The sharp increase in current account deficits together with a large external debt servicing burden led to one of the highest default risks for Pakistan during 2022 and 2023. As costly as it has been, the subsequent collapse in economic activity driven largely due to the drying up of external financing to sustain domestic demand and contractionary policies implemented by fiscal and monetary authorities has helped address some of the imbalances. In the last 15 months, Pakistan’s imports have been less than the sum of its dollar income – exports and remittances – by almost $6 billion. As a result, the country’s default risk has also decreased substantially. The CDS spreads have declined from close to 60 percentage points to less than 30 percentage points. This is still incredibly high, but the trend is encouraging.

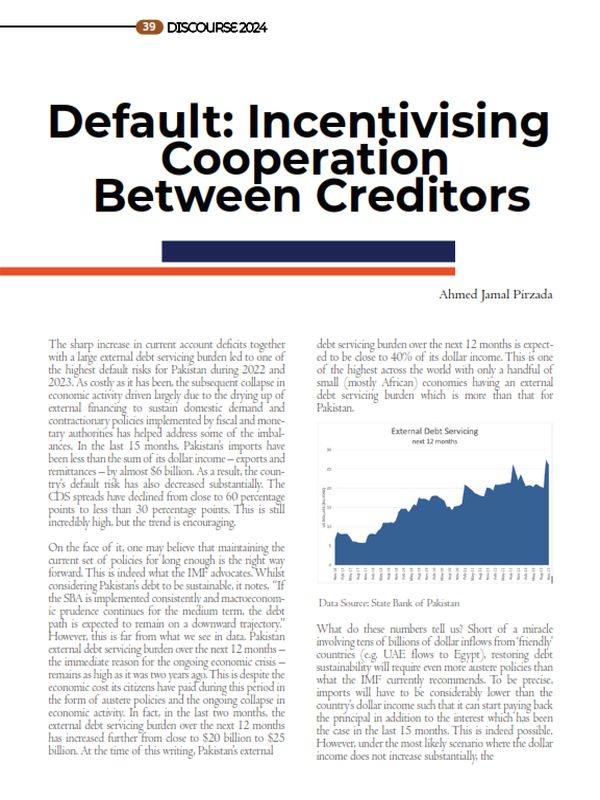

On the face of it, one may believe that maintaining the current set of policies for long enough is the right way forward. This is indeed what the IMF advocates. Whilst considering Pakistan’s debt to be sustainable, it notes, “If the SBA is implemented consistently and macroeconomic prudence continues for the medium term, the debt path is expected to remain on a downward trajectory.” However, this is far from what we see in data. Pakistan external debt servicing burden over the next 12 months – the immediate reason for the ongoing economic crisis – remains as high as it was two years ago. This is despite the economic cost its citizens have paid during this period in the form of austere policies and the ongoing collapse in economic activity. In fact, in the last two months, the external debt servicing burden over the next 12 months has increased further from close to $20 billion to $25 billion. At the time of this writing, Pakistan’s external debt servicing burden over the next 12 months is expected to be close to 40% of its dollar income. This is one of the highest across the world with only a handful of small (mostly African) economies having an external debt servicing burden which is more than that for Pakistan.

Data Source: State Bank of Pakistan

What do these numbers tell us? Short of a miracle involving tens of billions of dollar inflows from ‘friendly’ countries (e.g. UAE flows to Egypt), restoring debt sustainability will require even more austere policies than what the IMF currently recommends. To be precise, imports will have to be considerably lower than the country’s dollar income such that it can start paying back the principal in addition to the interest which has been the case in the last 15 months. This is indeed possible. However, under the most likely scenario where the dollar income does not increase substantially, the socio-economic cost which the citizens will be required to pay will increase to an extent where the reliance on austere policies alone will no longer be economically desirable even if not completely outrageous. As Rogoff (2022) notes, “Yet in some cases, particularly where the inherited debt burden is exceptionally large, it is by no means obvious that the debtor country’s low- and middle-income citizens fare better under an IMF-style adjustment plan than they would do in an outright default, or equivalently a rescheduling of repayments that lower the market value of the debt.”

Indeed, IMF itself notes that a ‘slower medium-term growth’ than what it currently projects will undermine its assessment that Pakistan’s debt is sustainable. This is revealing as IMF’s projections are in fact very much based on the ‘miracle’ assumption that tens of billions of dollar inflows from international creditors will materialise in the next few years. For example, IMF projects external inflows from international private creditors to increase from close to $7 billion during FY23 and FY24 to $15 billion in FY25. It further projects these to increase to $21 billion by FY28. This assumption underpins IMF’s projection that the GDP growth will increase to 3.5% in FY25 and to 5% by FY27. Such projections based on miraculous assumptions already undermine IMF’s assessment that Pakistan’s debt is sustainable.

Where do we go from here? Ideally, a well-functioning debt restructuring framework at the global level is the most desirable solution to the problem of debt sustainability. This is increasingly important with China emerging as one of the largest creditors but with geopolitical interests which do not always align with creditors associated with the Paris Club. The game where the creditors (or groups of creditors) are most incentivised to pass on the cost of restructuring to others due to conflicting interests and an absence of a cooperative framework leaves countries stuck in a debt trap with no good options but to consider the possibility of an outright default which will force the creditors to cooperate towards a mutually beneficial outcome even if through a messy process. The most recent example of this is Sri Lanka.

So, with every intention to provoke the reader, the big question I want to ask is should Pakistan default? At the core of it, this question is hardly provocative and simply a matter of considering the trade-offs involved. If the cost of continuing with the austere policies outweighs the cost the country will have to pay if it chooses to default, then the interesting question is not whether the country should default but, instead, why it chooses not to. Rogoff (2022) notes that this could be because the IMF programs “are overly focused on ensuring that foreign private creditors get paid in full and on time” and debtor country governments “often keen to avoid a politically destabilizing default.” However, before one could answer this question, one must ask what is the cost Pakistan will have to pay if it chooses to default? To answer this, let’s consider the case of Sri Lanka.

In the first quarter of 2022 Sri Lanka recorded a trade deficit of $1.59 billion. While close to $0.7 billion of the trade deficit was financed by remittances, the rest was financed by central bank reserves. Soon after, with reserves falling below $2 billion, Sri Lanka’s government chose to default in April 2022. The depletion of reserves and the drying up of financial flows from the rest of the world in preceding quarters meant that Sri Lanka could no longer sustain the high levels of trade deficits. As a result, the exchange rate collapsed, and the economy experienced a sharp slowdown with the GDP growth falling from close to 0% in the first quarter of 2022 to -7.4% in the second quarter[1].

This adjustment was necessary to bring imports to a level which could be financed using the country’s dollar income. Worse still, Sri Lanka’s banking system’s exposure to external creditors as discussed below required imports to fall even further. Trade deficit fell from $1.59 billion in the first quarter of 2022 to $0.67 billion in the second quarter and $0.16 billion in the third quarter of 2022. It recovered in subsequent quarters but only due to an increase in remittances thus allowing the country to finance more imports than it could in the immediate aftermath of the sovereign default. According to recent reports, Sri Lanka’s GDP is projected to grow at 1.6% in 2024 but only after contracting by 7.8% and 3.6% in 2022 and 2023, respectively. Overall, Sri Lanka’s economy has contracted by 11.7% in the period after default[2].

Sri Lanka is a useful example to highlight the significant cost associated with sovereign default. However, critically, these also depend on factors which are not common to Pakistan. First, and the most important, Pakistan’s dollar income has been more than its imports by a significant amount over the last 15 months. Therefore, unlike Sri Lanka, Pakistan will be able to finance more imports than what is currently possible once it suspends its debt repayments. Second, the cost of default is amplified if the country’s banking system plays an important role in the economy (Obstfeld et al., 2010). This is indeed the case for Sri Lanka where bank deposits amounted to 60% of GDP just before the crisis. In contrast, bank deposits amount to only 35% of GDP in the case of Pakistan.

Third, the exposure of domestic banks to external financing is another critical factor which can exacerbate the crisis. Default and subsequent restructuring of domestic debt sent the Sri Lankan banks scrambling for dollars to service the maturing credit lines they had in place from external sources but could no longer be renewed. It is reported that Sri Lankan banks have repaid $3.4 billion in debt to their external creditors since April 2022[3]. These were raised from the open market thus putting additional pressure on the exchange rate and requiring an even bigger slowdown in economic activity to generate necessary current account surpluses. Once again, this is not case for Pakistan.

The discussion above highlights that the cost of default will be nowhere close to what we have seen in the case of Sri Lanka. Instead, the biggest risk will come from the restructuring of domestic debt due to excessive exposure of the banking system to the sovereign. This will require measures such as preventing banks from giving out dividends and, instead, using these to build capital over a few years. Additionally, it will make sense for the government to temporarily relax regulatory requirements around capital adequacy ratio while the central bank announces a much more proactive role for itself in providing liquidity whenever the need arises. Finally, the fragility of the banking system in the context of domestic debt restructuring can be presented to international creditors in a credible and transparent manner to convince them that any largescale restructuring of domestic debt will undermine the long-term success of any new arrangement that is reached at the end of restructuring process.

Perhaps a miracle will happen and the assumptions underlying IMF projections will come true even if these haven’t in the last two years. But in the more realistic scenario where these don’t, it is important to consider the trade-offs between keeping the economy paralysed under the long shadow of short-term rollovers or an outright default which forces the creditors to sit on the table and start talking. I am tempted to argue that the latter option is less costly than the former.

The author is a Senior Lecturer and School Resource Director at the University of Bristol’s Economics Department.

[1] National Accounts Estimates – 2023 Q2. Statistics Department, National Bank of Sri Lanka. https://www.cbsl.gov.lk/sites/default/files/cbslweb_documents/national_accounts_estimates_2023_q2.pdf

[2] Reuters: Sri Lanka’s economy returns to growth, led by agriculture. https://www.reuters.com/markets/asia/sri-lankas-economy-returns-growth-led-by-agriculture-2023-12-15/

[3] EconomyNext: Sri Lanka banks repay debt or collect US$1.7bn to Sept 2023. https://economynext.com/sri-lanka-banks-repay-debt-or-collect-us1-7bn-to-sept-2023-142275/