Inviting FDI: Is Pakistan an Attractive Destination?

INTRODUCTION

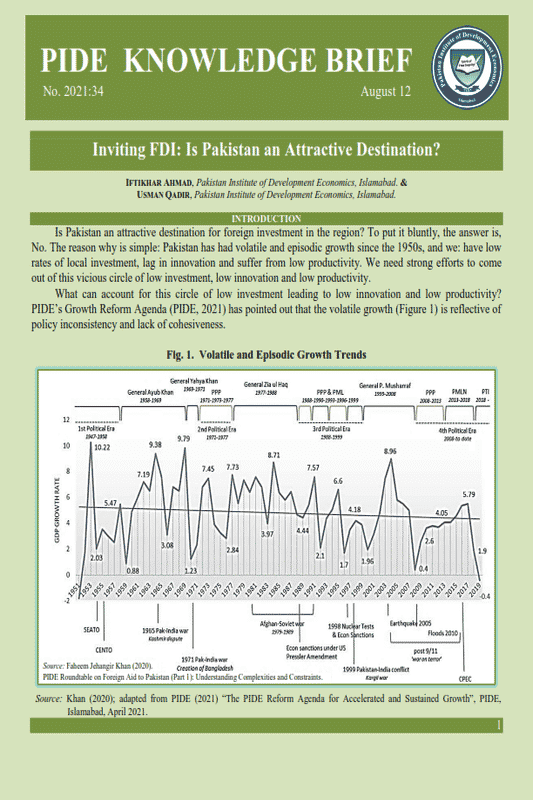

Is Pakistan an attractive destination for foreign investment in the region? To put it bluntly, the answer is, No. The reason why is simple: Pakistan has had volatile and episodic growth since the 1950s, and we: have low rates of local investment, lag in innovation and suffer from low productivity. We need strong efforts to come out of this vicious circle of low investment, low innovation and low productivity.

What can account for this circle of low investment leading to low innovation and low productivity? PIDE’s Growth Reform Agenda (PIDE, 2021) has pointed out that the volatile growth (Figure 1) is reflective of policy inconsistency and lack of cohesiveness.

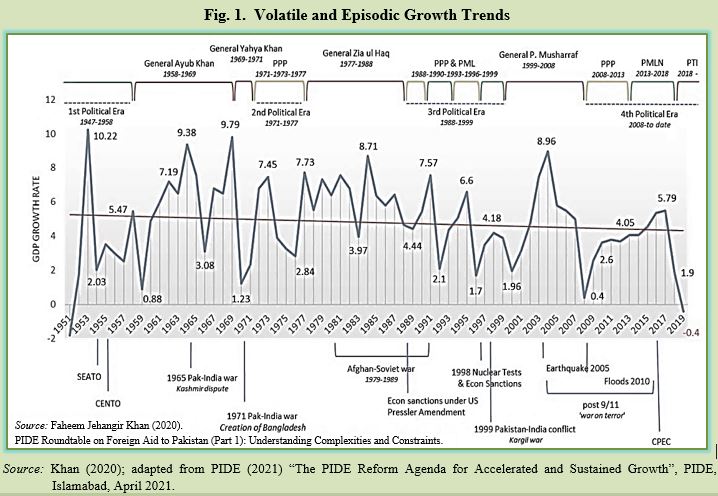

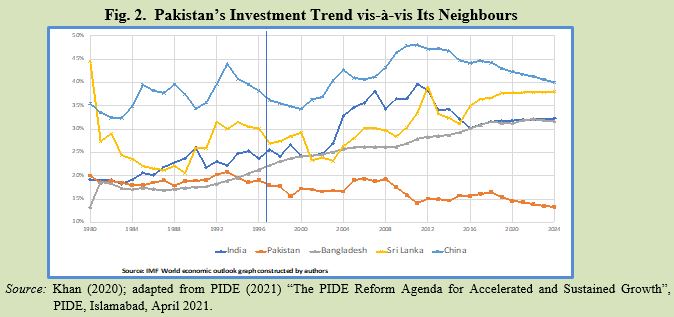

Reversing this trend and making Pakistan a better and more appealing destination for FDI will require concerted and coordinated efforts to develop an enabling environment addressing the vicious circle of low investment (see Figure 2), low innovation and low productivity (Figure 3). As evident, investment levels in Pakistan are well below regional comparator nations, even Bangladesh and Sri Lanka.

Coming to the issue of productivity, according to the PIDE Reform Agenda, the highs of Total Factor Productivity (TFP) have typically been associated with deregulation, liberalisation, better fundamentals, institutional & structural reforms, and private sector dynamism. Low level of productivity, on the other hand, has been associated with soaring external debt, adverse policy environment like Statutory Regulatory Orders (SROs), and policy instability reflected in frequent changes in taxes and tariffs. The decline in investment and productivity[1] over time is well documented (Figure 3).

Source: Siddique (2020), adapted from PIDE (2021).

Source: Siddique (2020), adapted from PIDE (2021).

________________________________

[1] As measured by Total Factor Productivity (TFP), traditionally calculated by dividing a country’s total output by a weighted average of labour and capital inputs.

Constraints to Growth in Pakistan: In a Nutshell

- Poor investment climate.

- Limited capacity for transactions.

- Policy inconsistencies.

- Skewed incentive structure.

- Limited regulatory skills.

- Long term financing constraints.

- Large government footprint.

- High documentation costs.

- High transaction costs.

- Over-regulation.

- Institutional and legal framework that constrain economic activity.

Source: PIDE (2021).

The solution to this problem can be approached on two fronts i.e., market development and regulations and government policies. On the market side we need to address issues affecting low productivity, investment and R&D. Weak technology adaptability and acquisition and creativity stemming from a nascent knowledge economy. There is also the lack of vibrant cities and internet access affecting market development. On the government policy side, we need strong institutions, consistent policies, reducing the footprint of the government through de-regulation and increasing engagement with the private sector.

PAKISTAN AS A DESTINATION FOR FDI

Engaging in investment is a competitive process with multiple avenues available, so the question is why would an investor choose to invest in a particular place? Global indicators such as competitiveness rankings provide a benchmark and clue regarding the attractiveness of a destination for investment. Here we consider such key rankings in light of Pakistan’s attractiveness as an investment destination.

PAKISTAN’S GLOBAL COMPETITIVENESS AND ENABLING ENVIRONMENT

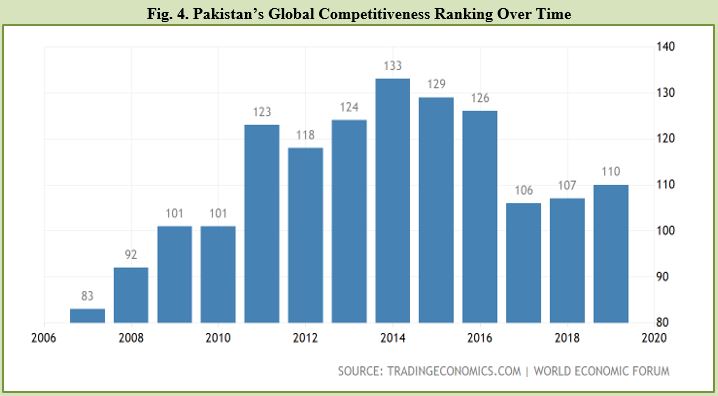

An analysis of Pakistan’s competitiveness in global context highlights the areas that need the attention of the government. Improvements on the main fronts (see Table 1) can help in attracting FDI into the country. Pakistan ranked 107 in the Global Competitiveness Index (GCI) in 2018, and this had fallen to 110th in 2020 (see Figure 4)—indicating a worsening of our competitiveness in the global arena, rather than an improvement.

Looking at the pillars of the GCI (Table 1), Pakistan’s standing in a regional context is weak, ranking well below India in most cases, and worse than even Bangladesh in some cases. Compared to the regional average, Pakistan fares better (than average) for 2 pillars; one of which is market size, attributable to our high population levels. Pakistan fares worse than the average for 9 pillars; clearly a holistic approach is required to improve the country’s ranking and help attract FDI.

Source: Global Competitive Index 2018, World Economic Forum,

Source: Global Competitive Index 2018, World Economic Forum,

Authors’ calculations.

Note: Region average includes Pakistan.

Red indicates ranking below average.

Blue indicates average ranking.

Green indicates ranking better than average.

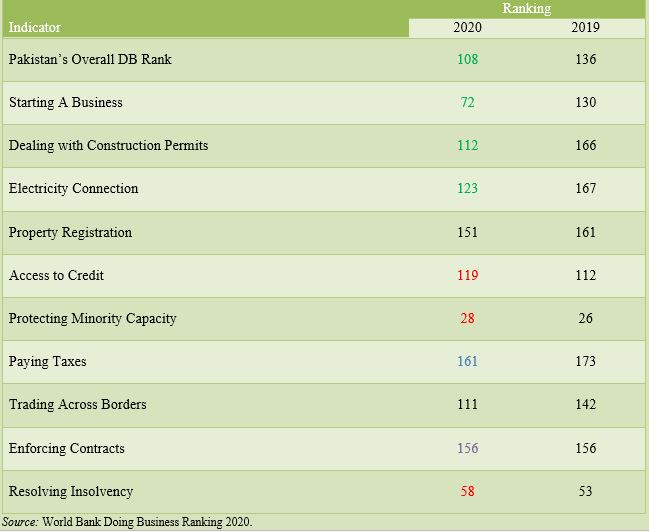

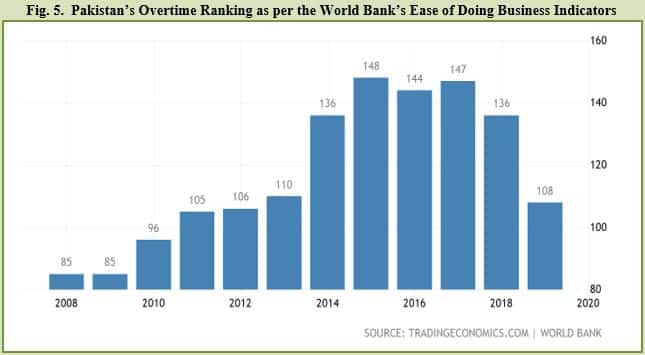

Compared with last year, Pakistan does appear to have made some improvement in providing an enabling environment for businesses, as seen by a temporal comparison of the indicators used in the World Bank Ease of Doing Business (EODB) Index[2] (Table 2; Figure 5).

Note: Green indicates a substantial improvement in the ranking

Blue indicates small improvement

Yellow indicates no change, and

Red indicates a deterioration.

___________________________________

[2] The EODB index has been the subject of much controversy and the methodology and rankings can be considered suspect, but the underlying factors can still be used to get a sense of the sort of enabling environment a specific country has, and what improvements, if any, have been made over time. So, the argument here is not banking on the absolute raking or numbers instead the message is to concentrate on the indicators where improvements can bring actual ease in business activities.

Though progress has been made on reducing hurdles, they remain. The question is what can be done to turn the tide and improve appeal of Pakistan’s economy as a destination for FDI.

IMPROVING THE APPEAL OF PAKISTAN AS AN FDI DESTINATION

We believe the answer lies in making Special Economic Zones (SEZ) be made fully functional, as mandated in the SEZ Act, in the short run. Doing so in the true spirit of the word will mean that businesses interested in operating in Pakistan will not have to face such hurdles. In the long term, a holistic approach is required to address underlying structural constraints that are resulting in a less favourable business environment, as detailed in PIDE’s Reform Agenda. The steps that can be taken in this context are discussed below.

IDENTIFY CHANNELS AND MODALITIES TO DEVELOP SEZS

Coming to SEZs, Pakistan needs to identify the channels and modalities required to develop these zones and populate them on a fast-track basis with productive units. We already have 19 SEZs approved and many more planned; what we need to do is to rationalise these, operationalise the most efficient and encourage businesses to avail the available facilities.

Investor’s confidence can be boosted, and regional competitiveness increased if we no longer use selling of industrial plots in the SEZ as a criterion for its success. Instead, the transfer of technology and actual production taking place should be used as the criterion.

Pakistan’s SEZ Act 2012 (Amended 2016) was implemented almost 10 years ago, and the generous incentives including 10-year tax exemption, granted under the act, expired in June 2020. On the policy front, it is high time to assess the policy, identify areas that need redressal and what weaknesses are present so a better and more informed policy can be implemented.

In the short-term what Pakistan needs to do is direct investment for securing a place in the global value chain by focusing on the following areas:

(1) Packaging.

(2) Assembling.

(3) Processing.

(4) IT solutions.

In the medium-term, Pakistan needs to facilitate the transfer of Chinese and other, sunset industries to set up in SEZs. This will facilitate the transfer of technology, provide employment, and increase our domestic output and integration into the global economy.

CHINESE FOREIGN INVESTMENT ALONG THE BRI ROUTE

There is limited information available at this time on a number of areas that can offer input on potential areas for Chinese FDI to enter in Pakistan under the Belt and Road Initiative (BRI). Pakistan’s Board of Investment (BOI) must engage with think tanks and support detailed analysis on what sectors are being preferred by Chinese investors, what products does China import that Pakistan can provide, what is current level of skills in Pakistan and where is the deficit between the two countries.

What are the areas where Pakistan needs FDI, and what Pakistan can learn from the international experience in SEZs along with the facilities being offered? BOI needs to explore options for incentivising investment in firm-level R&D to enhance productivity and competitiveness of firms in consultation with stakeholders.

CAPITALISING ON POTENTIAL FOR EFFECTIVE REFORM

The potential exists in Pakistan for effective reform, and the key to attracting FDI from China and elsewhere is to capitalise on this potential. We need the right set of skills and knowledge for youth to capitalise on our demographic dividend. We need to align the curricula of universities and technical and vocational training institutions to the skills required by firms in SEZs, for the 4th industrial revolution and for a digital economy.

REDEFINING THE ROLE OF BOARD OF INVESTMENT

The role of BOI needs to be redefined to effectively lead, in collaboration with NDRC (China), industrial cooperation and B2B collaborations. In this regard the role of BOI must be to establish links and cooperation between SEZs in both countries. Special desks to facilitate Chinese investors in Pakistan’s Embassies in China and Dubai must be set up. And finally, BOI must take ownership of SEZs under the China-Pakistan Economic Corridor (CPEC) initiative.

FINAL THOUGHTS

While specifically targeting FDI from China in the short term to benefit from CPEC is a commendable goal, Pakistan must make efforts to encourage FDI into the country in general. With Pakistan being in a geo-strategic location and surrounded by contesting power struggles, bringing China specific policies will give such policies strategic importance. Along with greater influence, we anticipate greater interruption as well. If Pakistan provides incentives and facilitates investment in true spirit for all, it will create goodwill with investors and encourage further investment.

By focusing on developing our credibility, competitiveness and capacity, market forces can reveal our comparative advantage. We also need to map our human capital and develop a holistic strategy for incorporating the required skills, expertise and work ethics that are required to compete effectively into our society. A silo approach to develop our human capital will undoubtedly fail, as it has in the past, and create hurdles for potential investors. SEZs should be developed in the true spirit of the SEZ Act and developed as an economic proposition rather than a tool for equity.

REFERENCES

Pakistan, Government of (2015). Special economic zones act, 2012. Islamabad: Modified and Amended, Board of Investment, Government of Pakistan, 31st December 2015.

Khan, Faheem J. (2020). Foreign aid to Pakistan: Understanding complexities and constraints. Presentation made at PIDE Roundtable Discussion Series on Foreign Aid in Pakistan – Part I, August 7, 2020.

PIDE (2021) The PIDE reform agenda for accelerated and sustained growth. PIDE, Islamabad, April 2021.

Siddique, Omer (2020). Total factor productivity and economic growth in Pakistan: A five decade analysis. (PIDE Working Paper 2020:11).