to increase their share in the credit supply market by waiving the stringent conditions of documentation and sharing the production risk by rescheduling the credit.

The general perception and literature depict arthi as an exploiter in the food supply chain who abuses his power for personal gain at all costs. However, the reality is not so worse. Without any doubt, arthi charges four to five times the rate of interest than the formal institutions, but he also provides a service that the formal credit sector does not. Moreover, perceptions about arthi among farmers are mixed. Some farmers claim that arthi are helping hands in difficult times. Still, others demonstrate that these charges have very high-interest rates while acknowledging the financial support extended during the crisis.

References

ACAC (2019). Agricultural Credit Advisory Committee (ACAC) meeting held on November 19, 2019

Haq et al. (2013). Who is the “arthi”: Understanding the commission agent’s role in the agriculture supply chain. Working Paper, International Growth Centre. London School of Economics and Political Science. A study by National Institute of Banking & Finance (NIBAF) & Pakistan Microfinance Network (PMN), Funded through the International Growth Centre – Pakistan.

Saboor, A; Hussain, M; and Munir, M. (2009). Impact of microcredit in alleviating poverty: an insight from rural Rawalpindi, Pakistan. Pak J. Life Soc Sci, 7 (1) (2009), pp. 90-97

Sulewski, P; Adam W; Paweł, K; Kinga, P; Magdalena, S; and Tomasz, S. (2020). ‘Farmers’ Attitudes towards Risk—An Empirical Study from Poland. Agronomy, Vol. 10, 1555; MDPI. doi:10.3390/agronomy10101555

Younus, S. (2019). Agri-finance: are banks missing out on a big opportunity? Published in Daily Dawn, March 18, 2019.