The efficient allocation of capital plays a key role in development by nurturing innovation and increasing industrial productivity. However, the reallocation of capital towards less productive firms at the expense of more productive firms harms growth of industries. Recently economists have discussed the existence and rise of zombie firms which slowed down growth in several countries including neighboring India. A zombie firm is characterized as a loss-making firm that has lost the ability to generate enough profits to cover their interest payments. They survive only by repeatedly refinancing their loans. In the competitive market, zombies have to either exit or restructure. If zombie congestion rises, it potentially crowds out growth opportunities for more productive firms.

The notion of zombie firms was applied for the first time to Japanese firms during the period of the Lost Decade (1991-2000 – a period of economic stagnation in Japan). In that period, Japanese banks kept injecting new loans to unprofitable firms to keep them alive. The Japanese economy did not begin to recover until this practice of misallocation of capital had ended. Recent literature has revisited this connection and shown that misallocation of capital is emerging as a vital explanation for the fall in productivity of several OECD and Asian economies.

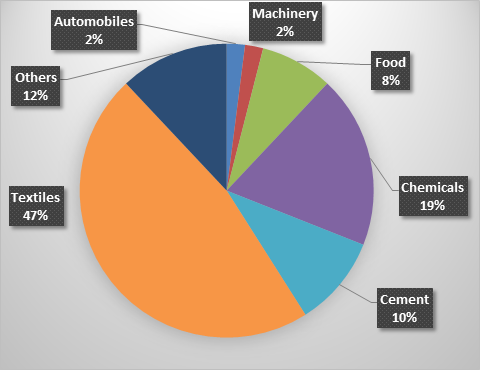

Rarely discussed, but the concentration of zombies is the real challenge for industrial growth in Pakistan as well. The misallocation of capital to these unprofitable firms indicates that credit reallocation is not always to the healthier, innovative, and more productive firms. Using balance sheets of the listed firms, we estimate the share of these unproductive firms in the marketplace. Our estimates suggest that approximately 25 percent of firms show up as the zombie firms in Pakistan. Furthermore, roughly 47% of these nonviable firms exist in textile, 19% in chemical, and 10% in the cement sector. The concentration of these firms is not limited to any particular sector. They exist both in the private and public sectors. Our estimates suggest, roughly USD 3 billion short term bank credit flows to these firms annually. In a resource scarce country such as Pakistan, it is reasonable to assume that the efficient allocation of this credit could improve performance of the industrial sector.

What are the potential sources for the prevalence of zombie firms in Pakistan? One driver is the tendency for banks to make evergreen loans to non-viable firms. This practice allows them to avoid showing losses on their balance sheet, and if they show the losses, they have to create provisions to balance their sheets. Second, the meager interest rate is another potential factor that reduces the pressure on creditors to clean up their balance sheets, which encourages banks to make evergreen loans to these firms. Third, public sector enterprises appear as zombie firms as well, which again is a big challenge to banks because public sector enterprises (PSEs) have faced high levels of debt or overcapacity. These firms have created a debt cycle, as they are often forced to borrow from banks to repay interest payments. Banks lend to them because they come with a government guarantee, and even keep lending with non-performing loans.

The support to zombie firms to stay alive impairs market competition. In this situation, banks let these unprofitable firms distort competition in the economy. They depress market prices and increase congestion of less productive firms in the market. The zombie’s distortion also impacts the overall productivity of industry and job creation that more productive firms could generate. The survival of unproductive firms for an extended period may crowd out investment opportunities, employment generation, and overall productivity of the industry that more productive firms could generate.

This debate should not distract from the contribution of banks in a hard time to support firms. However, the role of regulators is the key to break this ongoing debt cycle. Devising effective regulatory measures to capture the non-viable firms in the marketplace, regulators can generate larger space for the more productive and small-medium enterprises (SMEs) to access credit. Priority in credit access to productive firms, as well as small-medium and innovative enterprises, would improve the health of financial markets and may reap higher investment and employment generation in the country.