What Do We Know of Trade Elasticities?

Hafsa Hina,[1] Pakistan Institute of Development Economics, Islamabad.

Devaluation[2] is necessitated only when policy weakness leads to a loss of reserves. It takes on a harsher form when central banks refuse to recognize the will of the market and spends reserves to preserve an artificial value of the exchange rate.

Ill-informed popular debate appears to hold to the notion that the purpose of a devaluation is to devalue to improve the trade balance and as they say “improve competitiveness.”

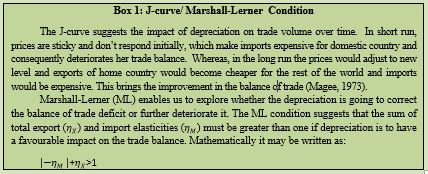

There is an old debate on whether exchange rate depreciation impacts the trade balance positively or not. We will summarize that here.

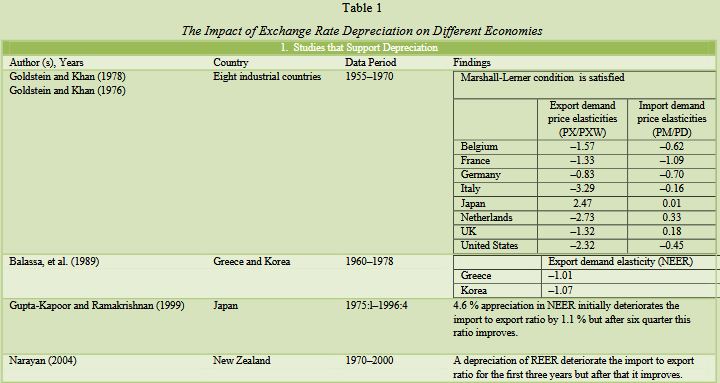

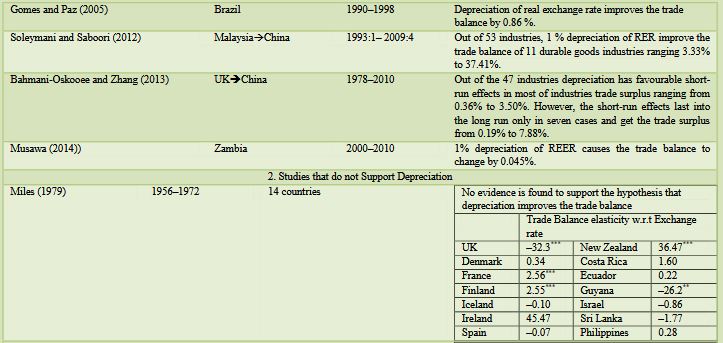

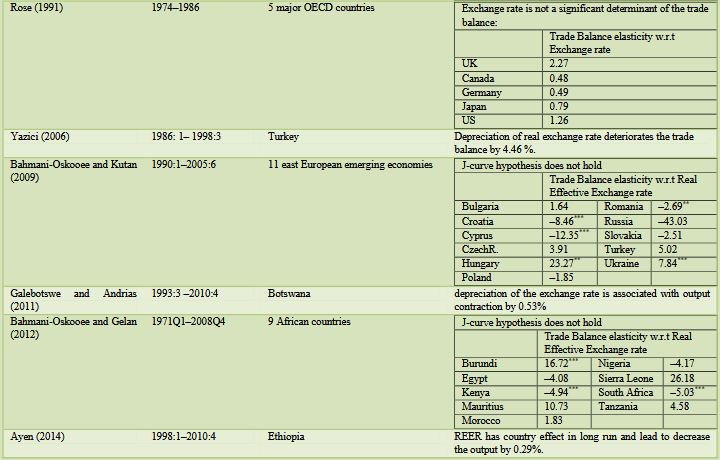

The impact of an exchange rate depreciation on trade balance has not been widely endorsed. The studies in the area of depreciation can be divided into two groups. The first group of studies supports the view that depreciation is successful in improving the trade balance and demand for exports and imports are responsive to exchange rate. Whereas, the second group that do not lend support to the effectiveness of depreciation in resolving the trade deficit problem (see Table 1).

Note: PX= price of exports; PXW= weighted average of the export prices of the country’s trading partners; PM is import prices, PD is domestic price. ***, ** indicates significance at 1% and 5%.

Note: PX= price of exports; PXW= weighted average of the export prices of the country’s trading partners; PM is import prices, PD is domestic price. ***, ** indicates significance at 1% and 5%.

____________________________

[1] The author’s thanks goes to Nadeem Ul Haque, Abdul Jalil and Usman Qadir, their suggestions prompted to revise the document and to make it valuable. The author remain responsible for any errors and weaknesses.

[2]In this study devaluation and depreciation will be used interchangeably and market based flexible exchange rate system followed by SBP from July 2000.

Here we will review the evidence from Pakistan to inform policymaking and local research about

- The elasticities of imports and exports with respect to income, relative prices and exchange rate;

- Examine the short-term effect and long term effect of the real depreciation of PKR on the real imports and real exports of Pakistan; and

- Investigate the existence of J-curve Phenomena.

Survey of Empirical Studies on the Demand for Imports and Exports in Pakistan

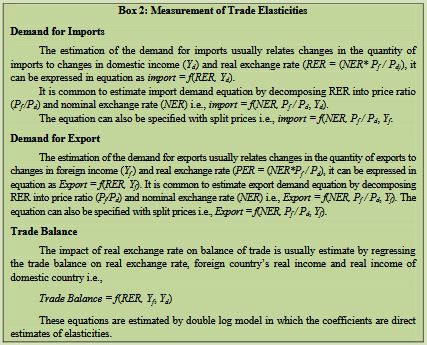

In the field of international economics, income and price elasticities are useful in determining the trade flows. Income elasticities measures how the trade flows respond to change in GDP and price elasticities access the impact of changes in relative prices, tariffs and/or exchange rates on trade flows (see Box 2).

These elasticities are especially critical to the Pakistan economy because of rising trade deficit. In case of Pakistan, there is a vast amount of the literature focuses on the role of exchange rates in affecting the trade balance or, more specifically the demand for exports and imports both at aggregated and disaggregated (commodity wise, industry wise and country wise) level. Here we are reviewing the studies that measures the elasticities at aggregated level.

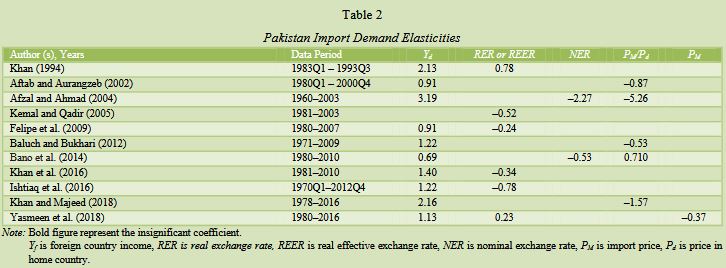

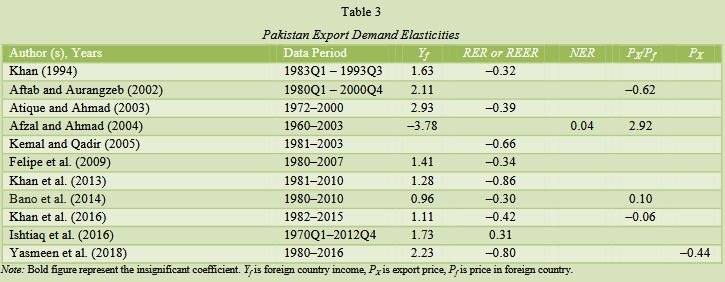

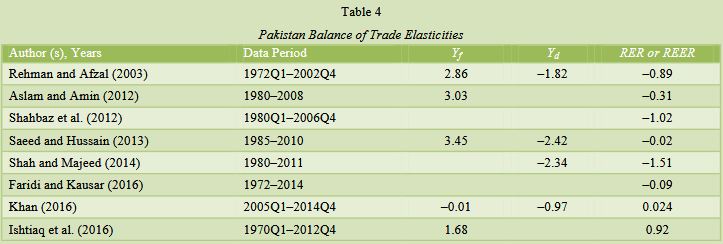

The Tables 2, 3 and 4 provide the elasticities of import, export and balance of trade with respect to exchange rate, prices and income. Instead, they vary depending on their sample period, data frequency, empirical methods and modelled macroeconomic variables.

Conclusions of these studies exhibit no common pattern regarding the role of exchange rates in determining trade flows.

- In case of export demand, the range of real exchange rate elasticity lies between –0.80 to –0.30 (except Ishtiaq et al., 2016). It means that Pakistan’s export demands do not increase in a significant way with the depreciation of exchange rate.

- Increase in world income has positive impact on export demand.

- For import demand, the range of real exchange rate elasticity lies between –0.24 to –0.78 (except Khan (1994) and Yasmeen et al. (2018)). It means that depreciation of real exchange rate decreases the import’s demand at low rate.

- Increase in domestic income boosts the demands of foreign product.

- Real exchange rate depreciation will not lead to improve the balance of trade its ranges between –1.51 to –0.02.

Beside the exchange rate there are other factors behind the persistent trade balance and limits the role of exchange rate policies to correct the trade balance. Such as:

(1) Most of Pakistan’s imports consist of capital and intermediate goods. This dependence makes import demand relatively inelastic and unresponsive to exchange rate policies.

(2) Agricultural goods have inelastic supply and most of Pakistan’s exports are consisting of agricultural goods. Therefore, export demand may be less sensitive, in term to its prices and the world income and depreciation policy did not have much effect on the export volume.

(3) Low Value addition in Pakistan’s exports due to low development of industrial sector, Pakistan has not yet expanded her product range in favour of technology-intensive products.

Does currency depreciation necessarily result in positive exports and negative imports? Evidence from the updated data

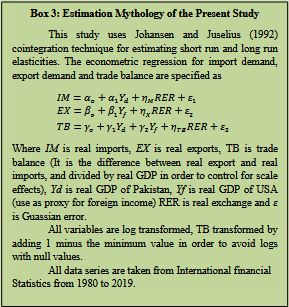

The exchange rate policies of Pakistan and their relationship to trade flow is presented in Box 3.

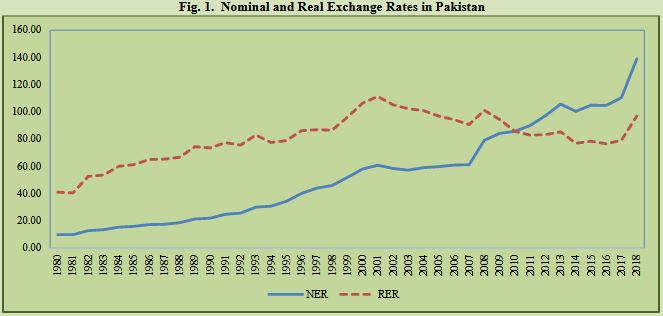

The visualization of nominal and real exchange rate of PKR against US $ is depicted in Figure 1. Rise in NER and RER shows the depreciation of nominal and real exchange rate respectively. From 1980 to 2001 both lines follow the same direction but after that NER and RER have been moving in opposite directions as the SBP started pursuing a policy of intermittently fixing the exchange rate even as crises happened. It indicates that domestic prices are increasing relative to foreign prices and offsetting the impacts of NER depreciation. In the past few years, despite of significant amount of nominal depreciation, real depreciation has not occurred, in fact RER has moved in opposite direction. Clearly SBP exchange rate policy was standing against the market. SBP should not try to use reserves to fix the value of the exchange rate except to deal with very short-term disorderly conditions. Otherwise, currency crises or attacks happen if the SBP attempts to use reserves to hold the exchange rate against the market.[3]

| Box 3: Exchange Rate Policies and Trade Flow of Pakistan Pakistan followed a policy of export-led growth in order to bring the sustainability in her balance of payments. To achieve this objective, Pakistan had adopt various exchange rate regimes from fixed exchange rates to a policy of managed float. · In January 1982 Pakistan rupee was delinked from the US $. Previously the rupee/dollar exchange rate was fixed and appreciation of the US $ in 1980-81 had reduced the competitiveness of Pakistan’s export in the international market. The floating exchange rate policy helped the import liberalization process by allowing the government to eliminate restrictions without running into balance of payment problems because the exchange rate was set by the market force. Under the new system, State Bank of Pakistan used to set an exchange rate of PKR based on trade weighted currency basket. · PKR has been devalued by 39 percent, for the period of 1982–87. During this period, export earnings boosted by 65 percent and balance of trade improved by 27.3 percent. It should be keep in mind that beside devaluation, incentives were given to industrialist to increase manufactured exports and the Economic Co-operation Organization (ECO) and the South Asian were found in 1980s to increase trade with in South Asian region. These improvements could not be sustained over a long period because of political instability in the country and rapid increases in oil prices. Managed float was abolished by the State Bank of Pakistan in July 2000 and flexible exchange rate system was finally achieved. Trade policies are highly liberalized after 2000, average tariff rate was reduced from 47% in 1990s to 18% in 2000s (FBR, year book 2018-2019). During this period both export and import sector showed improvement. Regardless of, the average annual growth rate of imports is 14% greater than the annual growth rate of exports i.e., 10%. |

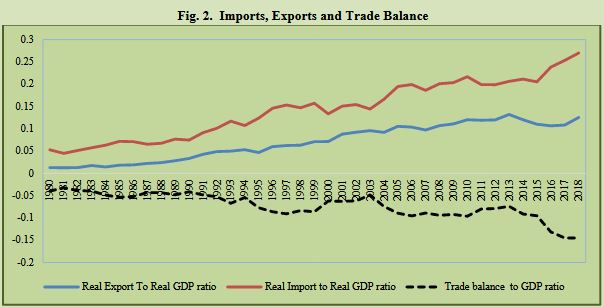

As Figure 2 shows this flawed exchange rate policy has also showed up in the trade balance. While Pakistan as a developing country had a trade balance but in as exchange rate policy took on an increasing anti market stance, imports started to grow and exports more or less stagnated to lead to a widening trade balance. The imports grew faster than the exports and have almost been always higher than the exports.

______________________________

______________________________

[3] PIDE’s Knowledge Brief No. 7:2020, Pakistan’s five currency crisis by Nadeem Ul Haque and Hafsa Hina.

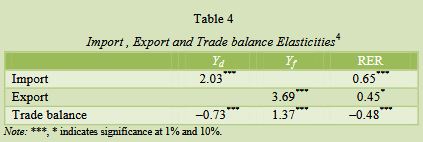

Table 4, shows that:

Table 4, shows that:

(1) 1% depreciation of real exchange rate of PKR will increase the demand for exports by only 0.45% and increase the demand for imports by 0.65%. Therefore, trade balance deteriorate by 0.48%.

(2) Marshall Lerner condition does hold for Pakistan because as export elasticity is according to theory and depreciation would increase the demand for export. But, import elasticity is opposite to theory and deprecation would not reduce the demand for imports. Therefore, at aggregate level, Pakistan will remain a net importer and depreciation policy will not improve its trade balance.

CONCLUSION

Depreciation is an outcome as a country loses reserves rather than a policy option to improve trade. Elasticities reflect the structure of the economy. Export elasticity reveals that export demand is less responsive to change in real exchange rate. It shows that we are still exporting commodities with no Pakistan brand. For example, most of our primary goods such as basmati rice are exported to the name of other country brands. Brand loyalty protects the goods in the international market and it is necessary to educate exporters about the branding of their products. Import demand is also inelastic to change in real exchange rate. Our major imports are based on machinery and petroleum products, which serve as necessity input in production. Inelastic import demand reveals that we have made no progress on developing energy saving and remain dependent on imported energy. Therefore, exchange rate policy can do nothing on the structure. In fact, the need for a devaluation is the inefficiencies in the structure of the economy. Thus the choice is clear reform to fix the structure or let the exchange rate to depreciate.

__________________________

[4] The cointegration results are highly sensitive to the choice of the lag length, structural break and the coefficients may vary with trade regimes. The issue of structural break and trade elasticities for different trade regimes are addressed in the working paper 24:2020 of PIDE.

REFERENCES

Aftab, Zehra & Khan, Aurangzeb (2002). The long-run and short-run impact of exchange rate devaluation on Pakistan’s trade performance. The Pakistan Development Review, 41(3), 277–286.

Afzal, M. & Ahmad, I. (2005). Estimating long-run trade elasticities in Pakistan: A cointegration approach. The Pakistan Development Review, 43(4), 757–770.

Ali, A. (2014). Share of imported goods in consumption of Pakistan. SBP Research Bulletin, Short Notes, 10(1), 57–61.

Ayen, Y. W. (2014). The effects of currency devaluation on output: The case of Ethiopian economy. Journal of Economics and International Finance, 6(5), 103–111.

Bahmani-Oskooee, M. & Gelan, A. (2012). Is there J-curve effect in Africa? International Review of Applied Economics, 26(1), 73–81.

Bahmani-Oskooee, M. & Kutan, A. M. (2009). The J-curve in the emerging economies of Eastern Europe. Applied Economics, 41(20), 2523–2532.

Bahmani-Oskooee, M. & Zhang, R. (2013). The J-curve: Evidence from commodity trade between UK and China. Applied Economics, 45(31), 4369–4378.

Bahmani-Oskooee, Mohsen (1998). Cointegration approach to estimate the long-run trade elasticities in LDCs. International Economic Journal 12(3), 89–96.

Balassa, B., Voloudakis, E., Fylaktos, P., & Suh, S. T. (1989). The determinants of export supply and export demand in two developing countries: Greece and Korea. International Economic Journal, 3(1), 1–16.

Baluch, K. A. and Syder, S. K. B. (2012). Price and income elasticity of imports: The case of Pakistan. State Bank of Pakistan, Research Department. (SBP Working Paper Series 48).

Bano, S. S., Raashid, M., & Rasool, S. A. (2014). Estimation of Marshall Lerner condition in the economy of Pakistan. Journal of South Asian Development, 3(4), 72–90.

Chaudhary, M. A. & Amin, B. (2012). Impact of trade openness on exports growth, imports growth and trade balance of Pakistan. Forman Journal of Economic Studies, 8, 63–81.

Faridi, M. Z. & Kausar, R. (2016). Exploring the existence of J-curve in Pakistan: An empirical analysis. Pakistan Journal of Social Sciences, 36(1), 551–561.

FBR, Year Book (2018-19). Ministry of Finance, Government of Pakistan.

Felipe, J. S., McCombie, L., & Naqvi, K. (2009). Is Pakistan’s growth rate balance-of-payments constrained? Policies and implications for development and growth. (ADB Economics Working Paper Series No. 160).

Galebotswe, O. & Andrias, T. (2011). Are devaluations contractionary in small import-dependent economies? Evidence from Botswana. Botswana Journal of Economics, 8(12), 86–98.

Goldstein, M. & Khan, M. S. (1978). The supply and demand for exports: A simultaneous approach. The Review of Economics and Statistics (May): 275–286.

Goldstein, M. & Mohsin, S. K. (1976). Large versus small price changes and the demand for imports. IMF Staff Papers 23, 200–225.

Gomes, F. A. & Paz, S. (2005). Can real exchange rate devaluation improve the trade balance? The 1990–1998 Brazilian case. Applied Economics Letters, 12(9), 525–528.

Gupta-Kapoor, A. & Ramakrishnan, U. (1999). Is there a J-curve? A new estimation for Japan. International Economic Journal, 13(4), 71–79.

Hasan, Aynul & Khan, Ashfaque H. (1994). Impact of devaluation on Pakistan’s external trade: An econometric approach. The Pakistan Development Review, 33(4), 1205–1215.

Hussain, M. (2016). J-curve analysis of Pakistan with D-8 group. Euro-Asian Journal of Economics and Finance, 4(3), 68–80.

Ishtiaq, N., Qasim, H, M., & Dar, A. A. (2016). Testing the Marshall-Lerner condition and the J-curve phenomenon for Pakistan: Some new insights. International Journal of Economics and Empirical Research, 4(6), 307–319.

Johansen, S. & Juselius, K. (1992). Testing structural hypothesis in a multivariate cointegration analysis of the PPP and UIP for UK. Journal of Econometrics, 53, 211–44.

Kemal, M. A. & Qadir, U. (2005). Real exchange rate, exports, and imports movements: A trivariate analysis. The Pakistan Development Review, 44(2), 177–195.

Khan, F. N. & Majeed, M. T. (2018). Modelling and forecasting import demand for Pakistan: An empirical investigation. The Pakistan Journal of Social Issue, 10, 50–64.

Khan, S., Khattak, U., S., Amin, A. & Ashar, H. (2016). Empirical analysis of aggregate export demand of Pakistan. Journal of Global Innovations in Agricultural and Social Sciences, 4(1), 50–55.

Khan, S., Azam, M., & Emirullah, C. (2016). Import demand income elasticity and growth rate in Pakistan: The impact of trade liberalization. Foreign Trade Review, 51(3), 1–12.

Khan, Shahrukh R. & Aftab, S. (1995). Devaluation and balance of trade in Pakistan. The Pakistan Development Review.

Khan, S., Khan, S. A., & Zaman, K. U. (2013). Pakistan’s export demand income and price elasticity estimates: Reconsidering the evidence. Research Journal of Recent Sciences, 2(5), 59–62.

Magee, S. (1973). Currency contract, pass through and devaluation. Brooking Papers on Economic Activity, 303–325.

Miles, M. (1979). The effects of devaluation on the trade balance and the balance of payments: Some new results. Journal of Political Economy, 87(3), 600–620.

Musawa, N. (2014). Relationship between Zambias exchange rates and the trade balance J-curve hypothesis. International Journal of Finance and Accounting, 3(3), 192–196.

Narayan, P. K. (2004). New Zealand’s trade balance: Evidence of the J-curve and granger causality. Applied Economics Letters, 11, 351–354.

Rahman, M. & Islam, A. (2006). Taka-Dollar exchange rate and Bangladesh trade balance: Evidence on J-curve or S-curve? Indian Journal of Economics and Business, 5, 279–288.

Rehman, Ur, H. & Afzal, M. (2003). The J-curve phenomenon: An evidence from Pakistan. Pakistan Economic and Social Review, 41(1), 45–58.

Rose, A. K. (1991). The role of exchange rates in a popular model of international trade: Does the Marshall-Lerner condition hold? Journal of International Economics, 30, 301–316.

Saeed, B, M. & Hussain, Ijaz (2013). Real exchange rate and trade balance of Pakistan: An empirical analysis. Jinnah Business Review, 1(1), 44–51.

Shah, A. & Majeed, T. M. (2014). real exchange rate and trade balance in Pakistan: An ARDL co-integration approach. University Library of Munich, Germany. (MPRA Paper 57674).

Shahbaz, M., Jalil, A., & Islam, F. (2012). Real exchange rate changes and the trade balance: The evidence from Pakistan. The International Trade Journal, 26(2), 139–153.

Shahzad, A. A., Nafees, B., & Farid, N. (2017). Marshall-Lerner condition for South Asia: A panel study analysis. Pakistan Journal of Commerce and Social Sciences, 11(2), 559–575.

Soleymani, A., Chua, S. Y., & Saboori, B. (2011). The J-curve at industry level: Evidence from Malaysia-China trade. International Journal of Economics and Finance, 3(6), 66–78.

Yasmeen, R. & Hafeez, M. (2018). Trade balance and terms of trade relationship: Evidence from Pakistan. Pakistan Journal of Applied Economics, 28(2), 173–188.

Yazici, M. (2006). Is the J-curve effect observable in Turkish Agricultural sector? Journal of Central European Agriculture, 7(2), 319–322.