SEVENTH AND EIGHTH REVIEWS UNDER THE EXTENDED ARRANGEMENT UNDER THE EXTENDED FUND FACILITY, REQUESTS FOR WAIVERS OF NON OBSERVANCE OF PERFORMANCE CRITERIA, AND EXTENSION, AUGMENTATION, AND REPHASING OF ACCESS

International Monetary Fund (IMF) issued a staff report on the seventh and eighth reviews of the extended arrangement under the Extended Fund Facility (EFF) on September 1, 2022. As per the review report, the authorities of Pakistan are allowed to draw USD 1.1 billion, keeping in view the measures taken by authorities to address fiscal and external challenges. The IMF board has also approved the extension of the EFF till June 2023 along with extra Special Drawing Rights (SDR) of 720 million, bringing the total access under the EFF to about USD 6.5 billion.

The review report has also identified some priority measures to be considered by the Pakistani authorities, such as the implementation of an approved budget, market-determined exchange rate policy, proactive and prudent monetary policy, the expansion of the social safety net, and structural reforms related to the performance of state-owned enterprises (SOEs) and governance. The set of measures that have been identified contains both short-term and medium-term measures to promote long-term growth. In this regard, the Pakistan Institute of Development Economics (PIDE) has also been working extensively to identify the measures that are necessary to remove the bottlenecks in the economy to improve productivity and increase growth.

Therefore, the objective of this document is twofold, i.e., a commentary on the measures suggested by the review report and what other measures should be part of the program.

1.GROWTH IS LIMITED BY STRUCTURAL BOTTLENECKS THAT THE PROGRAM DOES NOT ADDRESS

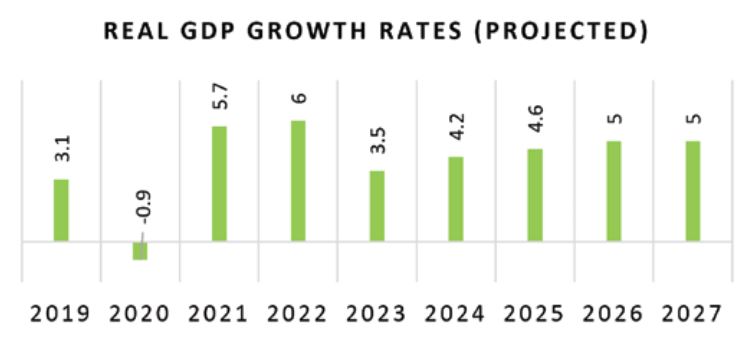

The PIDE reform agenda (RAPID) notes that Pakistan needs a sustainable growth rate of around 8 percent over a long period, given the population pressure. However, the review report shows that the economy of Pakistan starts overheating at a growth rate of around 6 percent. PIDE notes that this is primarily due to the low investment rate in the economy accompanied by a worsening long-term trend of investment as a percentage of GDP. Additionally, there are substantial regulatory and productivity constraints in the economy that the program should be addressing (See PIDE Reform Agenda (RAPID) and PIDE Sludge Audit. I).

Source: IMF Pakistan Country Report (2022)

Source: IMF Pakistan Country Report (2022)

2. WHERE SHOULD THE INTEREST RATES BE?

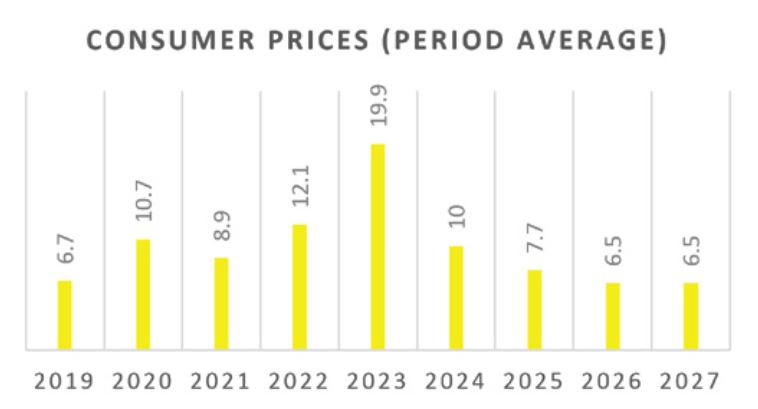

The review report suggests that the State Bank of Pakistan (SBP) will continue a tight monetary policy, as per the standard prescription, to restrain higher inflation expectations. According to the review, the SBP and the IMF staff agreed to a tight monetary policy to achieve positive real interest rate. However, the real rate remains negative! And the real rate is likely to remain negative through the program period. This implies that the nominal interest rate should be 20 percent or even more. However, it would be challenging for the SBP to curtail inflation through monetary tightening due to the following facts:

Source: IMF Pakistan Country Report (2022)

Source: IMF Pakistan Country Report (2022)

- The SBP began to tighten monetary policy in November 2021[1] but failed to achieve positive real rate and control inflation.

- The review report projects that the broad money growth will be around 12 percent during the FY-2023. Therefore, PIDE argues that the demand-side pressure will not be a major driver of inflation in the near future. The current wave of inflation may be more supply-side shock driven.

- PIDE estimates suggest that supply-side pressures will contribute to inflation by more than 80 percent during FY-2023[2] . Hence, further tightening of the monetary policy may not be desirable. Interestingly, the Risk Assessment Matrix of the review report also points out that several supply shocks, including the disruption of supply chains, higher energy prices, and higher commodity prices are more important for inflation. Nevertheless, further tightening of the monetary policy may reduce the exchange rate pressures. The current external sector pressure is due to surging import demand. A tight monetary policy may reduce external sector pressure through effective import demand management. The review report, however, did not take a clear stance on this issue.

- We also agreed with IMF that all concessionary interest rates should be eliminated to ensure that the policy rate has teeth. Unfortunately, we do not see the program recommending a time path to achieve this goal. There should be a sunset clause.

_______

[1] From November 2021 to July 2022 the SBP has raised the policy rate by 800 basis points — from 7 % to 15 %.

[2] In-house calculations, see PIDE Analytics 01 for the methodology.

_______

For Full Text Download PDF