Need of the Hour: Simplicity and not Complexity in the SEZ Act

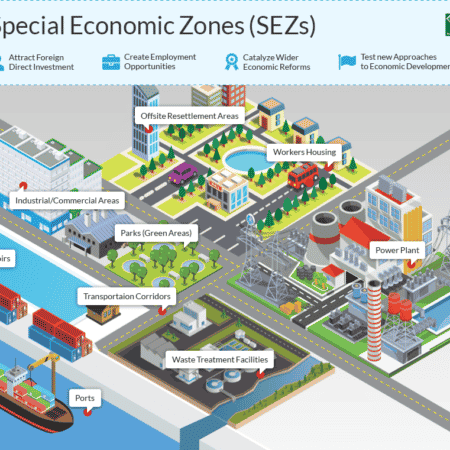

Despite the attractive incentives package (summarized in Table 1 below), the Special Economic Zones (SEZs) are yet to bring noticeable growth to the industrial sector. Ideally, the SEZ Act (2012) promises an attractive incentive package for both the SEZ developers and the SEZ enterprises. The Act envisions SEZs as vibrant production hubs for the manufacturing activities to take place. However, the definition mainly portrays a place for production activities only. It is evident from the fact that the foremost eligibility requirement for any ‘industrial zone developer’ to apply for SEZ status is the possession of minimum 50 acres of land. Although the requirement makes sense for a place meant for accommodating production units (with manufacturing activities), such a prerequisite is not universal for all types of economic activities and therefore must be flexible. This is important for the fact that land does not come with unlimited availability and has alternative uses. So, if the aim is to facilitate new firms, then the SEZ incentives should be allowed to all those sectors and forms which have viable business prospects.

Table 1: Incentives Package for SEZ Development

| Facilities promised to SEZ enterprises at SEZs | Incentives package provided under SEZ Act |

| 1. One-stop shop | For SEZ developers |

| 2. Electricity, Gas and Water | 1. Exemption from all taxes in relation to the development and operation of the SEZ for five years |

| 3. Sewerage, drainage and wastewater treatment | 2. One-time exemption from customs duties and taxes for all capital goods imported into the country |

| 4. Local-road-inside and access-road-outside zone | 3. Electricity and Gas lines at Zero point |

| 5. Communications (telephone, Internet, cable TV) | 4. One-window facility by BOI and at SEZA |

| 6. Security (policing and check posts) | 5. Duty-free vehicles allowed under certain conditions |

| 7. Boundary wall around the zone | For SEZ Enterprises |

| 8. Firefighting facilities | 1. One-time exemption from all taxes and duties in relation to the import of plant and machinery |

| 9. Academic and vocational training facilities | 2. Exemption from all taxes on income for 10 years for SEZ enterprises starting production by 30th June 2020, otherwise for 5 years if enterprises start production after June 2020. |

| 10. Display centres for products | 3. Additional benefits are admissible under certain conditions |

Source: SEZ Act (2016)

Analyzing the bottlenecks attached to the SEZ Act, it is obvious that the services sector needs to be dealt with differently. We live in a digital age where services and products often occupy virtual space rather than physical space. In this context, by having the land requirements to qualify for SEZ status, the Act fails to accommodate the IT industry, thus leaving it out of its ambit. This highlights the need for introducing tailor-made facilitation for the services sector, possibly by differentiating SEZs by types.

Additionally, another bottleneck is the inability to deliver the promised infrastructural facilities as mentioned in the SEZ Act. It is important to note here that since the enactment of SEZ Act in 2012, and the subsequent notification of SEZs in 2016, there is no SEZ where all the promised facilities are available (dedicated utilities connection, dedicated grid station, one-window facilitation at SEZ premises etc.). Moreover, the condition that SEZ benefits are only allowed to a firm which becomes operational by June 2020, makes the equation further difficult to solve, given the fact that the promised facilities at the notified SEZs are still missing. A contributing factor to the gap is a scarcity of finances needed for the provision of dedicated services under the SEZ Act. Furthermore, there is a need for greater clarity regarding the relevant financing authority, either federal or provincial.

Lastly, the fact is that the SEZs were primarily established at new places, to be developed from scratch. It would perhaps have been more economical if the government were to focus on enhancing and extending existing industrial estates and allowing SEZ status to new firms (as happened at Hattar SEZ). This would have bypassed the massive infrastructure development setup costs at newly created SEZs. Unfortunately, since a substantial amount of time has passed with significant investments made, the government is now constrained to follow through with the new SEZs’ development or forego the finances already committed. Nonetheless, it would be effective to rethink how to make existing SEZs and Industrial Estates more vibrant and productive, and ensuring the provision of all the promised facilities to gain investors’ confidence in future projects.

Download full PDF

Connect with the Pakistan Institute of Development Economics

Subscribe

Select topics and stay current with our latest insights

- +92 51 9248051

- [email protected]

- PIDE, QAU Campus, Islamabad