by Mr. Shahid Sattar

Large Scale Manufacturing and Economic Growth

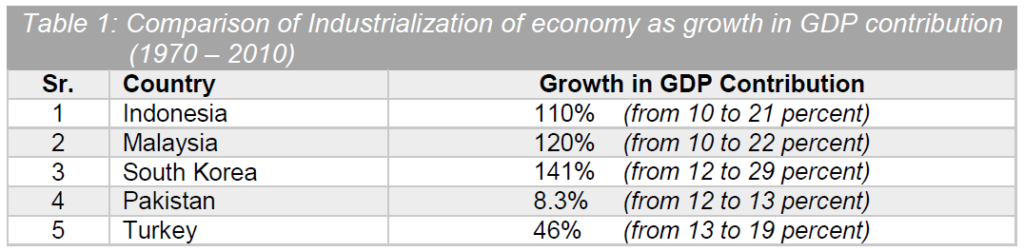

Large Scale Manufacturing (LSM) is sine qua non for achieving sustained economic growth. In the case of Pakistan, the contribution of LSM to total manufacturing is 78%. It contributes 9.5% and 12.6% respectively to national GDP and the labor force. However, the sector has been witnessing a decline for the past couple of years. It has shrunk from a significant 7.74% in June 2020 and 2.28% in FY 2019. The decline has resulted in unemployment coupled with a slowing of the economy owing to COVID-19. We have lost 1 out of every 5 jobs and they may not come back because of contracting of LSM. This can further aggravate the already contracting documented economy with lower tax revenue. But even before hitting decline, did Pakistan really industrialize? Historically, our industrialization has been the least compared to other developing countries in over 40 years.

If LSM growth is a proxy for industrialization, with the sector already in decline, are we headed towards deindustrialization? And more importantly, is this deindustrialization premature given the country’s socioeconomic realities?

The Numbers on Negative Growth

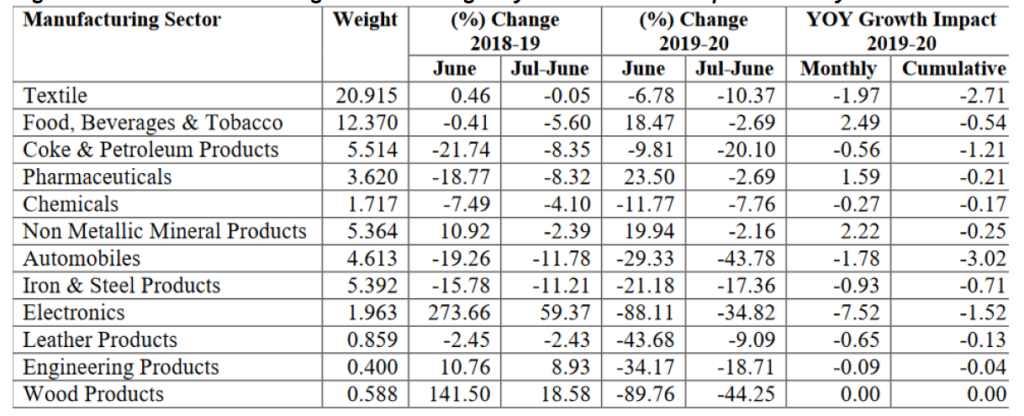

It is important to understand what has really been driving the negative growth in the LSM sector in recent years. The Quantum Index of Manufacturing (QIM), is a performance representation of the LSM sector. Formulation of the index is from the contribution of large-scale industries by weight. The sectors carrying the top 3 weights: Textiles (20.92%), Food, Beverages & Tobacco (12.37%) and Coke & Petroleum Products (5.51%). These post a grim look in the overall economy whereas others like Automobiles, Leather Products and Wood Products, albeit carrying less weight (6.6%, 1.2% and 0.8% respectively), have witnessed a dramatic decline with an activity drop of near zero (97%, 94.6% and 89.9% respectively) as of April 2020.

According to research by Business Recorder, we may regard the consecutive LSM contraction as manufacturing recession leading to widespread unemployment. Pakistan’s economy needs to grow by 7% per annum to absorb the new entrants to labor market each year. It is safe to assume that the number has increased many folds over the years. Sadly data collection for unemployment is totally flawed and patchy in Pakistan. So we may never be able to predict the growth rate against the required employment.

The Drivers of this Growth

Pakistan’s upward adjustment in energy tariffs, coupled with the abolishment of zero rated regimes for export sectors, has resulted in increased cost of business, severe liquidity crisis and reduced overall profitability for businesses. The textile industry of Pakistan, for instance–20.9% in QIM – bears the burden of the highest energy tariffs in the region. Electricity, although recently reduced from 13.3 cents/kWh to 9.0 cents/kWh, and gas at $6.5 / MMBTU – is still significantly higher than regional players like India and Bangladesh (7.2 cents/kWh and 7 cents/kWh, and $3.2/ MMBTU respectively). India in the meantime is devising market capture strategies through introduction of new incentives and even lower energy rates. Not surprisingly, the resultant impact is that textile companies have become regionally noncompetitive. This jeopardizes the sector’s potential to double exports and contribute positively to export-led growth in the coming years.

Other factors such as rupee depreciation, contractionary monetary and fiscal policies, and the country’s recent austerity drive, have also contributed to the decline in LSM and had huge negative fallout on the industrial sector. For industries relying on imported raw materials, rupee depreciation had a significant impact on their cost structure. Furthermore, tariff and non-tariff barriers discourage import of quality raw materials for better output while also making production regionally noncompetitive. Curbing inflation by hiking the policy rate increases cost of borrowing, discourages investments, subdues demand and further hampers overall production and performance of industries. Resultantly, sectors that practically halted their operations also contributed to the decline in LSM. For instance, the automobile sector alone accounted for a major portion of contraction in LSM (-36.5% during July-March FY 2020).

An Odd and Unsettling Deindustrialization

But what is it about Pakistan’s deindustrialization that is odd and unsettling? Economies deindustrialize to shift their comparative advantage. In recent years, the UK lost comparative advantage in clothing and electrical manufacturing to that in financial services. Similarly, between 1979 and 2016, the US faced deindustrialization as employment in manufacturing fell from 19 million to 12 million whilst manufacturing output increased owing to technological advancement. In Pakistan’s case, a significant simultaneous growth in the tertiary sector, or any serious technological upgradation or advancement, hasn’t occurred alongside the LSM contraction. Instead, poor policies, mismanaged resources, a persistent trade deficit and habitual borrowing with no planning for compensating growth in any of the complementary sectors is the real cause of deindustrialization. This raises question, who will then invest in LSM under such circumstances?

If the decline in Pakistan’s LSM isn’t due to a maturing economy, the oddity is likely to have economic repercussions. Planning to rejuvenate LSM sector will be required and must be coupled with growth in other complementary sectors. This will cater to employment for incoming youth bulge and allow focus on potential underutilized areas to regenerate growth. Industries facing the decline in productivity and manufacturing employment, and increase in current account deficit and external debt may never recover from the shock, while complementing growth from the tertiary sector may largely remain absent. This is not to say that all is bleak, however.

A Silver Lining Perhaps?

One silver lining has been a modest rise in employment in the services sector over the past decade, implying better living standards, growth in digital financial services and infrastructure development. Additionally, special package for construction sector form the government amounting to PKR 30 billion will boost growth in some of the sectors and generate employment.

But time has been testament to developed economies breaking the vicious cycle of poverty and achieving higher standards of living through industrialization and metamorphosed deindustrialization. Before Pakistan deindustrializes, it needs to give the manufacturing sector its due in the form of supportive policies and plans, allowing them to build capacity, operate at full potential and contribute to economic growth that may include creating new economic and industrial zones for innovation and entrepreneurial opportunities. Regionally competitive energy tariffs, credit schemes for importing machinery, and embedding a structured technology upgrading framework embedded in industrial policy will be first steps in the right direction.

About the Author: Mr. Shahid Sattar is Executive Director, All Pakistan Textile Mills Association

Why does Pakistan continue to ignore the significance of incremental innovation and imitation in improving economic competitiveness and value addition. why do we not discuss economic evolution and possible future paths as a state and as a society. Perhaps its time we considered a national innovation policy, engage in research for productivity and growth, and encourage technological development in all sectors.

UK is a bad example. UK shifted to financialization because it created tax havens and foreign funds boosted financialization. Should read Tom Brown’s book discussed in this article here:

https://www.standard.co.uk/business/anthony-hilton-british-business-and-what-went-horribly-wrong-a3640336.html

Pakistan needs to industrialize more to provide better jobs for people.

Do not need big firms to be successful in industrialization if SMEs can cluster. Look at Italy, the 2d leading manufacturing power in EU-which uniquely has majority of micro small SMEs. It is renowned for its clusters: https://www.unido.org/sites/default/files/2008-05/the_italian_SME_experience_and_possible_LL_0.pdf

THE ITALIAN SME EXPERIENCE AND POSSIBLE LESSONS FOR EMERGING COUNTRIES

Researchers have linked IMF to deindustrialization, which could also be an issue in Pakistan https://www.sciencedirect.com/science/article/abs/pii/0305750X9290138L Deindustrialization, adjustment, the World Bank and the IMF in Africa https://link.springer.com/chapter/10.1007/978-3-030-10743-7_3 Latin America Since the 1990s: Deindustrialization, Reprimarization and Policy Space Restrictions https://www.academia.edu/5571042/Increasing_Poverty_in_a_Globalised_World_Marshall_Plans_and_Morgenthau_Plans_as_Mechanisms_of_Polarisation_of_World_Incomes Increasing_Poverty_in_a_Globalised_World_Marshall_Plans_and_Morgenthau_Plans_as_Mechanisms_of_Polarisation_of_World_Incomes

Continuing my comment: Italy has been supporting SME cluster policy in Vietnam since 2009:

https://www.unido.org/news/italy-contributes-eur-3-million-sme-cluster-development-vietnam Italy Contributes EUR 3 Million to SME Cluster Development in Vietnam