Background of the study

“The ordinance for the revival of sick industrial units is widely promoted as an amnesty scheme awarded through an SRO. Empirical backing for the given time frames and criteria is lacking in the ordinance. Setting aside these three aspects, the ordinance is a step in the right direction as it will boost productivity and employment. Ideally, it will benefit existing firms with increased flow of resources and facilitate new entrants with fresh ideas.”

Introduction

While announcing the scheme on March 1, 2022, the Prime Minister acknowledged that the manufacturing sector is a crucial driver of the growth of an economy; an assertion that is in line with existing research on the subject. Previous attempts at boosting industrial production in Pakistan have been reactive rather than proactive and failed to make any substantial progress towards achieving their stated goals. As with those earlier attempts, the current ordinance is also reactive rather than proactive, but where it diverges is with the inclusion of clearly specified sunset 4 clauses and criteria in its components.

It is also revealed that registered arthies have business experience ranging between 10 to 30 years. Figure 1 depicts the agricultural supply chain of the grain market in Pakistan 2 . Our survey reveals that pakka arthi rarely deals directly with the farmer rather he approaches the farmer through kacha arthi and broker in the grain market.

While announcing the scheme on March 1, 2022, the Prime Minister acknowledged that the manufacturing sector is a crucial driver of the growth of an economy; an assertion that is in line with existing research on the subject. Previous attempts at boosting industrial production in Pakistan have been reactive rather than proactive and failed to make any substantial progress towards achieving their stated goals. As with those earlier attempts, the current ordinance is also reactive rather than proactive, but where it diverges is with the inclusion of clearly specified sunset 4 clauses and criteria in its components.

___________________________

1Senior Research Economist, PIDE

2Assistant Professor, PIDE

3The authors are indebted to Dr Nadeem ul Haque for the idea and inspiration for this pide knowledge brief, and for the invaluable feedback given on several earlier drafts. We would also like to acknowledge the input and assistance of Dr.Mahmood Khalid in revising earlier drafts of this work. Any errors or omissions are solely our responsibility.

4The final eligible date to avail the package

This knowledge brief provides an overview of the key highlights of the recently announced industrial package, and an analysis of its essential aspects. The analysis centres on the argument that the package should not be thought of as an amnesty scheme, the time frames and criteria used should be based on sound economic research and evidence. Furthermore, international best practices must be followed, and the ground realities of the domestic economy must be accounted for.

What follows is a discussion of these critical aspects and why the package needs to evolve and incorporate them.

Amnesty: the act of granting a pardon to a large group of individuals or entities

Laundering: transfer (illegally obtained funds/investments) through third party to conceal the true source

Tax Holiday: a government incentive that temporarily reduces or eliminates taxes for a temporary period

Locked Capital: capital of sick industrial units that cannot be easily disposed of or repurposed for other uses

Key Aspects of the Ordinance

The ordinance is a detailed document laying out specifics of the benefit being offered to potential investors. There are four areas of concern that policymakers are advised to take notice of, and address going forward: namely the optics of the ordinance as an amnesty scheme, lack of evidence-based time frames, ignoring accepted best practices and not accounting for the realities on the ground.

Calling the Ordinance an Amnesty Scheme is a disservice to investors and should be revisited

Amnesty schemes inherently reward non-abidance; it is an outcome that serves as a disincentive for those who fulfil their legal obligations. When we are going to encourage investment with funds that (may possibly) have been associated with questionable transactions, what incentive is there for an honest investor to bring funds into the economy?

When the purpose is to encourage investment in the economy for many years, why do we want to question where the funds come from, and discourage the

honest investor?

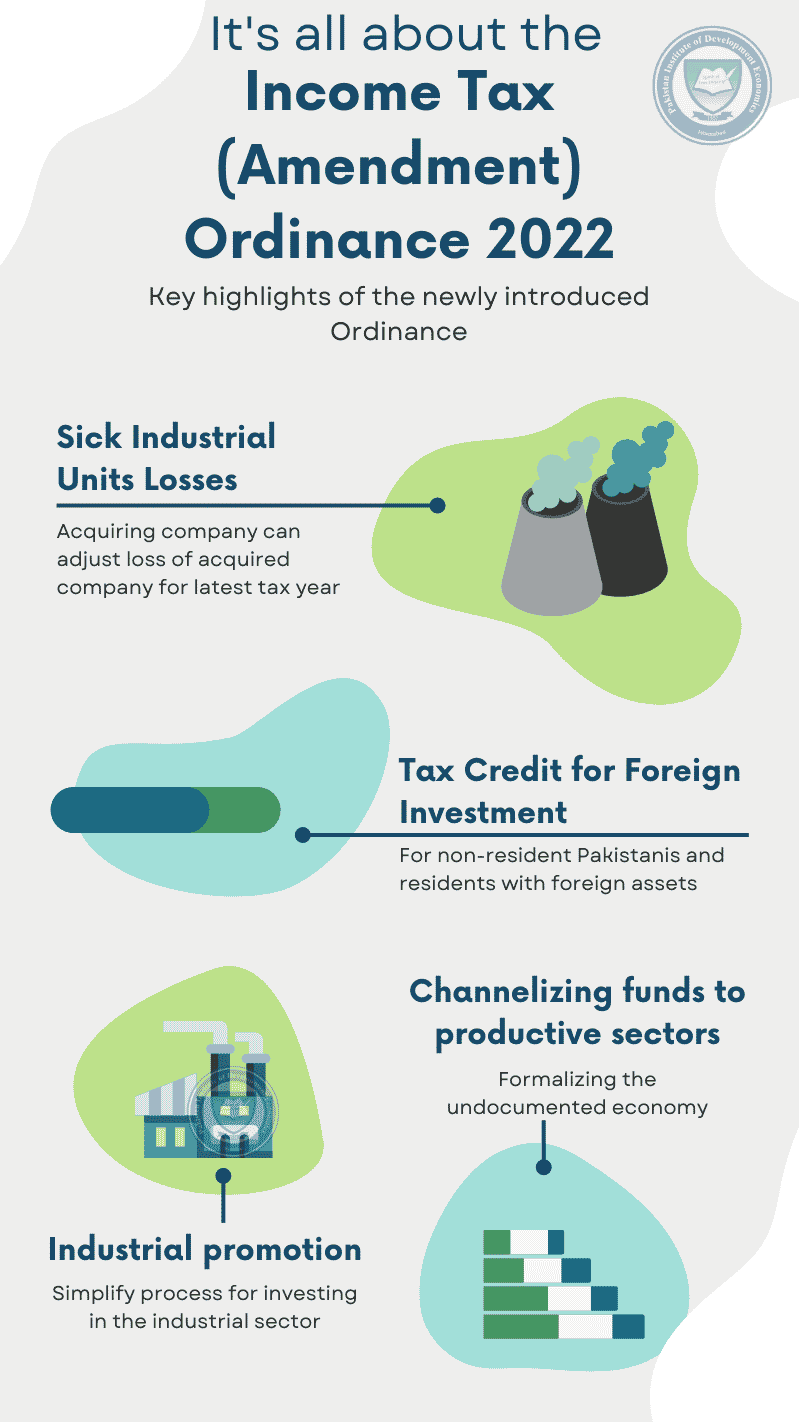

Ordinance Positives

- A scheme targeting specific sectors allows resources to be put to better use

- Channelizes resources to resource-starved Small and Medium Enterprises (SMEs)

- Tap locked capital (in the form of sick units) by providing incentives for restoring and investing in sick units

- Tapping overseas resources by incentivizing overseas investors to get five-(5) year tax holiday for investing in the economy

- Widening the tax base by reducing tax rate

- Putting off-the-radar capital to productive use without sparking frictions

- Clearly specified sunset clauses and criteria given for key aspects

Moreover, if an investor is bringing funds into the economy for several years and promoting economic activity in the form of industrial production, is it essential to know the source of the funds? Given the poor state of investment in the economy, do we really want to look a gift horse in the mouth?

The argument that funds will be laundered is debatable in any case. Funds being laundered means illicit gains are entering the system, circulating, and then being withdrawn without any benefit to the economy (see Box 1). However, the ordinance restricts industrial units (invested under this scheme) from being sold for four (04) years. It requires production activity to be started within three (03) years. Therefore, the funds cannot be withdrawn so promptly. Even if the industrial unit is subsequently sold, the transaction will have been documented and the funds used for productive activity.

That means that the scheme is not a channel for laundering funds. Consequently, this aspect of the ordinance needs to be revisited and not promoted as a “no questions asked” amnesty scheme.

This scheme is not a channel for funds to be laundered

Base time frames on credible research to be widely accepted. Enforce sunset clauses to promote e fficiency

The revival scheme covers units that are declared as “sick” 5 and incurring losses for 3 years. An October 2019 report identified 687 industrial units as being “sick” units. However, the motivation for excluding other (older) units is not stated explicitly. If an investor is willing to invest in such units, the government should allow such endeavors if the investor has exercised due diligence. Furthermore, feasibility studies can be used as a criterion to determine whether a

unit can be revived. Faraz (2020 & 2019) has discussed

the issue of unproductive capital at length. Allowing four (04) years for revival of any sick unit appears an arbitrary benchmark as the rule of thumb suggests 5 years instead. Such figures, along with the figures for commercial production which is stated as 2 years, should be based on research and empirical evidence and be industry or sector specific. Offering firms/investors an incentive with a clear sunset clause and specified performance criteria as given in the ordinance is a step in the right direction. It reflects the focus of the government on promoting efficiency over other interests, which will encourage further investment in the economy (Ahmad and Qadir, 2021). However, reducing the time will put pressure on firms and may lead to a higher failure rate; at the same time allowing generous incentives can also introduce inefficiencies of its own. The trade-of should be resolved through research.

Initiatives must be in line with economic theory and international best practices

In the corporate world, the ownership of firms is often consolidated or transferred through transactions. The firm consolidates its assets and operations with another firm, acquires the other firm or sells of some or all its assets to another firm. These are referred to as mergers and acquisitions (M&A), which are part of industrial economic activity. But standard M&A are explicitly excluded from this scheme. M&A promote efficiency and optimal use of scarce resources so they should be encouraged. Moreover, the motivation for targeting foreign investment separately is unclear. All investment should be treated equally, and same benefits given to all. Bifurcating the two will create distortions in the economy.

M&A promote e ciency and optimal use of scarce resources and should be encouraged

All investment should be treated equally; same bene ts given to all.

The reason for setting the minimum equity requirement is unclear. Such a requirement will exclude most SMEs 6 from investment and should be revisited. Instead of restricting investment to at least PKR 50 million or above, investors or a consortium of investors with a business plan for any amount may be facilitated through the scheme.

Excluded Industries:

Arms And Ammunition Explosives Sugar Cigarettes Aerated Beverages Flour Mills Vegetable Ghee Cooking Oil Manufacturing

The list of sectors excluded from investment must be based on sound reasoning. Other than defence or security related matters, the selection criteria being used may be provided in the form of background paper to ensure transparency and credibility as well as to spark future research.

Ground Realities Must Be Accounted for

Experience with similar schemes in different sectors has yielded mediocre results at best. Amnesty schemes by name have not succeeded in attracting a substantial influx of resources into the economy. Furthermore, given existing delays in issuing rebates (most recently in the case of Millat Tractors Limited 7 ) to entrepreneurs, measures must be put in place to ensure timely payment of dues and processing of red tape. The general trend in the economy has been to prefer speculative investments rather than re-investing in the businesses. So, requiring re-investing in expansion and/or modernization is economically sound and desirable from the point of view of encouraging economic activity in the country. Furthermore, it will discourage speculative investments in unproductive activities such as investing in real estate and foreign currency.

Conclusion

If we set aside the fact that this scheme is awarded through an SRO and propagated in the media as an amnesty scheme, the initiative by itself is a step in right direction. However, SROs culture, as pointed out by PIDE (2021), is something to be avoided, as SROs are inherently distortionary. These introduce an element of uncertainty & discrimination, and necessarily lacks requisite debate and deliberation in relevant forums.If we set aside the fact that this scheme is awarded through an SRO and propagated in the media as an amnesty scheme, the initiative by itself is a step in right direction. However, SROs culture, as pointed out by PIDE (2021), is something to be avoided, as SROs are inherently distortionary. These introduce an element of uncertainty & discrimination, and necessarily lacks requisite debate and deliberation in relevant forums. In the aftermath of the scheme being announced, the focus somehow seems to have been more on amnesty provision than on the more substantive measures promoting industrial activity. As discussed above, amnesties can have an adverse impact on investment and compliance decisions, and there is no sound economic justification for offering such a provision.

the focus somehow seems to have been more on amnesty provision in the ordinance rather than on the more substantive measures promoting industrial activity

IN A NUTSHELL

PIDE’s analysis shows that the industrial policy package or Income Tax (Amendment) Ordinance, 2022 has seven positives geared towards promoting industrial activity and upliﬞing the economy, given time limits and requirements lack appropriate justification. Further debate and research are required to refine the Ordinance for achieving its intended goals.

This industrial revival initiative will channelize resource to more productive uses by industries. The initiative provides access to resources by deficient industries, which is expected to boost productivity and employment generation. SMEs, which provide a basic eco-system for feasible industrialization, are the intended beneficiaries of this initiative (PIDE, 2022). Furthermore, rather than restricting entry of new firms, the initiative is expected to benefit existing players and facilitate new entrants having fresh ideas. Effective implementation of this initiative will not increase the footprint of the government, which is already too pervasive, at 67% of GDP (PIDE, 2020). Consequently, the expectation is that frictions will not increase. On the flip side however, the time frames and criteria used for exclusion of specific sectors and other aspects of the initiative need to be based on proper empirical evidence, which if already undertaken should be made available at relevant websites as background papers.

References

Ahmad, Iftikhar and Qadir, Usman (2021), “Inviting FDI: Is Pakistan an Attractive Destination”, PIDE Knowledge Brief, No.2021: 34. PIDE, Islamabad. August 12, 2021.

Faraz, Naseem (2020), “Tracing the Zombies: Unproductive Capital in Pakistan”, PIDE Policy and Research

Faraz, Naseem (2019), “Zombie Firms in Pakistan”, PIDE Policy and Research

PIDE (2020), “Increasing Space for Investment & Entrepreneurship Through Reducing the Footprint of Government on

The Economy in Pakistan”. PIDE, Islamabad, 2020.

PIDE (2021), “The PIDE reform agenda for accelerated and sustained growth”. PIDE, Islamabad, April 2021.

PIDE (2022), “Evaluations of Regulatory Authorities, Government Packages, And Policies”. PIDE, Islamabad, 2022.